Advertisement

- Portugal

- /

- Construction

- /

- ENXTLS:TDSA

What Teixeira Duarte, S.A.'s (ELI:TDSA) 26% Share Price Gain Is Not Telling You

Despite an already strong run, Teixeira Duarte, S.A. (ELI:TDSA) shares have been powering on, with a gain of 26% in the last thirty days. This latest share price bounce rounds out a remarkable 706% gain over the last twelve months.

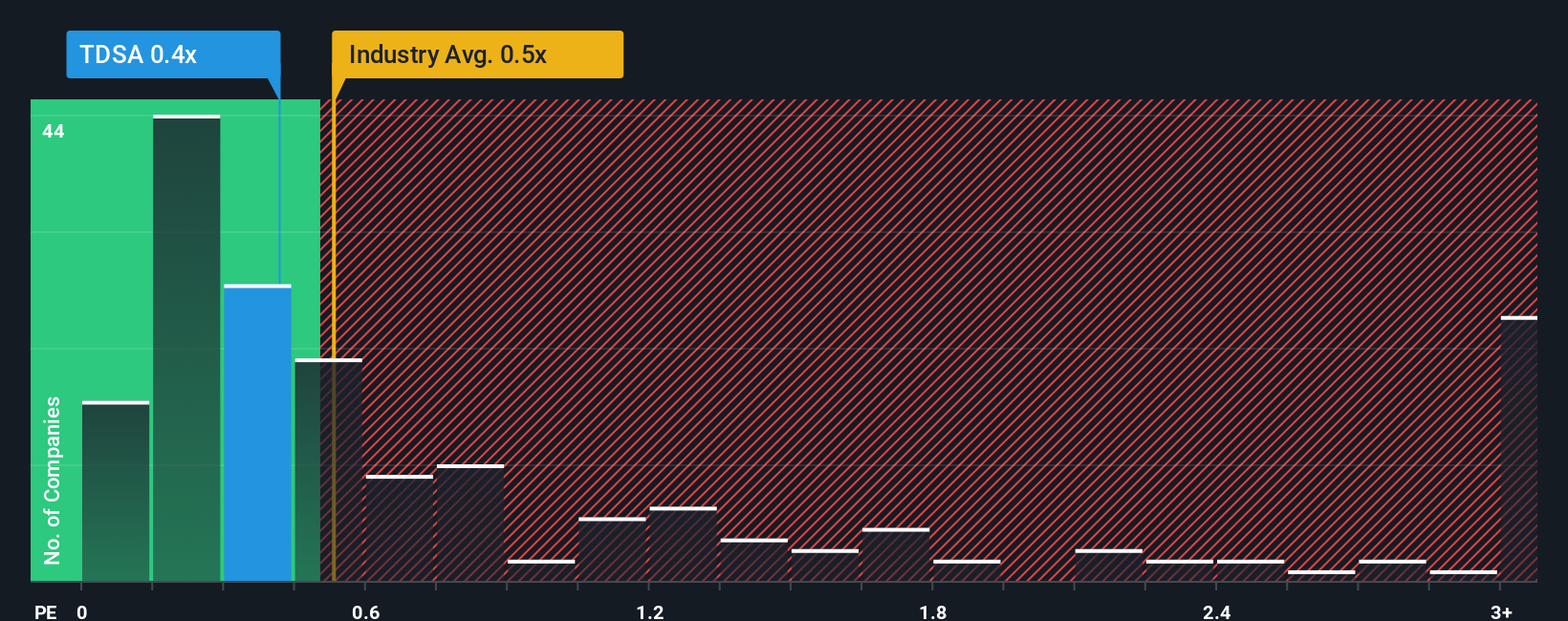

Although its price has surged higher, it's still not a stretch to say that Teixeira Duarte's price-to-sales (or "P/S") ratio of 0.4x right now seems quite "middle-of-the-road" compared to the Construction industry in Portugal, where the median P/S ratio is around 0.5x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Teixeira Duarte

How Teixeira Duarte Has Been Performing

As an illustration, revenue has deteriorated at Teixeira Duarte over the last year, which is not ideal at all. It might be that many expect the company to put the disappointing revenue performance behind them over the coming period, which has kept the P/S from falling. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

Although there are no analyst estimates available for Teixeira Duarte, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Teixeira Duarte's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 7.6%. Regardless, revenue has managed to lift by a handy 8.1% in aggregate from three years ago, thanks to the earlier period of growth. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

This is in contrast to the rest of the industry, which is expected to grow by 5.0% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in mind, we find it intriguing that Teixeira Duarte's P/S is comparable to that of its industry peers. It seems most investors are ignoring the fairly limited recent growth rates and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

What Does Teixeira Duarte's P/S Mean For Investors?

Its shares have lifted substantially and now Teixeira Duarte's P/S is back within range of the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Teixeira Duarte's average P/S is a bit surprising since its recent three-year growth is lower than the wider industry forecast. When we see weak revenue with slower than industry growth, we suspect the share price is at risk of declining, bringing the P/S back in line with expectations. Unless the recent medium-term conditions improve, it's hard to accept the current share price as fair value.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Teixeira Duarte you should know about.

If these risks are making you reconsider your opinion on Teixeira Duarte, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Teixeira Duarte might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTLS:TDSA

Teixeira Duarte

Operates in the construction, concessions and services, real estate, hospitality, distribution, and automotive sectors in Portugal, Angola, Brazil, Mozambique, and internationally.

Solid track record and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$26.69|18.6% undervalued

BE

Community Contributor