Advertisement

- Saudi Arabia

- /

- Logistics

- /

- SASE:4263

SAL Saudi Logistics Services (TADAWUL:4263) Is Paying Out A Larger Dividend Than Last Year

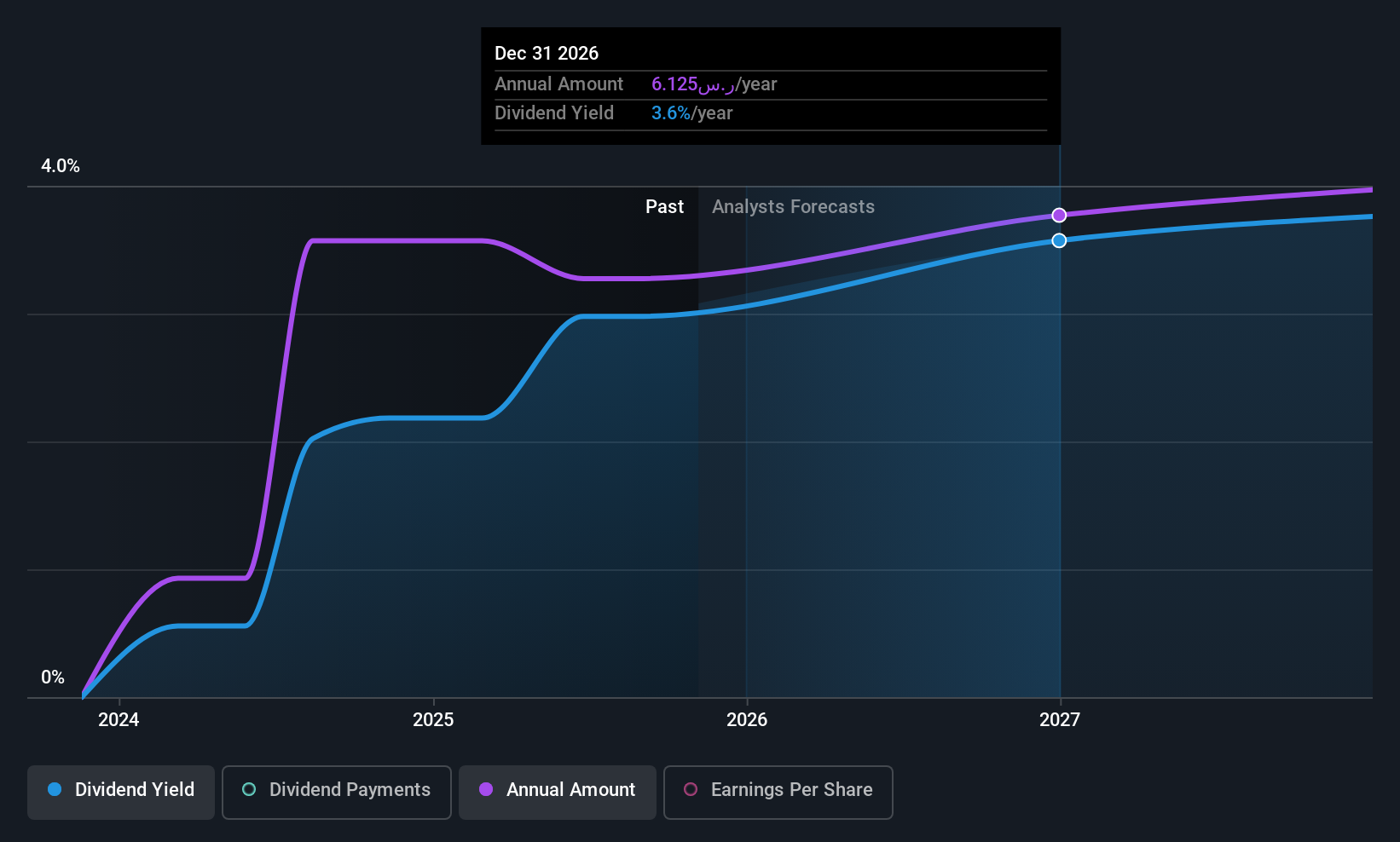

SAL Saudi Logistics Services Company (TADAWUL:4263) will increase its dividend from last year's comparable payment on the 1st of December to SAR1.70. This makes the dividend yield about the same as the industry average at 3.1%.

SAL Saudi Logistics Services' Future Dividend Projections Appear Well Covered By Earnings

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. Prior to this announcement, SAL Saudi Logistics Services' dividend made up quite a large proportion of earnings but only 55% of free cash flows. Since the dividend is just paying out cash to shareholders, we care more about the cash payout ratio from which we can see plenty is being left over for reinvestment in the business.

Looking forward, earnings per share is forecast to rise by 8.9% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could be 72% by next year, which is in a pretty sustainable range.

Check out our latest analysis for SAL Saudi Logistics Services

SAL Saudi Logistics Services' Dividend Has Lacked Consistency

Looking back, the dividend has been unstable but with a relatively short history, we think it may be a bit early to draw conclusions about long term dividend sustainability. Since 2023, the dividend has gone from SAR1.51 total annually to SAR5.32. This works out to be a compound annual growth rate (CAGR) of approximately 88% a year over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. SAL Saudi Logistics Services' EPS has fallen by approximately 71% per year during the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think SAL Saudi Logistics Services' payments are rock solid. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 1 warning sign for SAL Saudi Logistics Services that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4263

SAL Saudi Logistics Services

Provides logistics and supply chain solutions in the Kingdom of Saudi Arabia.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor