Stock Analysis

- South Korea

- /

- Biotech

- /

- KOSDAQ:A086900

KRX Growth Companies With High Insider Ownership In July 2024

Reviewed by Simply Wall St

The South Korean stock market has recently experienced a downturn, with the KOSPI declining over several sessions. Despite this slump, there is a positive global outlook that suggests potential for recovery, particularly in technology sectors. In such a market environment, growth companies with high insider ownership can be particularly compelling as these insiders often have a deep commitment to their companies' long-term success.

Top 10 Growth Companies With High Insider Ownership In South Korea

| Name | Insider Ownership | Earnings Growth |

| ALTEOGEN (KOSDAQ:A196170) | 26.6% | 73.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 36.4% |

| Global Tax Free (KOSDAQ:A204620) | 18.1% | 72.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 29.8% | 58.7% |

| Park Systems (KOSDAQ:A140860) | 33% | 36.3% |

| Vuno (KOSDAQ:A338220) | 19.5% | 105% |

| UTI (KOSDAQ:A179900) | 33.1% | 122.7% |

| INTEKPLUS (KOSDAQ:A064290) | 16.3% | 77.4% |

| HANA Micron (KOSDAQ:A067310) | 20% | 99.6% |

| Techwing (KOSDAQ:A089030) | 18.7% | 77.8% |

Let's review some notable picks from our screened stocks.

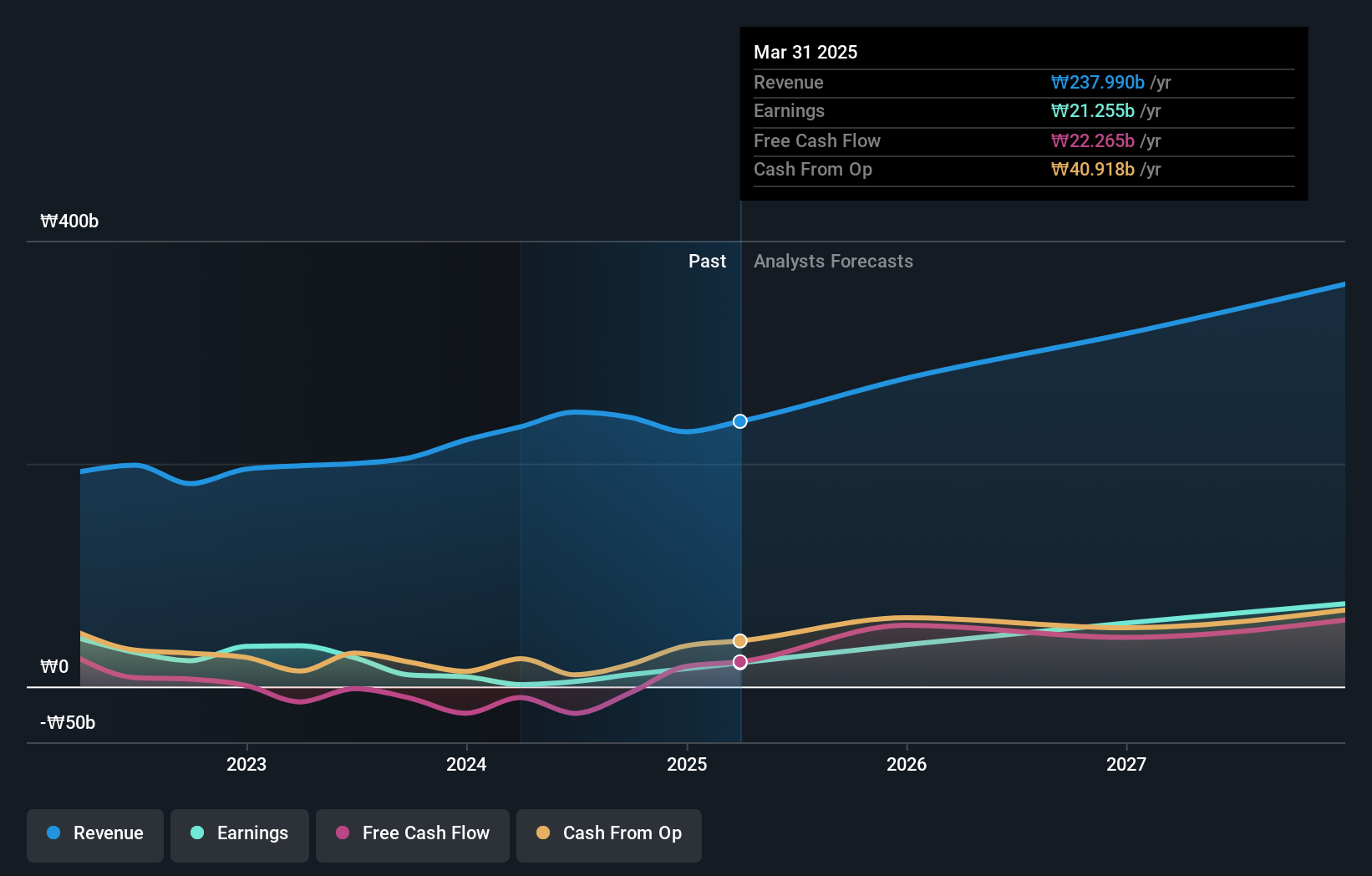

Medy-Tox (KOSDAQ:A086900)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Medy-Tox Inc. is a biopharmaceutical company based in South Korea, with a market capitalization of approximately ₩1.18 billion.

Operations: The revenue segments for the company are not specified in the provided text.

Insider Ownership: 19.8%

Earnings Growth Forecast: 68.3% p.a.

Medy-Tox, despite recent challenges with a significant drop in earnings and a shift from net income to a net loss as reported in May 2024, is positioned for potential growth. The company's revenue and earnings are expected to grow at 12.4% and 68.33% per year respectively, outpacing the South Korean market forecasts. However, its current profit margins are notably lower than the previous year, reflecting ongoing operational struggles. Trading significantly below estimated fair value suggests potential undervaluation amidst volatility.

- Get an in-depth perspective on Medy-Tox's performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility Medy-Tox's shares may be trading at a discount.

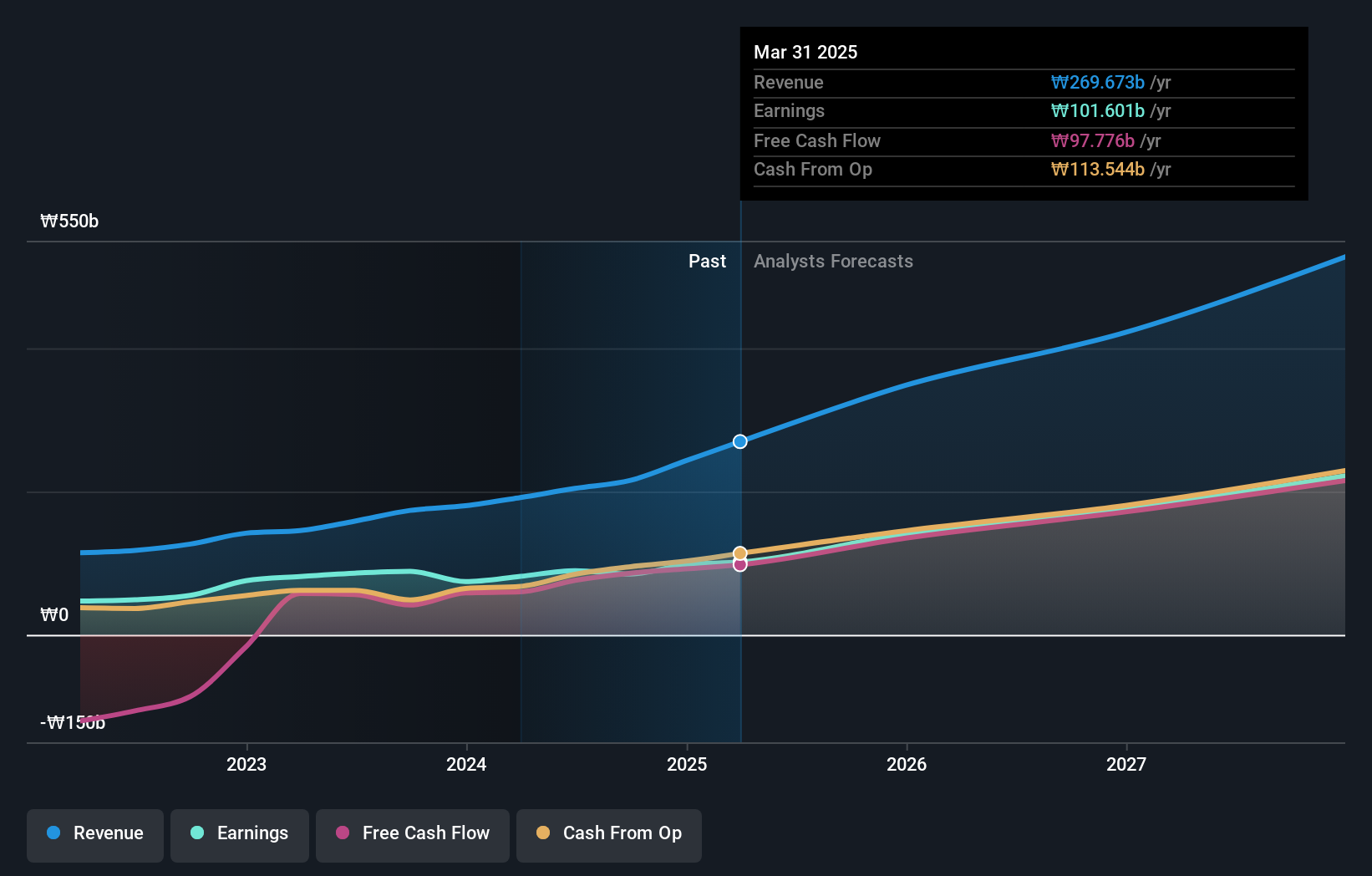

Seegene (KOSDAQ:A096530)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Seegene, Inc. is a global manufacturer and seller of molecular diagnostics products, with a market capitalization of approximately ₩995.86 billion.

Operations: The company generates its revenue primarily from the sale of diagnostic kits and equipment, totaling approximately ₩367.27 billion.

Insider Ownership: 35.7%

Earnings Growth Forecast: 129.2% p.a.

Seegene, despite a recent shift from net income to a net loss in Q1 2024, displays potential for growth with expected annual revenue increases outpacing the South Korean market at 13.1% per year. The company's earnings are also forecasted to grow significantly. However, its dividend coverage is weak, reflecting financial strain. Recently extending its buyback plan suggests confidence in future stability and value, aligning with substantial insider ownership that underscores commitment to the company’s success.

- Navigate through the intricacies of Seegene with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that Seegene's current price could be quite moderate.

CLASSYS (KOSDAQ:A214150)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CLASSYS Inc. specializes in the provision of medical aesthetics devices globally, with a market capitalization of approximately ₩3.06 billion.

Operations: The company generates revenue primarily from the surgical and medical equipment segment, totaling approximately ₩191.53 billion.

Insider Ownership: 10.1%

Earnings Growth Forecast: 22.5% p.a.

CLASSYS, a South Korean growth company with high insider ownership, has demonstrated robust performance with earnings growing 25.9% annually over the past five years. The company's revenue is expected to grow at 21.5% per year, outpacing the domestic market's average. Despite a highly volatile share price recently, CLASSYS maintains strong future prospects with significant earnings growth anticipated over the next three years and a forecasted high return on equity of 28.1%. Recent active participation in multiple global investment conferences underscores its strategic outreach and potential for continued expansion.

- Unlock comprehensive insights into our analysis of CLASSYS stock in this growth report.

- According our valuation report, there's an indication that CLASSYS' share price might be on the expensive side.

Taking Advantage

- Gain an insight into the universe of 79 Fast Growing KRX Companies With High Insider Ownership by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Medy-Tox is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A086900

Flawless balance sheet and good value.