- Saudi Arabia

- /

- Insurance

- /

- SASE:8050

Earnings growth of 17% over 3 years hasn't been enough to translate into positive returns for Salama Cooperative Insurance (TADAWUL:8050) shareholders

While it may not be enough for some shareholders, we think it is good to see the Salama Cooperative Insurance Company (TADAWUL:8050) share price up 14% in a single quarter. But that doesn't help the fact that the three year return is less impressive. After all, the share price is down 50% in the last three years, significantly under-performing the market.

Since Salama Cooperative Insurance has shed ر.س72m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

Check out our latest analysis for Salama Cooperative Insurance

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

Salama Cooperative Insurance became profitable within the last five years. We would usually expect to see the share price rise as a result. So given the share price is down it's worth checking some other metrics too.

We note that, in three years, revenue has actually grown at a 26% annual rate, so that doesn't seem to be a reason to sell shares. It's probably worth investigating Salama Cooperative Insurance further; while we may be missing something on this analysis, there might also be an opportunity.

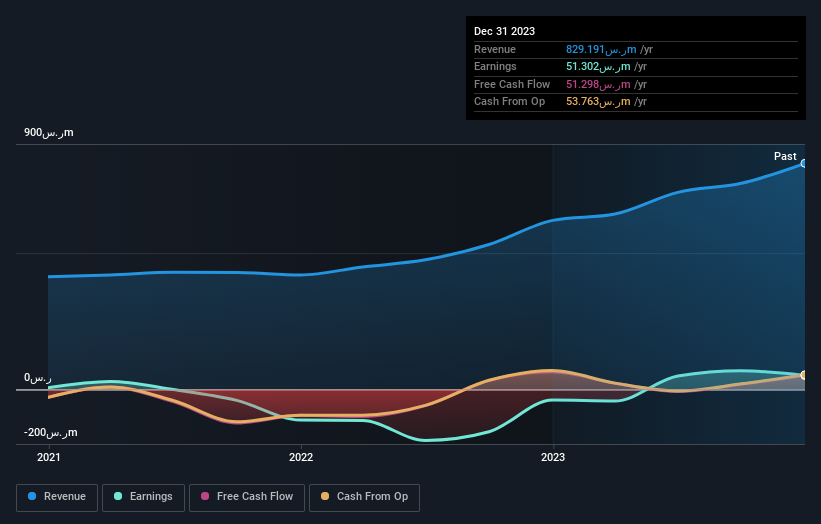

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

What About The Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Salama Cooperative Insurance's total shareholder return (TSR) and its share price return. Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. Salama Cooperative Insurance hasn't been paying dividends, but its TSR of -24% exceeds its share price return of -50%, implying it has either spun-off a business, or raised capital at a discount; thereby providing additional value to shareholders.

A Different Perspective

It's good to see that Salama Cooperative Insurance has rewarded shareholders with a total shareholder return of 114% in the last twelve months. That gain is better than the annual TSR over five years, which is 11%. Therefore it seems like sentiment around the company has been positive lately. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Like risks, for instance. Every company has them, and we've spotted 2 warning signs for Salama Cooperative Insurance (of which 1 is concerning!) you should know about.

But note: Salama Cooperative Insurance may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Saudi exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:8050

Salama Cooperative Insurance

Provides insurance products and services in the Kingdom of Saudi Arabia and internationally.

Flawless balance sheet and slightly overvalued.