- South Korea

- /

- Pharma

- /

- KOSE:A009420

KRX Stocks That May Be Undervalued In October 2024

Reviewed by Simply Wall St

Over the last 7 days, the South Korean market has remained flat, mirroring its performance over the past 12 months. In this context of stability and anticipated annual earnings growth of 30%, identifying undervalued stocks can offer potential opportunities for investors looking to capitalize on future gains.

Top 10 Undervalued Stocks Based On Cash Flows In South Korea

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Samwha ElectricLtd (KOSE:A009470) | ₩49200.00 | ₩92753.28 | 47% |

| APR (KOSE:A278470) | ₩266500.00 | ₩521631.47 | 48.9% |

| T'Way Air (KOSE:A091810) | ₩3070.00 | ₩5679.43 | 45.9% |

| SK Biopharmaceuticals (KOSE:A326030) | ₩104000.00 | ₩179969.09 | 42.2% |

| Lutronic (KOSDAQ:A085370) | ₩36700.00 | ₩63217.94 | 41.9% |

| ABCO Electronics (KOSDAQ:A036010) | ₩5810.00 | ₩11479.52 | 49.4% |

| Oscotec (KOSDAQ:A039200) | ₩34700.00 | ₩65156.22 | 46.7% |

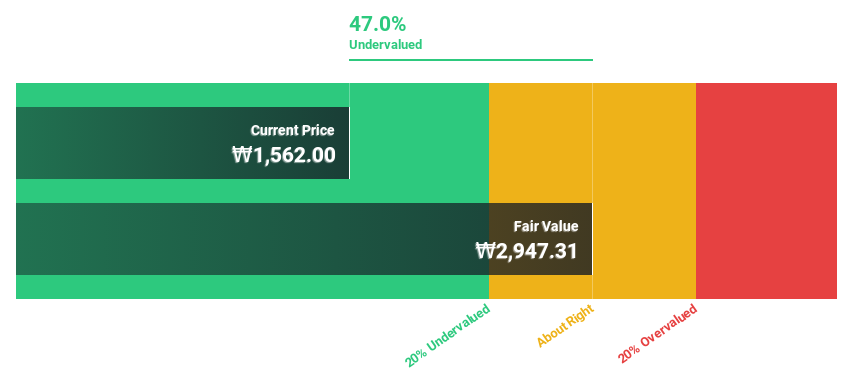

| Shinsung E&GLtd (KOSE:A011930) | ₩1691.00 | ₩2999.67 | 43.6% |

| Hotel ShillaLtd (KOSE:A008770) | ₩47800.00 | ₩82599.96 | 42.1% |

| Kakao Games (KOSDAQ:A293490) | ₩17500.00 | ₩29941.46 | 41.6% |

Underneath we present a selection of stocks filtered out by our screen.

SK hynix (KOSE:A000660)

Overview: SK hynix Inc., along with its subsidiaries, manufactures, distributes, and sells semiconductor products across Korea, China, the rest of Asia, the United States, and Europe with a market cap of ₩120.23 trillion.

Operations: The company generated ₩49.22 billion from the manufacture and sale of semiconductor products.

Estimated Discount To Fair Value: 15.1%

SK hynix is currently trading 15.1% below its estimated fair value of ₩205,748.53, with significant earnings growth forecast at 49.2% per year, outpacing the KR market's 29.7%. Recent financial results show a strong turnaround from a net loss to a net income of ₩4.12 trillion for Q2 2024, driven by high-quality earnings and new product developments like the GDDR7 graphics memory enhancing future cash flows and profitability potential.

- In light of our recent growth report, it seems possible that SK hynix's financial performance will exceed current levels.

- Click to explore a detailed breakdown of our findings in SK hynix's balance sheet health report.

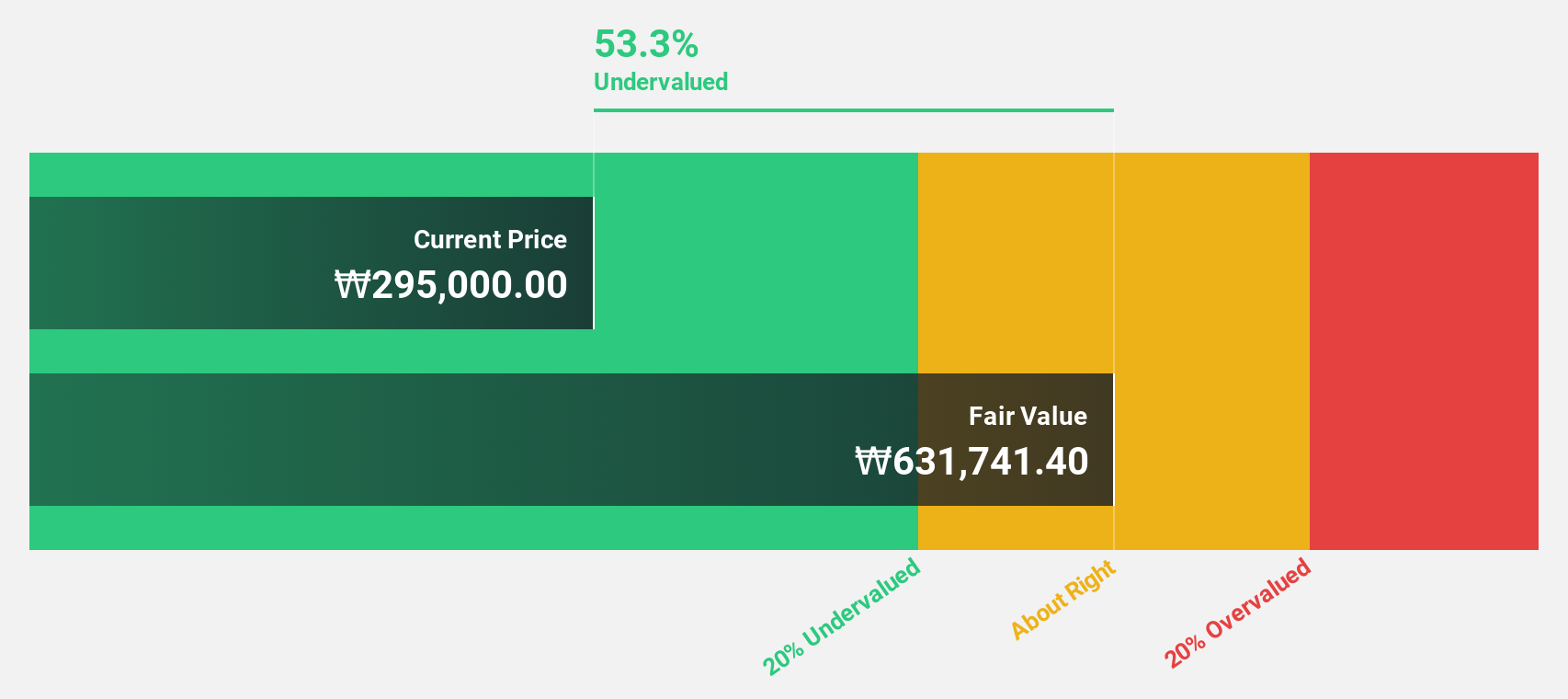

Hanall Biopharma (KOSE:A009420)

Overview: Hanall Biopharma Co., Ltd. is a pharmaceutical company that manufactures and sells pharmaceutical products in South Korea and internationally, with a market cap of ₩1.96 trillion.

Operations: The company generates revenue of ₩130.37 billion from the manufacture and sale of pharmaceuticals.

Estimated Discount To Fair Value: 28.5%

Hanall Biopharma is trading at ₩38,750, significantly below its estimated fair value of ₩54,214.67. Earnings are forecast to grow 93.89% annually and the company is expected to become profitable within three years, outperforming average market growth. Despite a recent net loss of ₩3.32 billion in Q2 2024 and declining sales, analysts predict a 31.6% stock price increase due to strategic leadership changes and anticipated revenue growth outpacing the KR market at 16% per year.

- Our comprehensive growth report raises the possibility that Hanall Biopharma is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of Hanall Biopharma.

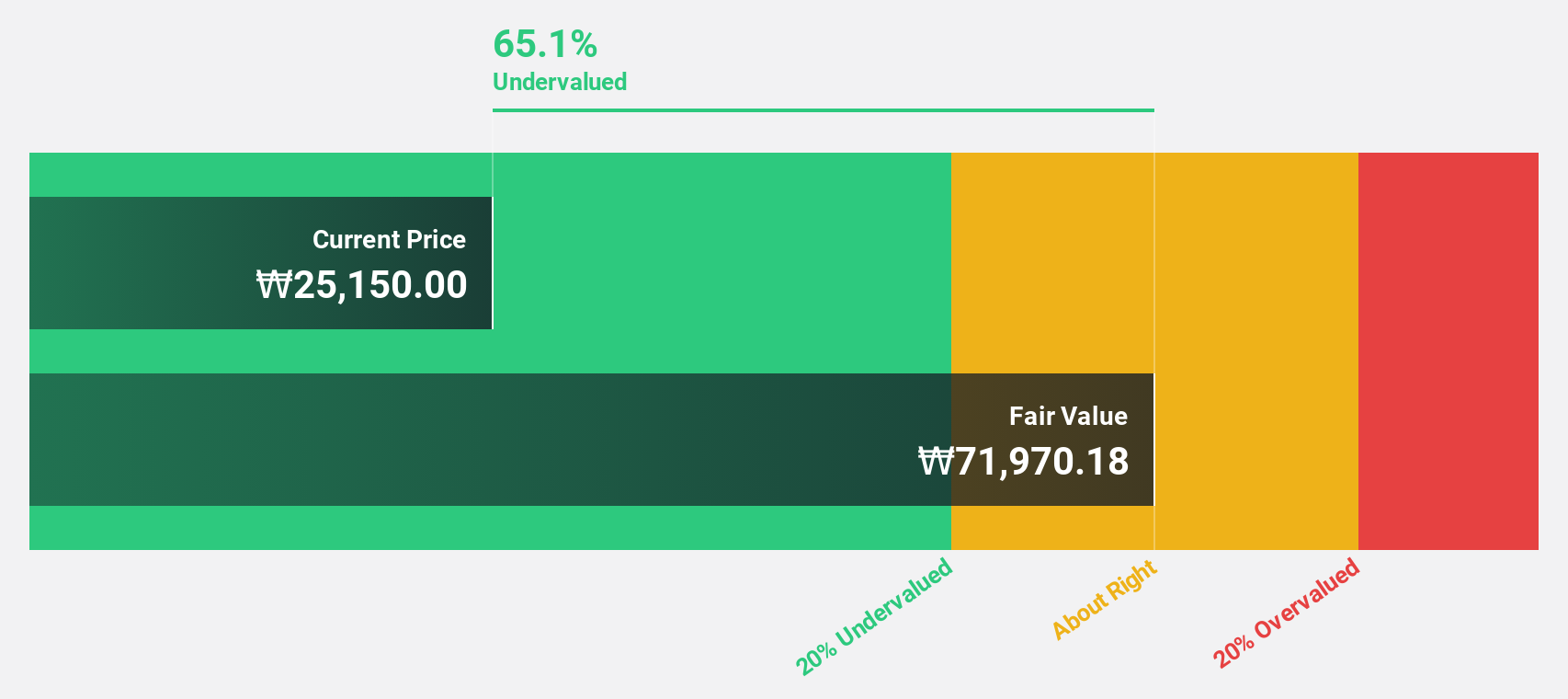

Shinsung E&GLtd (KOSE:A011930)

Overview: Shinsung E&G Co., Ltd. provides solar modules and solar systems in Korea and internationally, with a market cap of ₩344.23 billion.

Operations: The company generates revenue primarily from its Clean Environment Business Division, contributing ₩532.80 billion, followed by the Renewable Energy Business Division at ₩41.38 billion.

Estimated Discount To Fair Value: 43.6%

Shinsung E&G Ltd. is trading at ₩1691, significantly below its estimated fair value of ₩2999.67, indicating strong undervaluation based on discounted cash flow analysis. Despite interest payments not being well-covered by earnings, the company’s revenue is forecast to grow 16.6% annually, outpacing the KR market's 10.5%. Earnings are expected to grow at 108.51% per year with profitability anticipated within three years, making it a compelling investment relative to peers and industry standards.

- The growth report we've compiled suggests that Shinsung E&GLtd's future prospects could be on the up.

- Dive into the specifics of Shinsung E&GLtd here with our thorough financial health report.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 31 Undervalued KRX Stocks Based On Cash Flows now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanall Biopharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A009420

Hanall Biopharma

A pharmaceutical company, manufactures and sells pharmaceutical products in South Korea and internationally.

Flawless balance sheet with reasonable growth potential.