With EPS Growth And More, ASSA ABLOY (STO:ASSA B) Makes An Interesting Case

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

In contrast to all that, many investors prefer to focus on companies like ASSA ABLOY (STO:ASSA B), which has not only revenues, but also profits. Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide ASSA ABLOY with the means to add long-term value to shareholders.

Check out our latest analysis for ASSA ABLOY

ASSA ABLOY's Earnings Per Share Are Growing

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. That makes EPS growth an attractive quality for any company. Over the last three years, ASSA ABLOY has grown EPS by 9.5% per year. That growth rate is fairly good, assuming the company can keep it up.

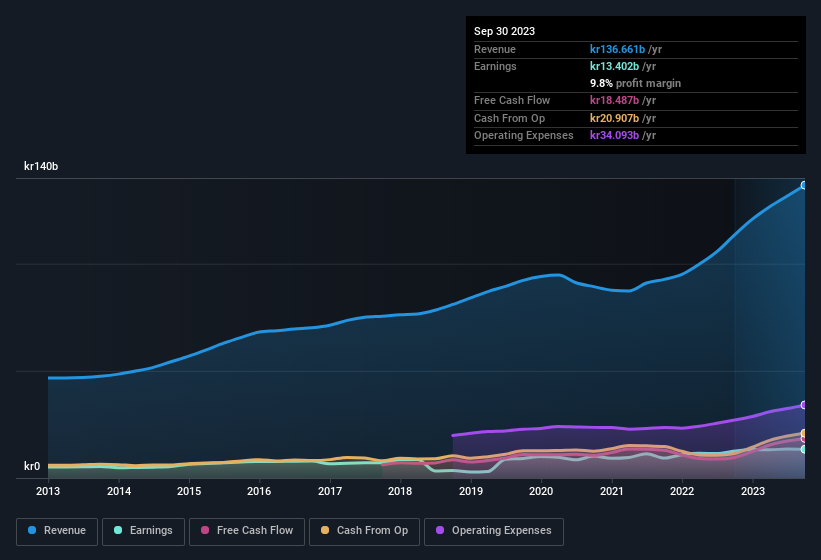

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While we note ASSA ABLOY achieved similar EBIT margins to last year, revenue grew by a solid 20% to kr137b. That's progress.

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for ASSA ABLOY's future profits.

Are ASSA ABLOY Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

We do note that, in the last year, insiders sold kr2.5m worth of shares. But that's far less than the kr37m insiders spent purchasing stock. This bodes well for ASSA ABLOY as it highlights the fact that those who are important to the company having a lot of faith in its future. We also note that it was the President, Nico Delvaux, who made the biggest single acquisition, paying kr15m for shares at about kr242 each.

On top of the insider buying, it's good to see that ASSA ABLOY insiders have a valuable investment in the business. To be specific, they have kr135m worth of shares. That's a lot of money, and no small incentive to work hard. Even though that's only about 0.05% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

Is ASSA ABLOY Worth Keeping An Eye On?

One positive for ASSA ABLOY is that it is growing EPS. That's nice to see. In addition, insiders have been busy adding to their sizeable holdings in the company. That makes the company a prime candidate for your watchlist - and arguably a research priority. What about risks? Every company has them, and we've spotted 1 warning sign for ASSA ABLOY you should know about.

Keen growth investors love to see insider buying. Thankfully, ASSA ABLOY isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:ASSA B

ASSA ABLOY

Provides door opening and access products, solutions, and services for the institutional, commercial, and residential markets in Europe, the Middle East, India, Africa, North and South America, Asia, and Oceania.

Solid track record established dividend payer.