- Sweden

- /

- Telecom Services and Carriers

- /

- OM:BAHN B

3 Top Swedish Dividend Stocks Yielding Up To 4.9%

Reviewed by Simply Wall St

As global markets show signs of recovery and optimism grows for economic stability, the Swedish stock market has also been gaining traction. In this favorable environment, dividend stocks in Sweden stand out as attractive options for investors seeking steady income. A good dividend stock typically offers a reliable payout, strong financial health, and potential for growth—all crucial factors in the current market climate.

Top 10 Dividend Stocks In Sweden

| Name | Dividend Yield | Dividend Rating |

| Bredband2 i Skandinavien (OM:BRE2) | 4.39% | ★★★★★★ |

| Betsson (OM:BETS B) | 5.64% | ★★★★★☆ |

| Nordea Bank Abp (OM:NDA SE) | 8.70% | ★★★★★☆ |

| Zinzino (OM:ZZ B) | 4.06% | ★★★★★☆ |

| HEXPOL (OM:HPOL B) | 3.56% | ★★★★★☆ |

| Axfood (OM:AXFO) | 3.13% | ★★★★★☆ |

| Duni (OM:DUNI) | 4.92% | ★★★★★☆ |

| Skandinaviska Enskilda Banken (OM:SEB A) | 5.46% | ★★★★★☆ |

| Avanza Bank Holding (OM:AZA) | 4.76% | ★★★★★☆ |

| Bahnhof (OM:BAHN B) | 3.94% | ★★★★☆☆ |

Click here to see the full list of 22 stocks from our Top Swedish Dividend Stocks screener.

Let's review some notable picks from our screened stocks.

