Advertisement

Is Sarawak Consolidated Industries Berhad (KLSE:SCIB) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Sarawak Consolidated Industries Berhad (KLSE:SCIB) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Sarawak Consolidated Industries Berhad

What Is Sarawak Consolidated Industries Berhad's Debt?

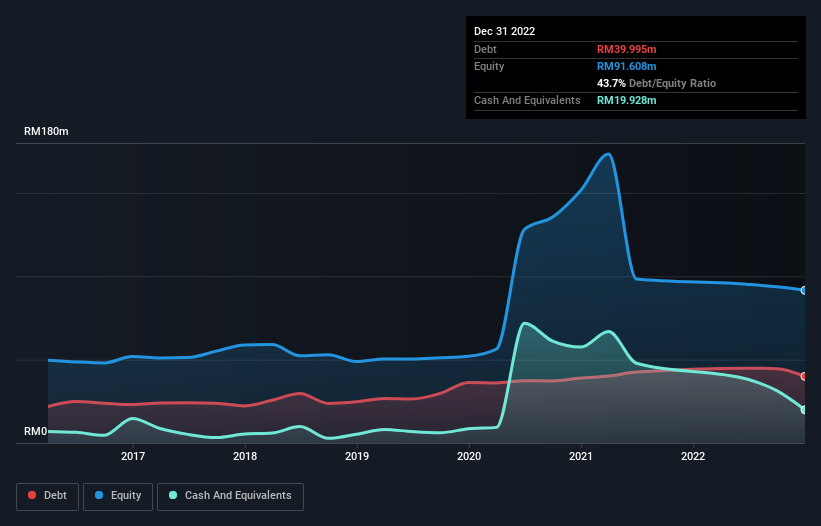

The image below, which you can click on for greater detail, shows that Sarawak Consolidated Industries Berhad had debt of RM40.0m at the end of December 2022, a reduction from RM44.9m over a year. However, it also had RM19.9m in cash, and so its net debt is RM20.1m.

A Look At Sarawak Consolidated Industries Berhad's Liabilities

The latest balance sheet data shows that Sarawak Consolidated Industries Berhad had liabilities of RM60.7m due within a year, and liabilities of RM24.5m falling due after that. Offsetting these obligations, it had cash of RM19.9m as well as receivables valued at RM76.0m due within 12 months. So it can boast RM10.7m more liquid assets than total liabilities.

This excess liquidity suggests that Sarawak Consolidated Industries Berhad is taking a careful approach to debt. Because it has plenty of assets, it is unlikely to have trouble with its lenders. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Sarawak Consolidated Industries Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Sarawak Consolidated Industries Berhad saw its revenue hold pretty steady, and it did not report positive earnings before interest and tax. While that's not too bad, we'd prefer see growth.

Caveat Emptor

Over the last twelve months Sarawak Consolidated Industries Berhad produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable RM50m at the EBIT level. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. But we'd want to see some positive free cashflow before spending much time on trying to understand the stock. So it seems too risky for our taste. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Sarawak Consolidated Industries Berhad you should be aware of, and 2 of them don't sit too well with us.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SCIB

Sarawak Consolidated Industries Berhad

An investment holding company, manufactures and sells precast concrete products and industrialized building systems for use in the infrastructure and construction industries primarily in Malaysia.

Slight risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor