Stock Analysis

- Saudi Arabia

- /

- Hospitality

- /

- SASE:4170

Strong week for Tourism Enterprises (TADAWUL:4170) shareholders doesn't alleviate pain of three-year loss

While it may not be enough for some shareholders, we think it is good to see the Tourism Enterprises Co. (TADAWUL:4170) share price up 19% in a single quarter. But that cannot eclipse the less-than-impressive returns over the last three years. Truth be told the share price declined 87% in three years and that return, Dear Reader, falls short of what you could have got from passive investing with an index fund. We really feel for shareholders in this scenario. It's a good reminder of the importance of diversification, and it's worth keeping in mind there's more to life than money, anyway.

Although the past week has been more reassuring for shareholders, they're still in the red over the last three years, so let's see if the underlying business has been responsible for the decline.

Check out our latest analysis for Tourism Enterprises

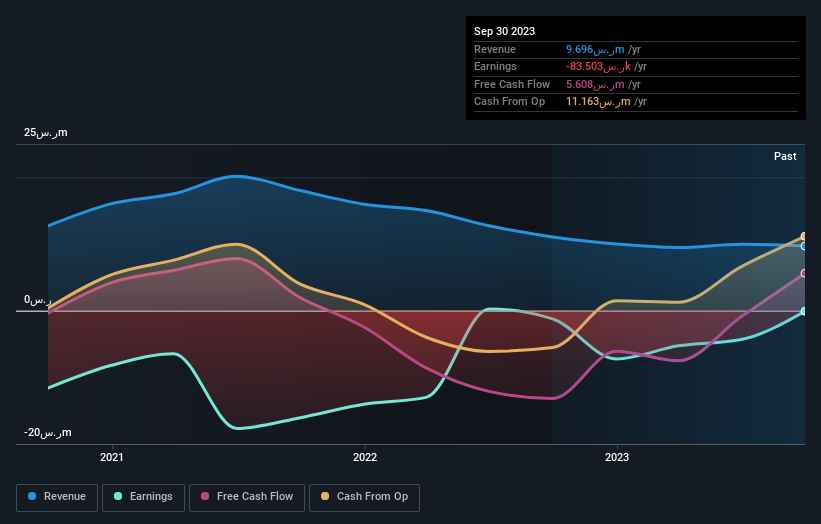

Tourism Enterprises isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally expect to see good revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

Over the last three years, Tourism Enterprises' revenue dropped 21% per year. That means its revenue trend is very weak compared to other loss making companies. And as you might expect the share price has been weak too, dropping at a rate of 23% per year. We prefer leave it to clowns to try to catch falling knives, like this stock. It's worth remembering that investors call buying a steeply falling share price 'catching a falling knife' because it is a dangerous pass time.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

If you are thinking of buying or selling Tourism Enterprises stock, you should check out this FREE detailed report on its balance sheet.

What About The Total Shareholder Return (TSR)?

We've already covered Tourism Enterprises' share price action, but we should also mention its total shareholder return (TSR). The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Tourism Enterprises hasn't been paying dividends, but its TSR of -13% exceeds its share price return of -87%, implying it has either spun-off a business, or raised capital at a discount; thereby providing additional value to shareholders.

A Different Perspective

Tourism Enterprises shareholders are up 0.5% for the year. Unfortunately this falls short of the market return. If we look back over five years, the returns are even better, coming in at 10% per year for five years. It's quite possible the business continues to execute with prowess, even as the share price gains are slowing. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Tourism Enterprises you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Saudi exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether Tourism Enterprises is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4170

Tourism Enterprises

Tourism Enterprises Co. engages in the managing of tourism buildings in the Kingdom of Saudi Arabia.

Flawless balance sheet and overvalued.