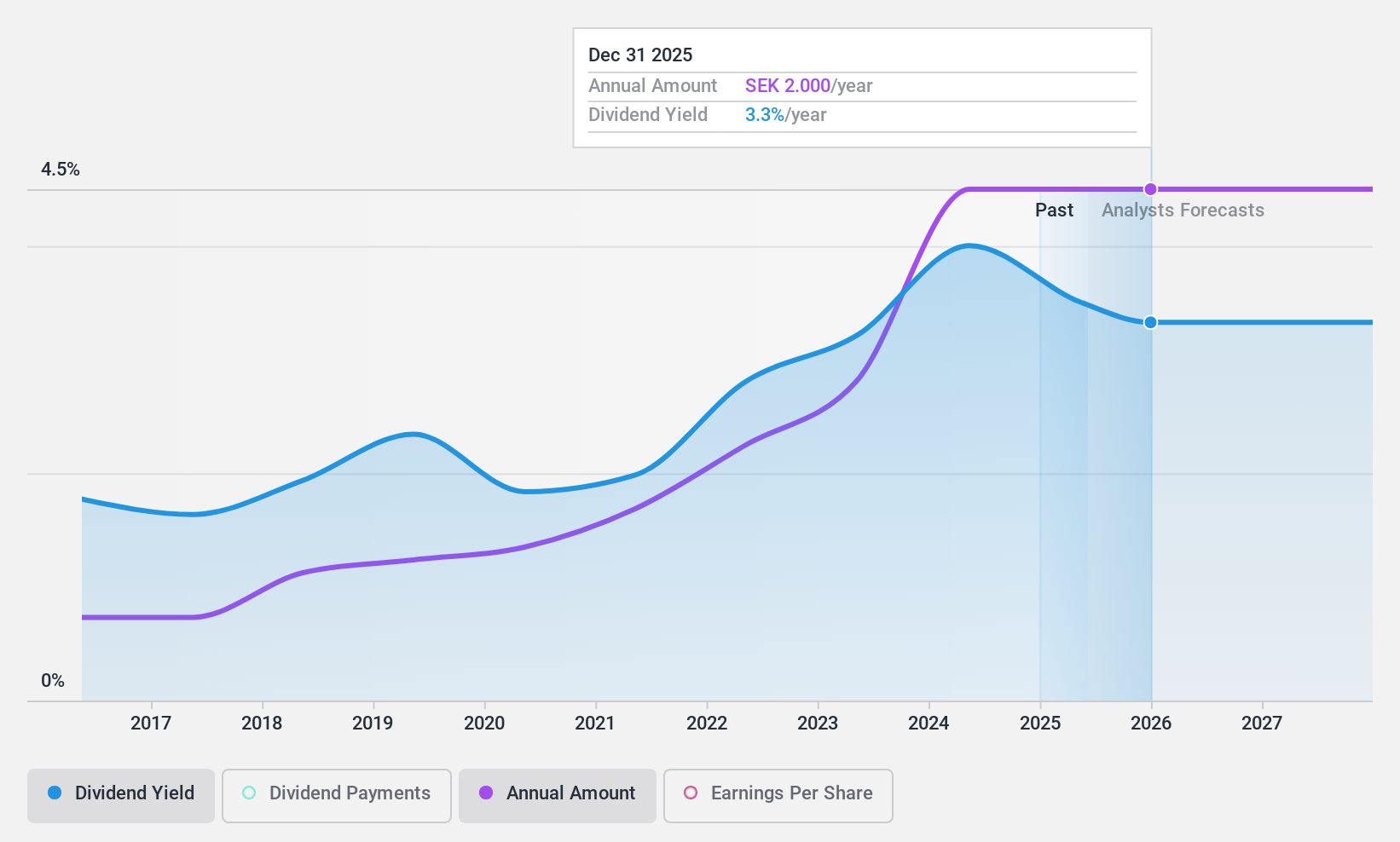

Bahnhof (OM:BAHN B)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Bahnhof AB (publ) operates in the Internet and telecommunications sector across Sweden and Europe, with a market cap of SEK5.45 billion.

Operations: Bahnhof AB (publ) generates revenue primarily from the Retail Market, which accounts for SEK1.30 billion, and the Corporate Market (excluding Typhoon), contributing SEK606.24 million.

Dividend Yield: 3.9%

Bahnhof's dividend payments have been stable and reliable over the past 10 years, demonstrating growth with little volatility. However, its current dividend yield of 3.94% is lower than the top 25% of Swedish market payers. Although dividends are covered by free cash flow (76.9%), they are not well covered by earnings due to a high payout ratio (97.5%). The stock trades at 33.1% below our fair value estimate, indicating potential undervaluation.

- Click here and access our complete dividend analysis report to understand the dynamics of Bahnhof.

- Our expertly prepared valuation report Bahnhof implies its share price may be too high.

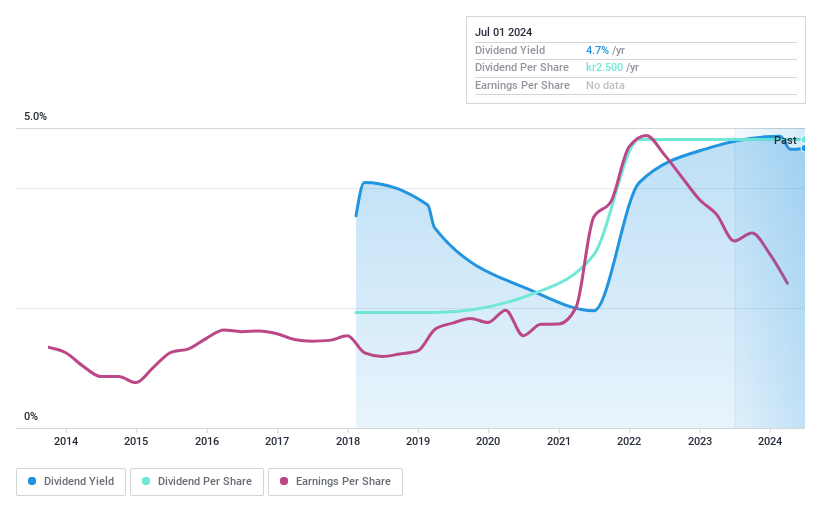

FM Mattsson (OM:FMM B)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: FM Mattsson AB (publ) develops, manufactures, and sells water taps and related products for bathrooms and kitchens across several European countries with a market cap of SEK 2.16 billion.

Operations: FM Mattsson AB (publ) generates revenue from two primary segments: SEK 783.23 million from international markets and SEK 1.12 billion from Nordic countries.

Dividend Yield: 4.9%

FM Mattsson's dividend payments have been growing steadily, though the company has only a 7-year track record. Its dividends are well covered by cash flows (49.5% payout ratio) and earnings (86.3% payout ratio). The stock is trading at 62.5% below its estimated fair value, suggesting potential undervaluation. Effective June 19, 2024, the company changed its name to FM Mattsson Mora Group AB (publ).

- Dive into the specifics of FM Mattsson here with our thorough dividend report.

- The valuation report we've compiled suggests that FM Mattsson's current price could be quite moderate.

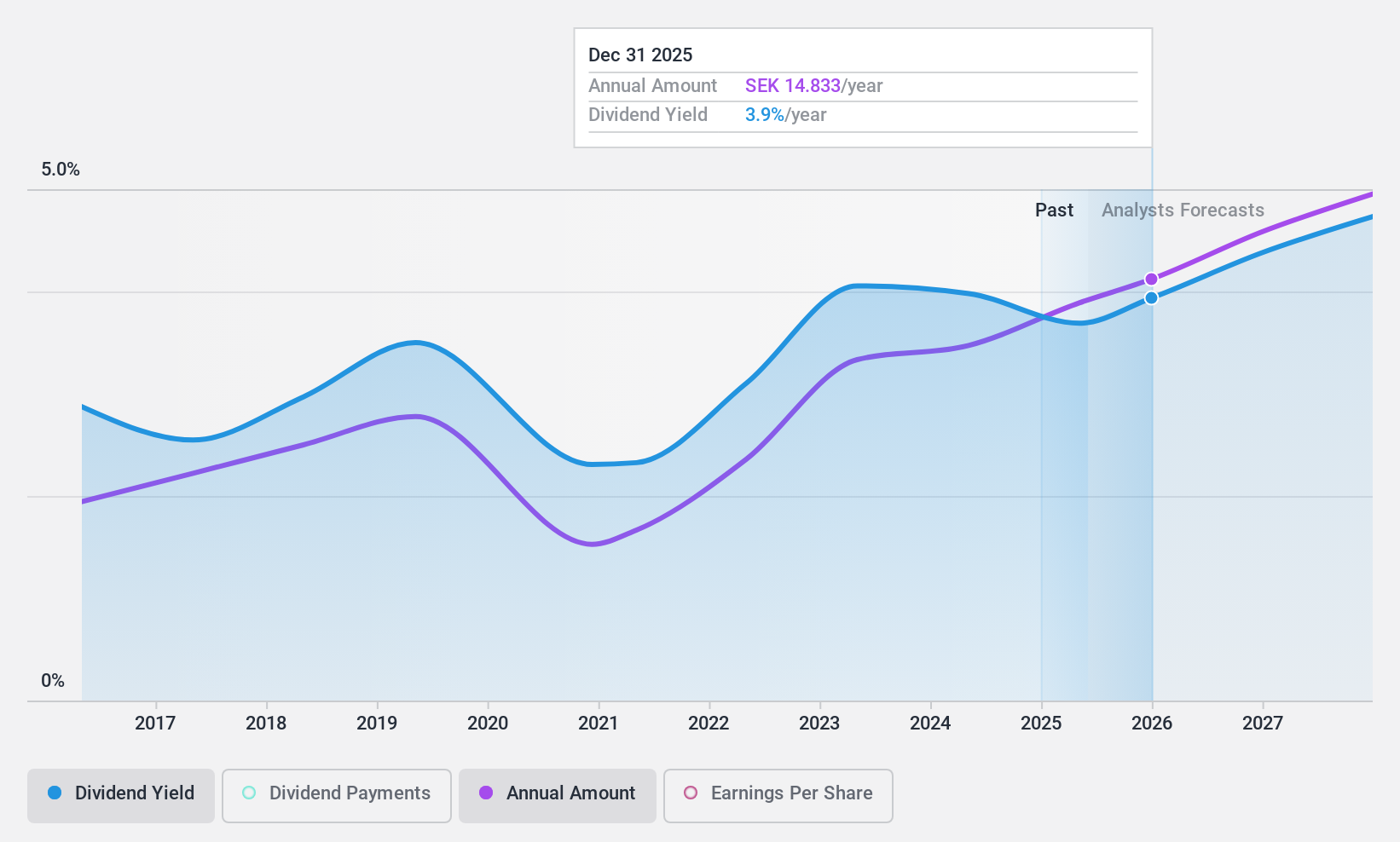

Loomis (OM:LOOMIS)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Loomis AB (publ) offers services in the distribution, payments, handling, storage, and recycling of cash and other valuables with a market cap of SEK 23.44 billion.

Operations: Loomis AB (publ) generates revenue from its key segments: Loomis Pay (SEK 77 million), Europe and Latin America (SEK 14.32 billion), and the United States of America (SEK 15.45 billion).

Dividend Yield: 3.7%

Loomis has a reasonable payout ratio of 59.4%, indicating dividends are covered by earnings, and a low cash payout ratio of 26.3%, suggesting strong coverage by cash flows. However, its dividend history is unstable with significant volatility over the past decade. Recent buyback activity includes repurchasing 702,500 shares for SEK 199.75 million between May and June 2024, reflecting proactive capital management amidst rising sales and net income in Q2 2024.

- Take a closer look at Loomis' potential here in our dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Loomis shares in the market.

Next Steps

- Investigate our full lineup of 22 Top Swedish Dividend Stocks right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bahnhof might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:BAHN B

Bahnhof

Engages in the Internet and telecommunications business in Sweden and rest of Europe.

Flawless balance sheet with solid track record and pays a dividend.