Advertisement

- South Korea

- /

- Consumer Services

- /

- KOSE:A019680

We Wouldn't Be Too Quick To Buy Daekyo Co., Ltd. (KRX:019680) Before It Goes Ex-Dividend

It looks like Daekyo Co., Ltd. (KRX:019680) is about to go ex-dividend in the next 2 days. Ex-dividend means that investors that purchase the stock on or after the 27th of December will not receive this dividend, which will be paid on the 28th of March.

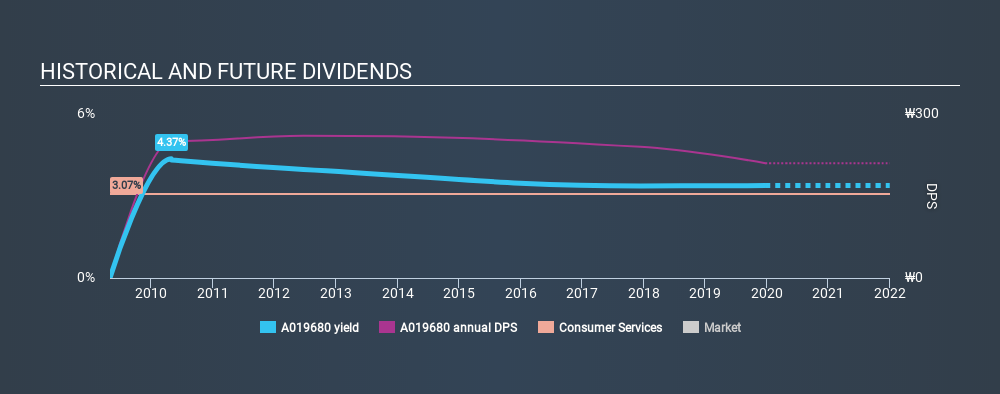

Daekyo's upcoming dividend is ₩110 a share, following on from the last 12 months, when the company distributed a total of ₩210 per share to shareholders. Looking at the last 12 months of distributions, Daekyo has a trailing yield of approximately 3.4% on its current stock price of ₩6210. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

View our latest analysis for Daekyo

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Daekyo paid out 196% of profit in the past year, which we think is typically not sustainable unless there are mitigating characteristics such as unusually strong cash flow or a large cash balance. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. It distributed 33% of its free cash flow as dividends, a comfortable payout level for most companies.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Daekyo fortunately did generate enough cash to fund its dividend. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Very few companies are able to sustainably pay dividends larger than their reported earnings.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. With that in mind, we're discomforted by Daekyo's 22% per annum decline in earnings in the past five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Daekyo has seen its dividend decline 1.7% per annum on average over the past ten years, which is not great to see.

To Sum It Up

Should investors buy Daekyo for the upcoming dividend? It's never great to see earnings per share declining, especially when a company is paying out 196% of its profit as dividends, which we feel is uncomfortably high. However, the cash payout ratio was much lower - good news from a dividend perspective - which makes us wonder why there is such a mis-match between income and cashflow. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

Curious what other investors think of Daekyo? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About KOSE:A019680

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor