- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A323280

Sammok S-FormLtd And 2 Other Undiscovered Gems In South Korea

Reviewed by Simply Wall St

Over the last 7 days, the South Korean market has experienced a 1.4% drop, while remaining flat over the past year, with expectations for earnings growth of 30% per annum in the coming years. In this environment, identifying stocks like Sammok S-Form Ltd that are positioned to capitalize on future growth opportunities can be crucial for investors seeking to uncover potential gems in a steady market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Korea Cast Iron Pipe Ind | NA | 1.97% | 8.84% | ★★★★★★ |

| Samyang | 49.49% | 6.68% | 23.96% | ★★★★★★ |

| Korea Airport ServiceLtd | NA | 3.97% | 42.22% | ★★★★★★ |

| Korea Ratings | NA | 1.13% | 0.54% | ★★★★★★ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| ASIA Holdings | 34.98% | 8.43% | 16.17% | ★★★★★☆ |

| Daewon Cable | 30.50% | 8.72% | 60.28% | ★★★★★☆ |

| Itcen | 64.57% | 14.33% | -24.39% | ★★★★★☆ |

| FnGuide | 36.10% | 8.92% | 10.27% | ★★★★☆☆ |

| THINKWARE | 36.75% | 21.25% | 22.92% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

Sammok S-FormLtd (KOSDAQ:A018310)

Simply Wall St Value Rating: ★★★★★☆

Overview: Sammok S-Form Co., Ltd manufactures, sells, and leases formwork for construction and civil engineering works in South Korea and internationally, with a market cap of ₩398.10 billion.

Operations: The company's primary revenue stream is from the manufacture of structural metal products, generating ₩457.90 billion.

Sammok S-FormLtd, a smaller player in its sector, has shown impressive financial health with earnings growing by 75% over the past year, outpacing the building industry's 28.5%. The company trades at a value that is 10.1% below its estimated fair value, suggesting potential upside for investors. With more cash than total debt and high-quality past earnings, Sammok S-FormLtd seems well-positioned financially without concerns about cash runway or interest coverage.

- Unlock comprehensive insights into our analysis of Sammok S-FormLtd stock in this health report.

Assess Sammok S-FormLtd's past performance with our detailed historical performance reports.

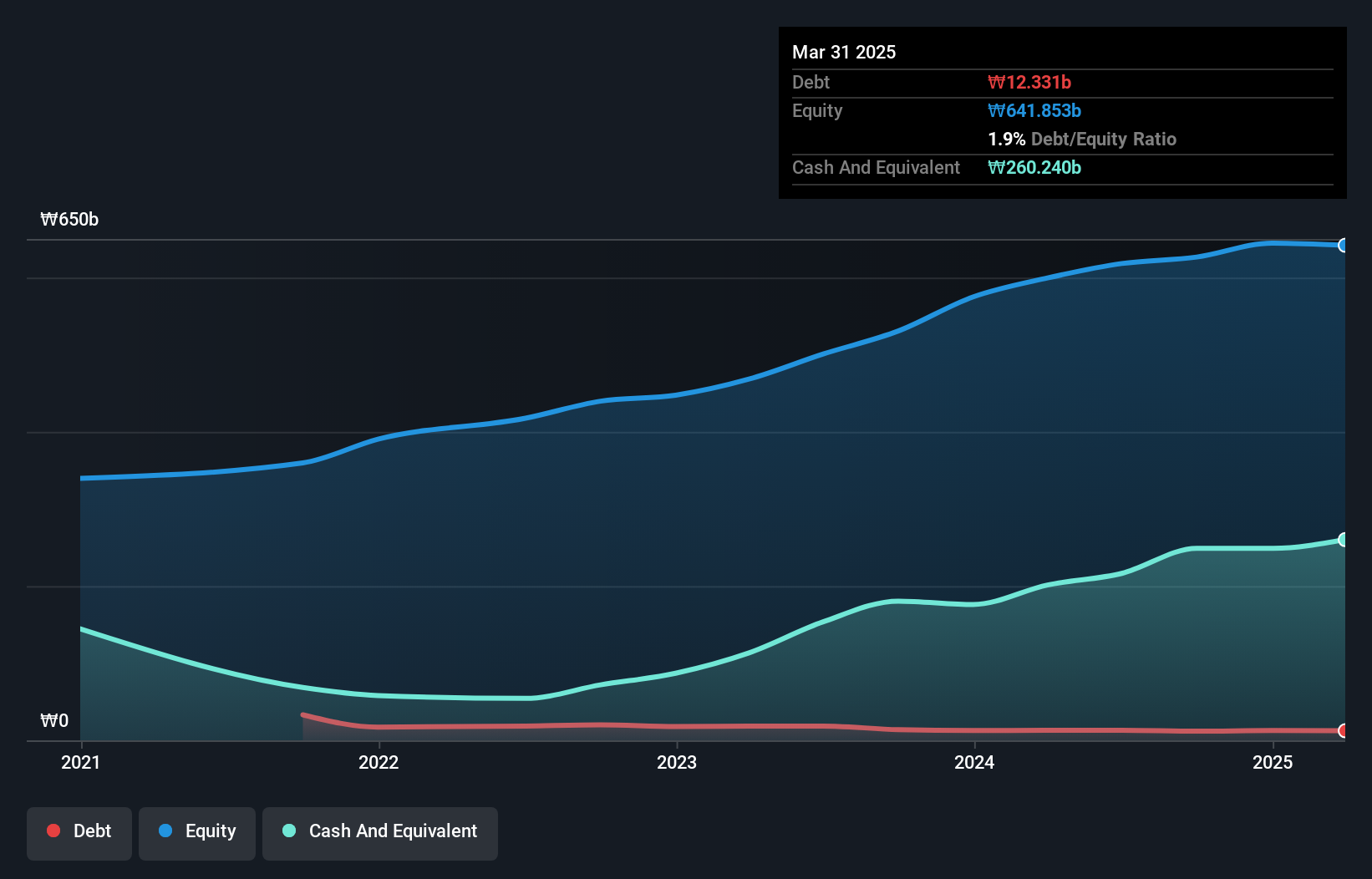

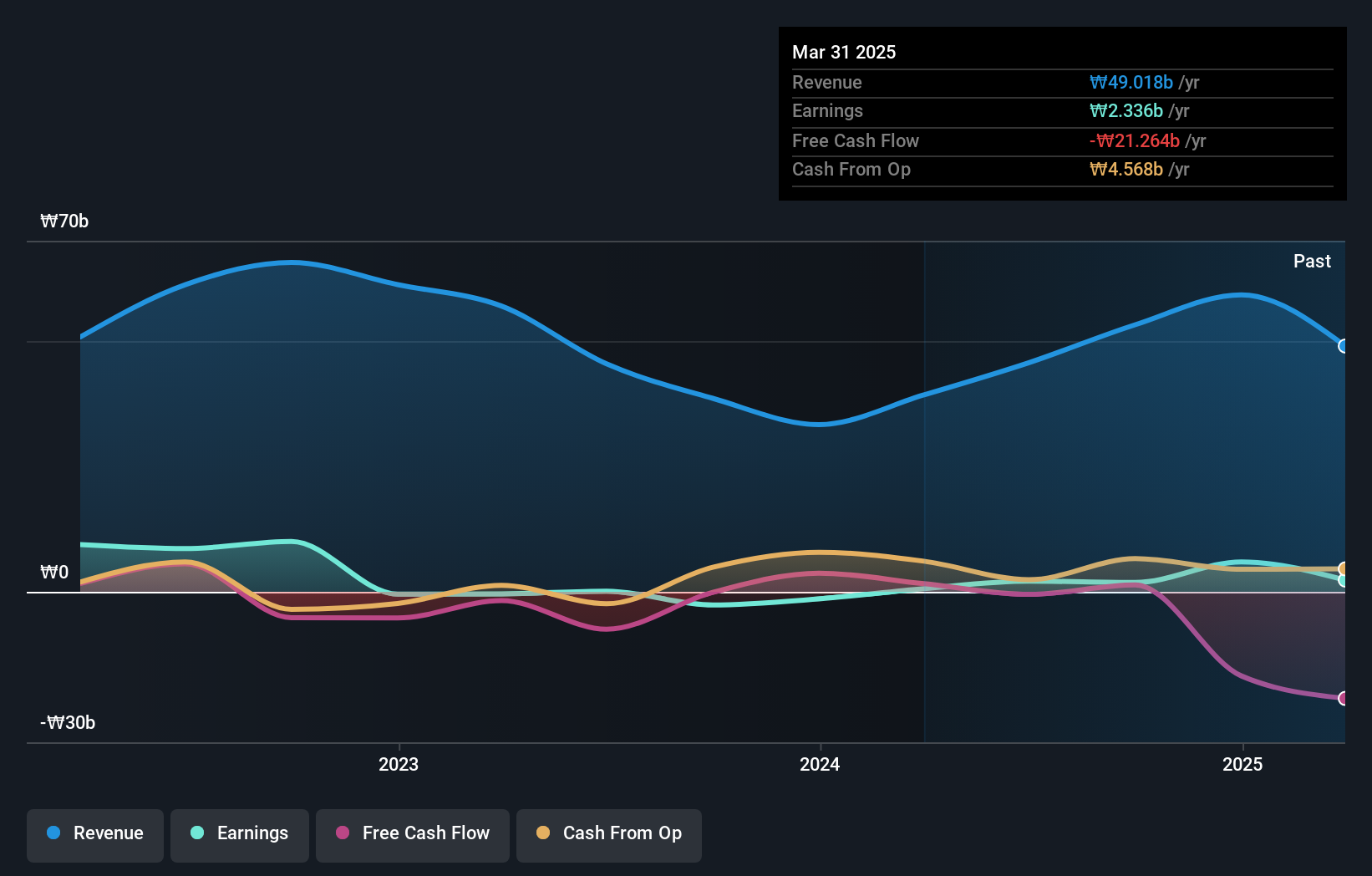

TaesungLtd (KOSDAQ:A323280)

Simply Wall St Value Rating: ★★★★★☆

Overview: Taesung Co., Ltd. is engaged in the development, manufacturing, and sale of PCB automation equipment both domestically in South Korea and internationally, with a market capitalization of approximately ₩743.64 billion.

Operations: Taesung's primary revenue stream is from the manufacturing and sale of PCB automation equipment, generating approximately ₩45.68 billion.

Taesung Ltd., a small player in the semiconductor industry, has shown impressive earnings growth of 1482% over the past year, significantly outpacing its industry peers. The company's debt management appears robust with an interest coverage ratio of 17.5 times and a net debt to equity ratio at a satisfactory 4%. Despite recent volatility in share price, Taesung's inclusion in the S&P Global BMI Index highlights its growing recognition.

- Click to explore a detailed breakdown of our findings in TaesungLtd's health report.

Gain insights into TaesungLtd's historical performance by reviewing our past performance report.

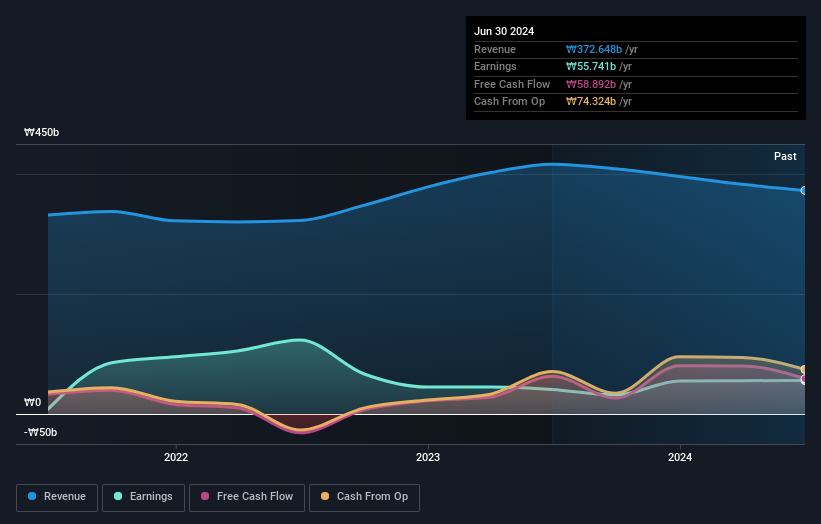

sindohLtd (KOSE:A029530)

Simply Wall St Value Rating: ★★★★★☆

Overview: Sindoh Co., Ltd. is engaged in the manufacturing and sale of printers, multi-functional machines, and office solutions both in Korea and internationally, with a market cap of ₩363.02 billion.

Operations: Sindoh Co., Ltd. generates its revenue primarily from the manufacturing segment, which accounts for ₩372.65 billion. The company's net profit margin is a key financial indicator to consider when evaluating its profitability and cost efficiency within this segment.

Sindoh Ltd. has shown impressive earnings growth of 36.6% over the past year, outpacing the tech industry average of -1.1%. The company is trading at 72.6% below its estimated fair value, suggesting potential undervaluation in the market. Additionally, Sindoh's debt-to-equity ratio has slightly increased from 0.9% to 1% over five years, yet it remains manageable with more cash than total debt on hand and high-quality earnings reported consistently.

- Dive into the specifics of sindohLtd here with our thorough health report.

Explore historical data to track sindohLtd's performance over time in our Past section.

Key Takeaways

- Click this link to deep-dive into the 185 companies within our KRX Undiscovered Gems With Strong Fundamentals screener.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TaesungLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A323280

TaesungLtd

Develops, manufactures, and sells PCB automation equipment in South Korea and internationally.

Excellent balance sheet with acceptable track record.