Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies PetroNor E&P Ltd. (OB:PNOR) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for PetroNor E&P

What Is PetroNor E&P's Debt?

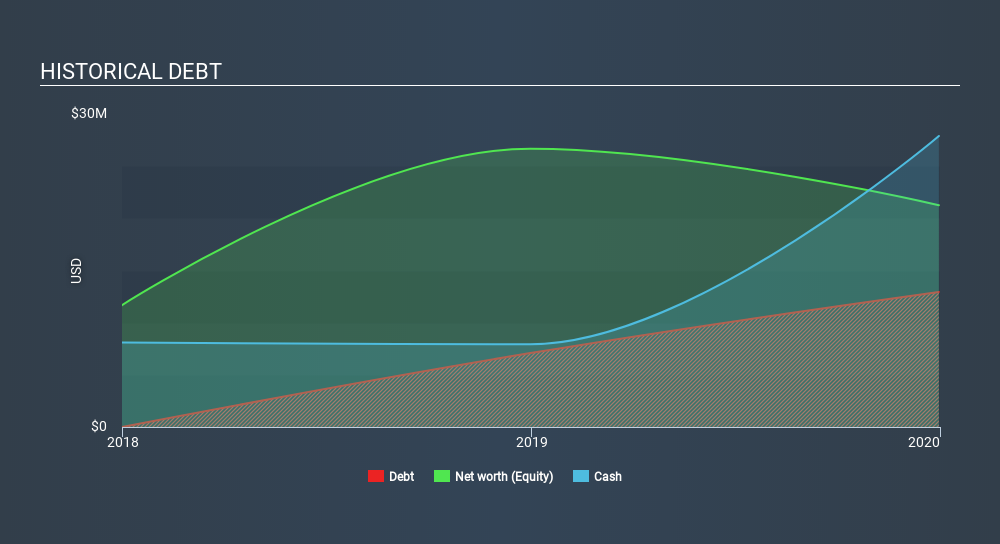

The image below, which you can click on for greater detail, shows that at December 2019 PetroNor E&P had debt of US$12.9m, up from US$7.08m in one year. But it also has US$27.9m in cash to offset that, meaning it has US$15.0m net cash.

A Look At PetroNor E&P's Liabilities

We can see from the most recent balance sheet that PetroNor E&P had liabilities of US$47.5m falling due within a year, and liabilities of US$14.4m due beyond that. On the other hand, it had cash of US$27.9m and US$24.8m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$9.25m.

Given PetroNor E&P has a market capitalization of US$84.3m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, PetroNor E&P boasts net cash, so it's fair to say it does not have a heavy debt load!

In fact PetroNor E&P's saving grace is its low debt levels, because its EBIT has tanked 48% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine PetroNor E&P's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While PetroNor E&P has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Looking at the most recent three years, PetroNor E&P recorded free cash flow of 29% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Summing up

Although PetroNor E&P's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$15.0m. So we are not troubled with PetroNor E&P's debt use. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for PetroNor E&P you should be aware of, and 1 of them is a bit unpleasant.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OB:PNOR

PetroNor E&P

Operates as an independent oil and gas exploration and production company in countries offshore West Africa.

Flawless balance sheet and good value.