Advertisement

- South Korea

- /

- Biotech

- /

- KOSDAQ:A256840

We Think You Can Look Beyond BNC Korea's (KOSDAQ:256840) Lackluster Earnings

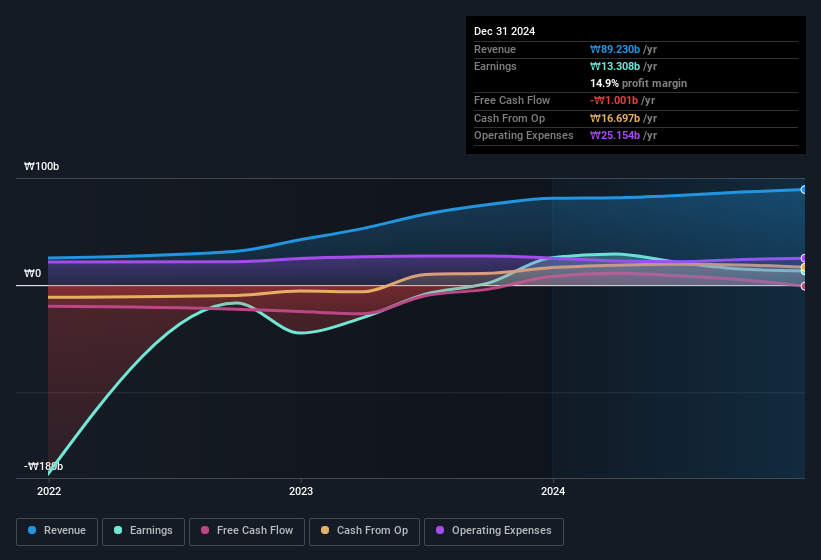

Shareholders appeared unconcerned with BNC Korea Co., Ltd.'s (KOSDAQ:256840) lackluster earnings report last week. Our analysis suggests that while the profits are soft, the foundations of the business are strong.

How Do Unusual Items Influence Profit?

Importantly, our data indicates that BNC Korea's profit was reduced by ₩6.3b, due to unusual items, over the last year. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And that's hardly a surprise given these line items are considered unusual. In the twelve months to December 2024, BNC Korea had a big unusual items expense. As a result, we can surmise that the unusual items made its statutory profit significantly weaker than it would otherwise be.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of BNC Korea.

Our Take On BNC Korea's Profit Performance

As we mentioned previously, the BNC Korea's profit was hampered by unusual items in the last year. Because of this, we think BNC Korea's underlying earnings potential is as good as, or possibly even better, than the statutory profit makes it seem! Unfortunately, though, its earnings per share actually fell back over the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. At Simply Wall St, we found 2 warning signs for BNC Korea and we think they deserve your attention.

Today we've zoomed in on a single data point to better understand the nature of BNC Korea's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if BNC Korea might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A256840

BNC Korea

Engages in the research and development, production, and sale of biomaterials for medicines in South Korea, Europe, China, Brazil, India, Indonesia, and Internationally.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor