- Malaysia

- /

- Trade Distributors

- /

- KLSE:SAMCHEM

A Rising Share Price Has Us Looking Closely At Samchem Holdings Berhad's (KLSE:SAMCHEM) P/E Ratio

Those holding Samchem Holdings Berhad (KLSE:SAMCHEM) shares must be pleased that the share price has rebounded 45% in the last thirty days. But unfortunately, the stock is still down by 21% over a quarter. But shareholders may not all be feeling jubilant, since the share price is still down 11% in the last year.

Assuming no other changes, a sharply higher share price makes a stock less attractive to potential buyers. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that deep value investors might steer clear when expectations of a company are too high. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). Investors have optimistic expectations of companies with higher P/E ratios, compared to companies with lower P/E ratios.

See our latest analysis for Samchem Holdings Berhad

Does Samchem Holdings Berhad Have A Relatively High Or Low P/E For Its Industry?

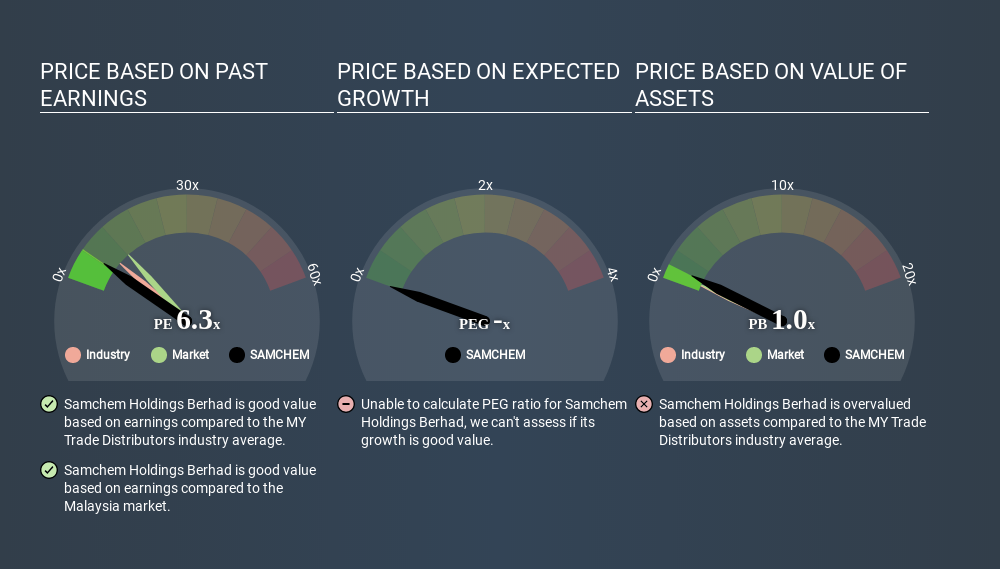

We can tell from its P/E ratio of 6.28 that sentiment around Samchem Holdings Berhad isn't particularly high. We can see in the image below that the average P/E (8.9) for companies in the trade distributors industry is higher than Samchem Holdings Berhad's P/E.

This suggests that market participants think Samchem Holdings Berhad will underperform other companies in its industry. Since the market seems unimpressed with Samchem Holdings Berhad, it's quite possible it could surprise on the upside. If you consider the stock interesting, further research is recommended. For example, I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. When earnings grow, the 'E' increases, over time. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. Then, a lower P/E should attract more buyers, pushing the share price up.

It's great to see that Samchem Holdings Berhad grew EPS by 11% in the last year. And its annual EPS growth rate over 5 years is 32%. This could arguably justify a relatively high P/E ratio.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

The 'Price' in P/E reflects the market capitalization of the company. In other words, it does not consider any debt or cash that the company may have on the balance sheet. The exact same company would hypothetically deserve a higher P/E ratio if it had a strong balance sheet, than if it had a weak one with lots of debt, because a cashed up company can spend on growth.

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

How Does Samchem Holdings Berhad's Debt Impact Its P/E Ratio?

Samchem Holdings Berhad has net debt worth 82% of its market capitalization. This is enough debt that you'd have to make some adjustments before using the P/E ratio to compare it to a company with net cash.

The Verdict On Samchem Holdings Berhad's P/E Ratio

Samchem Holdings Berhad's P/E is 6.3 which is below average (12.2) in the MY market. The company may have significant debt, but EPS growth was good last year. If the company can continue to grow earnings, then the current P/E may be unjustifiably low. What we know for sure is that investors are becoming less uncomfortable about Samchem Holdings Berhad's prospects, since they have pushed its P/E ratio from 4.3 to 6.3 over the last month. For those who like to invest in turnarounds, that might mean it's time to put the stock on a watchlist, or research it. But others might consider the opportunity to have passed.

Investors should be looking to buy stocks that the market is wrong about. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About KLSE:SAMCHEM

Samchem Holdings Berhad

An investment holding company, distributes industrial chemicals in Malaysia, Indonesia, Vietnam, and Singapore.

Solid track record with excellent balance sheet and pays a dividend.