Advertisement

- Saudi Arabia

- /

- Packaging

- /

- SASE:3007

Zahrat Al Waha For Trading (TADAWUL:3007) Is Reinvesting At Lower Rates Of Return

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. In light of that, when we looked at Zahrat Al Waha For Trading (TADAWUL:3007) and its ROCE trend, we weren't exactly thrilled.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Zahrat Al Waha For Trading, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

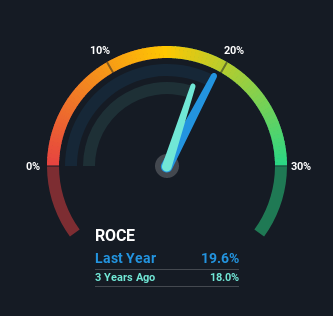

0.20 = ر.س60m ÷ (ر.س557m - ر.س250m) (Based on the trailing twelve months to March 2021).

Therefore, Zahrat Al Waha For Trading has an ROCE of 20%. On its own, that's a standard return, however it's much better than the 9.7% generated by the Packaging industry.

Check out our latest analysis for Zahrat Al Waha For Trading

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Zahrat Al Waha For Trading, check out these free graphs here.

What Can We Tell From Zahrat Al Waha For Trading's ROCE Trend?

When we looked at the ROCE trend at Zahrat Al Waha For Trading, we didn't gain much confidence. To be more specific, ROCE has fallen from 35% over the last five years. Given the business is employing more capital while revenue has slipped, this is a bit concerning. This could mean that the business is losing its competitive advantage or market share, because while more money is being put into ventures, it's actually producing a lower return - "less bang for their buck" per se.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 45%, which has impacted the ROCE. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. What this means is that in reality, a rather large portion of the business is being funded by the likes of the company's suppliers or short-term creditors, which can bring some risks of its own.

The Key Takeaway

In summary, we're somewhat concerned by Zahrat Al Waha For Trading's diminishing returns on increasing amounts of capital. The market must be rosy on the stock's future because even though the underlying trends aren't too encouraging, the stock has soared 106%. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

On a separate note, we've found 1 warning sign for Zahrat Al Waha For Trading you'll probably want to know about.

While Zahrat Al Waha For Trading may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Zahrat Al Waha For Trading might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SASE:3007

Zahrat Al Waha For Trading

Engages in the manufacturing and sale of PET preforms and caps in the Kingdom of Saudi Arabia.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.0% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor