Advertisement

- Sweden

- /

- Life Sciences

- /

- OM:BICO

3 European Growth Companies With High Insider Ownership Seeing Up To 54% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

As European markets rebound, with the STOXX Europe 600 Index climbing 3.93% and major indices like Italy’s FTSE MIB and the UK’s FTSE 100 showing significant gains, investor sentiment has been buoyed by the ECB's rate cuts and a delay in higher tariffs by President Trump. In this environment of cautious optimism, growth companies with high insider ownership can be attractive as they often indicate confidence from those closest to the business, potentially aligning well with market conditions that favor strategic long-term investments.

Top 10 Growth Companies With High Insider Ownership In Europe

| Name | Insider Ownership | Earnings Growth |

| Pharma Mar (BME:PHM) | 11.8% | 40.1% |

| Vow (OB:VOW) | 13.1% | 111.2% |

| Bergen Carbon Solutions (OB:BCS) | 12% | 50.8% |

| Elicera Therapeutics (OM:ELIC) | 20.5% | 97.2% |

| CD Projekt (WSE:CDR) | 29.7% | 37.4% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| Lokotech Group (OB:LOKO) | 13.6% | 58.1% |

| Ortoma (OM:ORT B) | 27.7% | 68.6% |

| Nordic Halibut (OB:NOHAL) | 29.7% | 60.7% |

| Xbrane Biopharma (OM:XBRANE) | 20% | 82.7% |

Let's dive into some prime choices out of the screener.

Norbit (OB:NORBT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Norbit ASA offers technology solutions across various industries and has a market cap of NOK8.34 billion.

Operations: The company's revenue is derived from three main segments: Oceans (NOK743.90 million), Connectivity (NOK515.70 million), and Product Innovation and Realization (PIR) (NOK543.10 million).

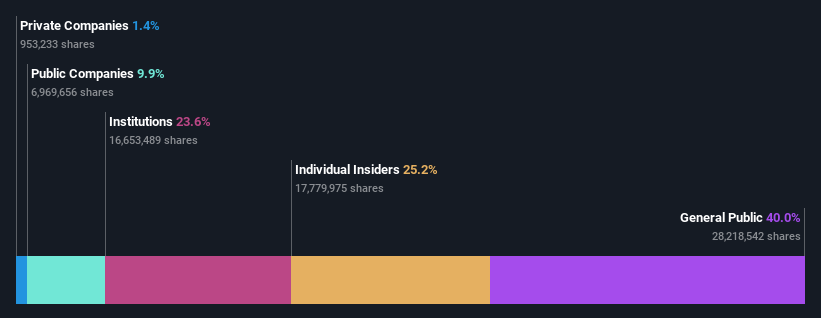

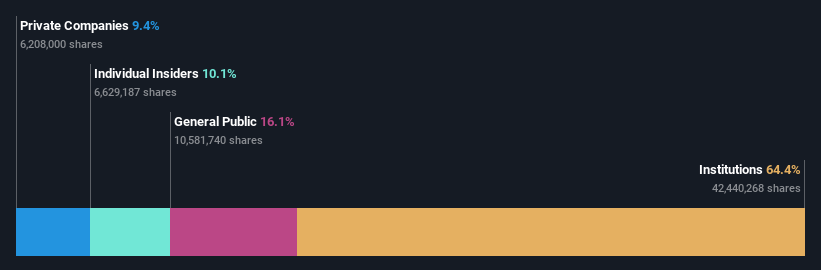

Insider Ownership: 13.2%

Earnings Growth Forecast: 26.1% p.a.

Norbit ASA demonstrates strong growth potential, with earnings expected to grow significantly at 26.1% annually, outpacing the Norwegian market. Recent guidance for 2025 targets revenues between NOK 2.2 billion and NOK 2.3 billion, with improved EBIT margins supported by robust demand across segments like Oceans and PIR. The company has also secured substantial orders in the defence sector worth approximately NOK 260 million, enhancing its growth outlook despite seasonal fluctuations and currency impacts.

- Click here and access our complete growth analysis report to understand the dynamics of Norbit.

- Upon reviewing our latest valuation report, Norbit's share price might be too pessimistic.

