Advertisement

- Saudi Arabia

- /

- Paper and Forestry Products

- /

- SASE:1202

What You Can Learn From Middle East Company for Manufacturing and Producing Paper's (TADAWUL:1202) P/S

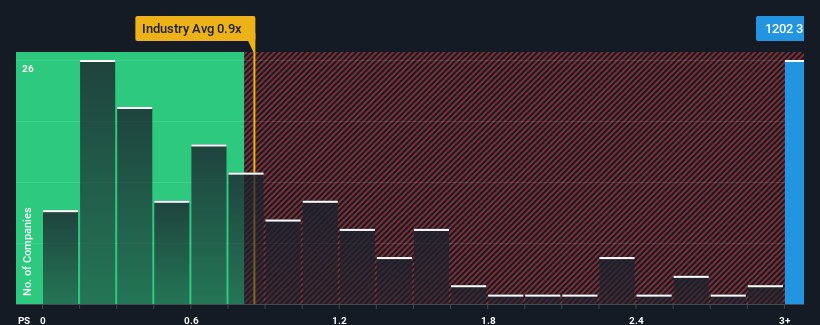

When you see that almost half of the companies in the Forestry industry in Saudi Arabia have price-to-sales ratios (or "P/S") below 0.9x, Middle East Company for Manufacturing and Producing Paper (TADAWUL:1202) looks to be giving off strong sell signals with its 3.6x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Middle East Company for Manufacturing and Producing Paper

How Middle East Company for Manufacturing and Producing Paper Has Been Performing

Recent times haven't been great for Middle East Company for Manufacturing and Producing Paper as its revenue has been falling quicker than most other companies. One possibility is that the P/S ratio is high because investors think the company will turn things around completely and accelerate past most others in the industry. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Middle East Company for Manufacturing and Producing Paper.Do Revenue Forecasts Match The High P/S Ratio?

Middle East Company for Manufacturing and Producing Paper's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 20%. Regardless, revenue has managed to lift by a handy 18% in aggregate from three years ago, thanks to the earlier period of growth. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next three years should generate growth of 18% per year as estimated by the two analysts watching the company. With the industry only predicted to deliver 9.1% each year, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Middle East Company for Manufacturing and Producing Paper's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Middle East Company for Manufacturing and Producing Paper's P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Middle East Company for Manufacturing and Producing Paper maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Forestry industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Middle East Company for Manufacturing and Producing Paper (at least 1 which doesn't sit too well with us), and understanding them should be part of your investment process.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SASE:1202

Middle East Company for Manufacturing and Producing Paper

Engages in the production and sale of container boards and industrial papers in the Kingdom of Saudi Arabia, the Middle East, Africa, Asia, and Europe.

Adequate balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor