Stock Analysis

- Malaysia

- /

- Construction

- /

- KLSE:LFECORP

Investors Appear Satisfied With LFE Corporation Berhad's (KLSE:LFECORP) Prospects As Shares Rocket 29%

LFE Corporation Berhad (KLSE:LFECORP) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. The last 30 days bring the annual gain to a very sharp 83%.

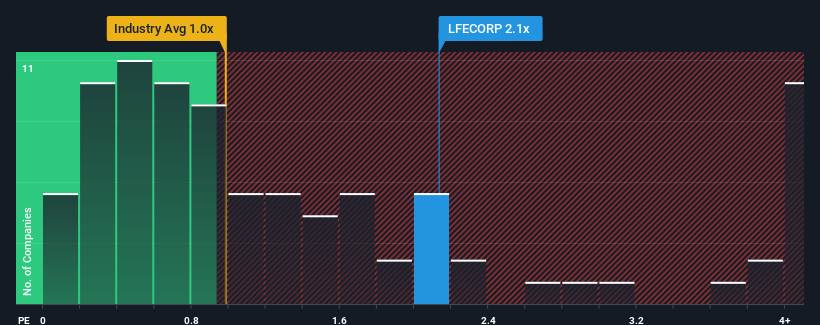

After such a large jump in price, you could be forgiven for thinking LFE Corporation Berhad is a stock not worth researching with a price-to-sales ratios (or "P/S") of 2.1x, considering almost half the companies in Malaysia's Construction industry have P/S ratios below 1x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for LFE Corporation Berhad

How Has LFE Corporation Berhad Performed Recently?

With revenue growth that's exceedingly strong of late, LFE Corporation Berhad has been doing very well. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on LFE Corporation Berhad's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For LFE Corporation Berhad?

LFE Corporation Berhad's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 56% last year. This great performance means it was also able to deliver immense revenue growth over the last three years. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 13% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this in consideration, it's not hard to understand why LFE Corporation Berhad's P/S is high relative to its industry peers. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the wider industry.

What We Can Learn From LFE Corporation Berhad's P/S?

LFE Corporation Berhad's P/S is on the rise since its shares have risen strongly. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of LFE Corporation Berhad revealed its three-year revenue trends are contributing to its high P/S, given they look better than current industry expectations. At this stage investors feel the potential continued revenue growth in the future is great enough to warrant an inflated P/S. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

We don't want to rain on the parade too much, but we did also find 3 warning signs for LFE Corporation Berhad that you need to be mindful of.

If these risks are making you reconsider your opinion on LFE Corporation Berhad, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're helping make it simple.

Find out whether LFE Corporation Berhad is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:LFECORP

LFE Corporation Berhad

An investment holding company, engages in the provision of construction, mechanical, and electrical services in Malaysia.

Flawless balance sheet with solid track record.