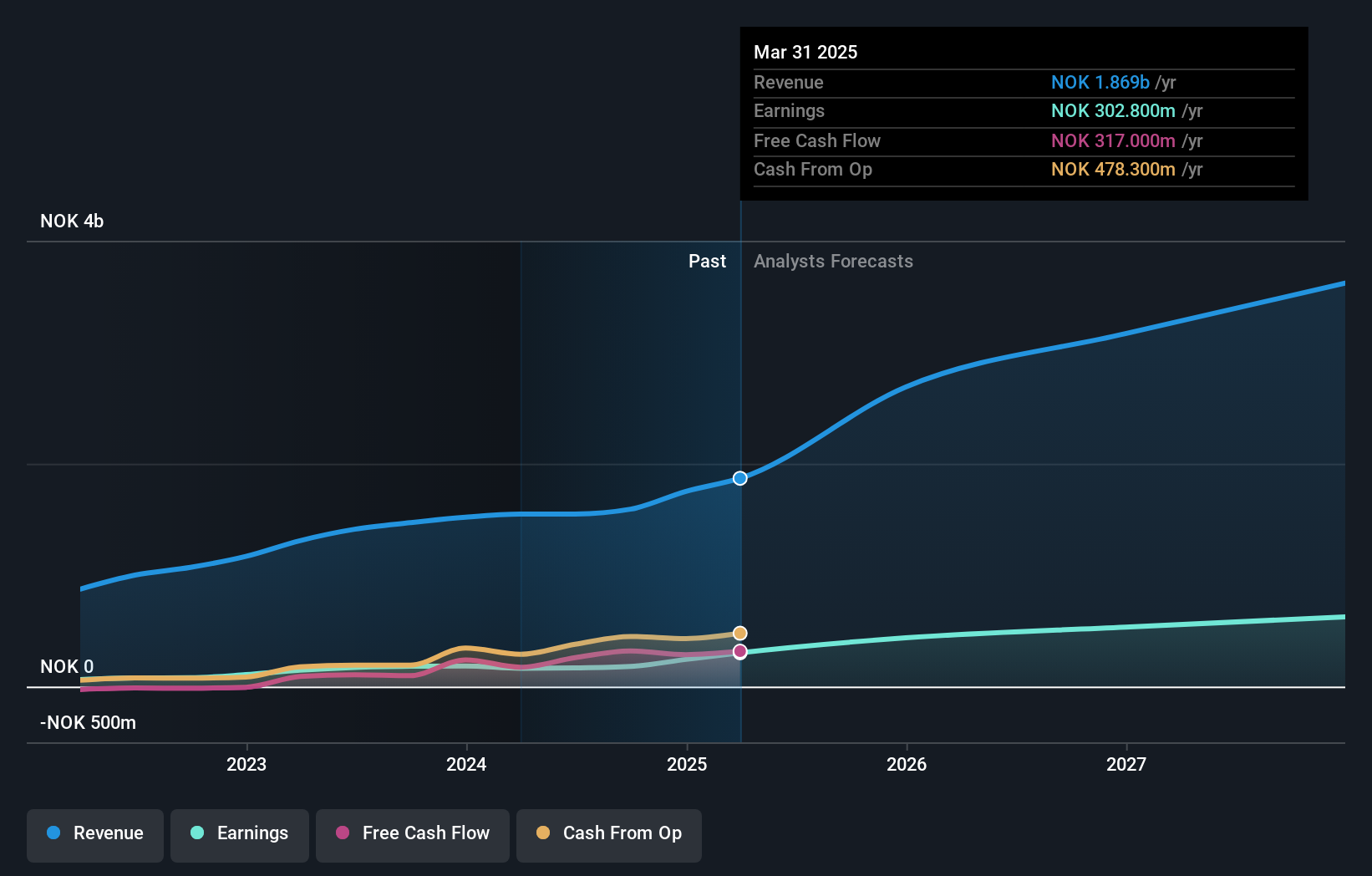

BICO Group (OM:BICO)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BICO Group AB (publ) offers hardware, laboratory automation, and software solutions across North America, Europe, Asia, and internationally with a market cap of SEK2.54 billion.

Operations: The company's revenue segments include Bioprinting with SEK369.30 million, Lab Automation at SEK571.60 million, and Life Science Solutions generating SEK1.01 billion.

Insider Ownership: 24.9%

Earnings Growth Forecast: 54.5% p.a.

BICO Group's recent financial performance shows a turnaround, with net income reaching SEK 346.8 million in Q4 2024 compared to a significant loss the previous year. Despite trading below its estimated fair value and showing good relative value compared to peers, BICO faces challenges with high share price volatility and low forecasted return on equity at 2.9%. Revenue growth of 7.2% annually is expected, outpacing the Swedish market but remaining below high-growth benchmarks.

- Navigate through the intricacies of BICO Group with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report BICO Group implies its share price may be lower than expected.

Bonesupport Holding (OM:BONEX)

Simply Wall St Growth Rating: ★★★★★★

Overview: Bonesupport Holding AB is an orthobiologics company that develops and sells injectable bio-ceramic bone graft substitutes globally, with a market cap of SEK20.50 billion.

Operations: The company's revenue is primarily derived from its Pharmaceuticals segment, amounting to SEK898.73 million.

Insider Ownership: 10.1%

Earnings Growth Forecast: 48.1% p.a.

Bonesupport Holding's growth trajectory is underscored by its high expected revenue growth of 29.5% annually, surpassing the Swedish market's average. Despite a decline in profit margins from 41.5% to 14.9%, its earnings are forecasted to grow significantly at 48.1% per year, outpacing the market average of 13.1%. The company recently reported strong sales figures and is advancing its product pipeline with CERAMENT® V seeking FDA approval, enhancing its competitive position in bone infection management solutions.

- Delve into the full analysis future growth report here for a deeper understanding of Bonesupport Holding.

- The valuation report we've compiled suggests that Bonesupport Holding's current price could be quite moderate.

Next Steps

- Navigate through the entire inventory of 215 Fast Growing European Companies With High Insider Ownership here.

- Interested In Other Possibilities? Trump has pledged to "unleash" American oil and gas and these 21 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if BICO Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:BICO

BICO Group

Provides hardware, laboratory automation, and software solutions in North America, Europe, Asia, and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor