Advertisement

How Electrolux Professional’s Reorganization Plan (OM:EPRO B) Has Changed Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this month, Electrolux Professional announced a major business reorganization targeting SEK175 million in annual cost savings by 2027, impacting production sites and employees across Europe.

- This operational shift may alter the company’s efficiency and profit outlook, potentially influencing how investors view its long-term prospects.

- We'll examine how the planned cost-saving measures could influence Electrolux Professional’s future earnings and operational risk narrative.

These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Electrolux Professional Investment Narrative Recap

For me, being a shareholder in Electrolux Professional means believing in its ability to grow earnings through ongoing innovation, global expansion, and the enhancement of operational efficiency. The recent business reorganization, targeting SEK175 million in annual cost savings by 2027, could improve profit margins in the medium term, but its immediate effect on the key catalyst, earnings growth via sustainable product rollout, may be limited as the benefits are not realized overnight. The biggest risk remains the pressure on margins from higher operational and R&D costs, which could offset anticipated improvements if innovation-driven returns take longer to materialize or do not match investment levels.

Among recent developments, the September announcement of large-scale cost-saving measures stands out most in this context. The planned restructuring, impacting several European sites and hundreds of employees, reflects management’s effort to address cost pressures and streamline operations. While this move is expected to enhance future profitability, it is also likely to influence near-term market sentiment and could reshape investor expectations for the company’s financial trajectory.

Yet, unlike the promise of future savings, the ongoing risk of R&D and operational cost pressures is something every investor should stay alert to because ...

Read the full narrative on Electrolux Professional (it's free!)

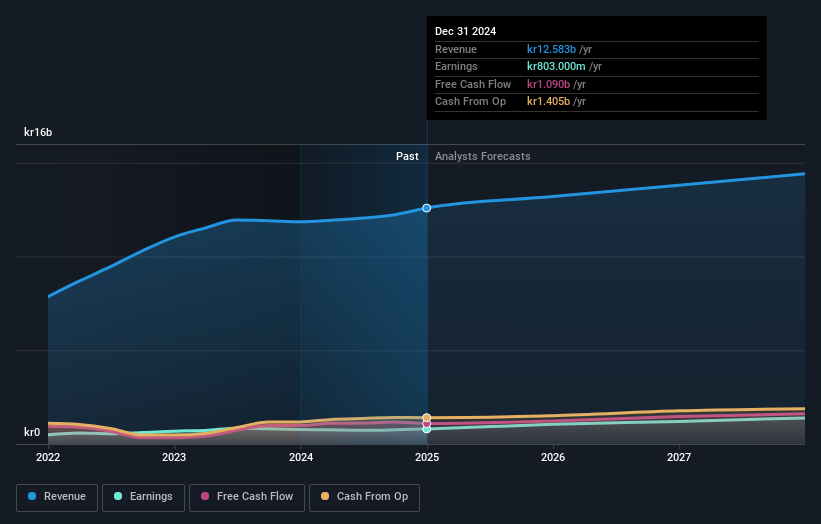

Electrolux Professional's narrative projects SEK14.2 billion revenue and SEK1.4 billion earnings by 2028. This requires 4.2% yearly revenue growth and a SEK582 million earnings increase from SEK818 million today.

Uncover how Electrolux Professional's forecasts yield a SEK75.00 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Every one of the 1 retail investor fair value estimates in the Simply Wall St Community arrived at SEK75 per share, flagging consensus on current undervaluation. Still, margin pressures from rising operational and R&D costs could weigh on Electrolux Professional’s future performance so you should consider a wide range of views before making up your mind.

Explore another fair value estimate on Electrolux Professional - why the stock might be worth as much as 16% more than the current price!

Build Your Own Electrolux Professional Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Electrolux Professional research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Electrolux Professional research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Electrolux Professional's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Electrolux Professional might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:EPRO B

Electrolux Professional

Provides food service, beverage, and laundry products and solutions to restaurants, hotels, healthcare, educational, and other service facilities.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor