Advertisement

- Saudi Arabia

- /

- Paper and Forestry Products

- /

- SASE:1202

Middle East Company for Manufacturing and Producing Paper's (TADAWUL:1202) Share Price Not Quite Adding Up

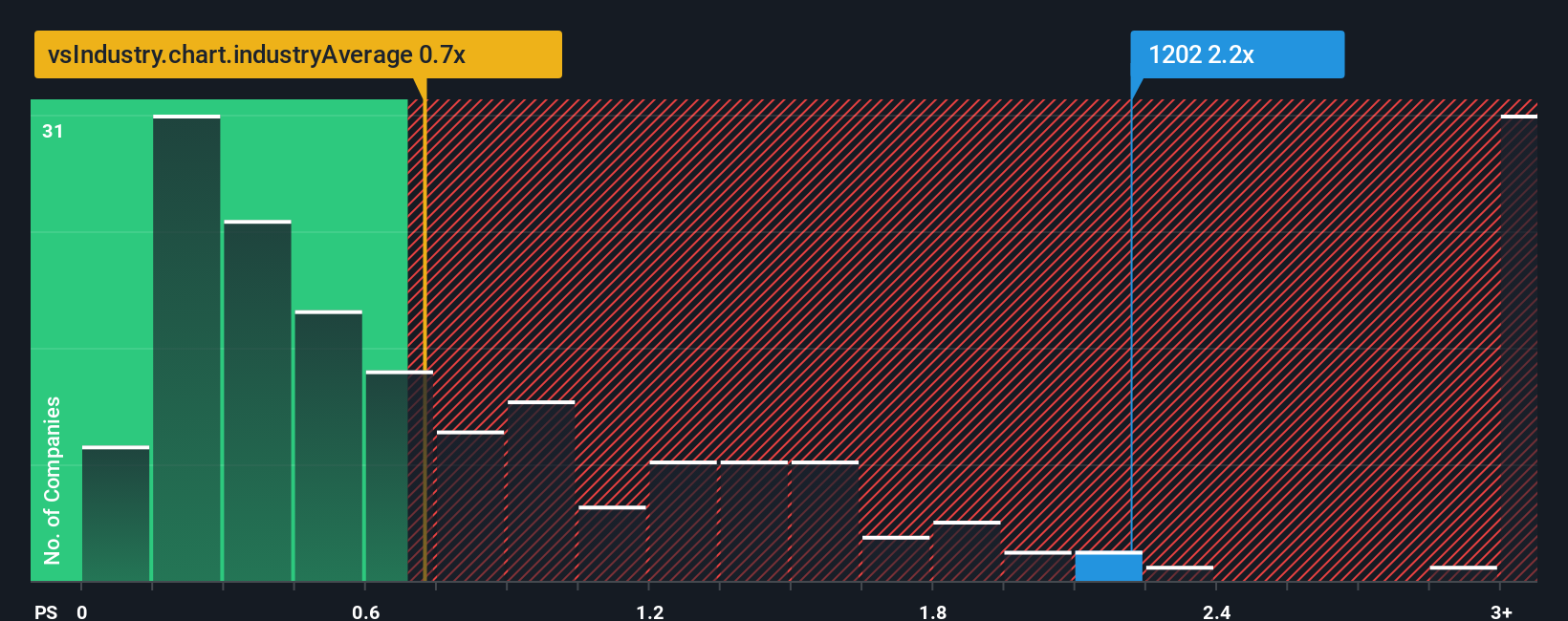

Middle East Company for Manufacturing and Producing Paper's (TADAWUL:1202) price-to-sales (or "P/S") ratio of 2.2x may not look like an appealing investment opportunity when you consider close to half the companies in the Forestry industry in Saudi Arabia have P/S ratios below 0.7x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Middle East Company for Manufacturing and Producing Paper

How Middle East Company for Manufacturing and Producing Paper Has Been Performing

Middle East Company for Manufacturing and Producing Paper certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Middle East Company for Manufacturing and Producing Paper's future stacks up against the industry? In that case, our free report is a great place to start.How Is Middle East Company for Manufacturing and Producing Paper's Revenue Growth Trending?

Middle East Company for Manufacturing and Producing Paper's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 22% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 7.0% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the lone analyst covering the company suggest revenue should grow by 11% over the next year. Meanwhile, the rest of the industry is forecast to expand by 10%, which is not materially different.

With this in consideration, we find it intriguing that Middle East Company for Manufacturing and Producing Paper's P/S is higher than its industry peers. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

The Key Takeaway

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Analysts are forecasting Middle East Company for Manufacturing and Producing Paper's revenues to only grow on par with the rest of the industry, which has lead to the high P/S ratio being unexpected. The fact that the revenue figures aren't setting the world alight has us doubtful that the company's elevated P/S can be sustainable for the long term. A positive change is needed in order to justify the current price-to-sales ratio.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Middle East Company for Manufacturing and Producing Paper, and understanding should be part of your investment process.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:1202

Middle East Company for Manufacturing and Producing Paper

Engages in the production and sale of container boards and industrial papers in the Kingdom of Saudi Arabia, the Middle East, Africa, Asia, and Europe.

Adequate balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor