- Mexico

- /

- Infrastructure

- /

- BMV:GAP B

Is Grupo Aeroportuario del Pacífico. de (BMV:GAPB) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Grupo Aeroportuario del Pacífico, S.A.B. de C.V. (BMV:GAPB) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Grupo Aeroportuario del Pacífico. de

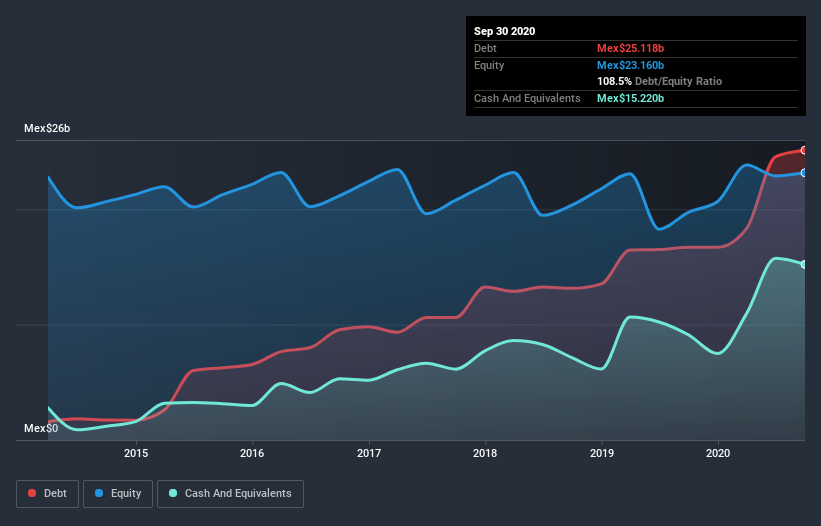

What Is Grupo Aeroportuario del Pacífico. de's Debt?

The image below, which you can click on for greater detail, shows that at September 2020 Grupo Aeroportuario del Pacífico. de had debt of Mex$25.1b, up from Mex$16.7b in one year. However, because it has a cash reserve of Mex$15.2b, its net debt is less, at about Mex$9.90b.

How Strong Is Grupo Aeroportuario del Pacífico. de's Balance Sheet?

According to the last reported balance sheet, Grupo Aeroportuario del Pacífico. de had liabilities of Mex$8.34b due within 12 months, and liabilities of Mex$20.7b due beyond 12 months. Offsetting this, it had Mex$15.2b in cash and Mex$2.29b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by Mex$11.5b.

Since publicly traded Grupo Aeroportuario del Pacífico. de shares are worth a total of Mex$103.9b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Grupo Aeroportuario del Pacífico. de has net debt worth 1.5 times EBITDA, which isn't too much, but its interest cover looks a bit on the low side, with EBIT at only 5.1 times the interest expense. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. Shareholders should be aware that Grupo Aeroportuario del Pacífico. de's EBIT was down 43% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Grupo Aeroportuario del Pacífico. de can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Grupo Aeroportuario del Pacífico. de recorded free cash flow worth 61% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Based on what we've seen Grupo Aeroportuario del Pacífico. de is not finding it easy, given its EBIT growth rate, but the other factors we considered give us cause to be optimistic. There's no doubt that it has an adequate capacity to convert EBIT to free cash flow. It's also worth noting that Grupo Aeroportuario del Pacífico. de is in the Infrastructure industry, which is often considered to be quite defensive. When we consider all the factors mentioned above, we do feel a bit cautious about Grupo Aeroportuario del Pacífico. de's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Grupo Aeroportuario del Pacífico. de is showing 3 warning signs in our investment analysis , and 1 of those is significant...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

When trading Grupo Aeroportuario del Pacífico. de or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BMV:GAP B

Grupo Aeroportuario del Pacífico. de

Grupo Aeroportuario del Pacífico, S.A.B. de C.V., together with its subsidiaries, holds concessions to develop, operate, and manage airports in Mexico and Jamaica.

Reasonable growth potential with acceptable track record.