- South Korea

- /

- Trade Distributors

- /

- KOSE:A005440

Undiscovered Gems in South Korea for September 2024

Reviewed by Simply Wall St

Over the last 7 days, the South Korean market has dropped 4.2%, and while its performance has been flat over the past year, earnings are expected to grow by 29% per annum over the next few years. In this environment, identifying stocks with strong growth potential and solid fundamentals becomes crucial for investors looking to capitalize on future opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Korea Airport ServiceLtd | NA | 3.97% | 42.22% | ★★★★★★ |

| NOROO PAINT & COATINGS | 13.99% | 5.04% | 7.98% | ★★★★★★ |

| Korea Cast Iron Pipe Ind | NA | 1.97% | 8.84% | ★★★★★★ |

| Samyang | 49.49% | 6.68% | 23.96% | ★★★★★★ |

| Woori Technology Investment | NA | 22.60% | -1.67% | ★★★★★★ |

| ONEJOON | 10.13% | 35.30% | -5.78% | ★★★★★☆ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| ASIA Holdings | 34.98% | 8.43% | 16.17% | ★★★★★☆ |

| Oriental Precision & EngineeringLtd | 54.53% | 3.14% | 0.80% | ★★★★★☆ |

| FnGuide | 36.10% | 8.92% | 10.27% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

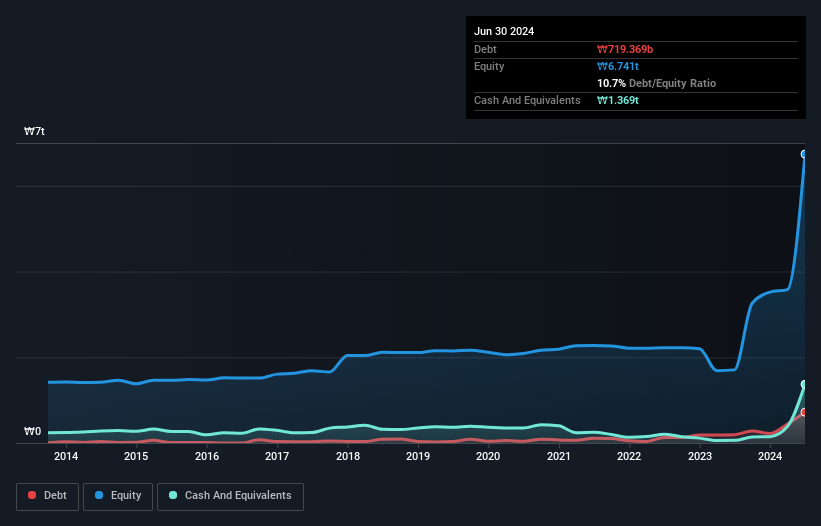

Hyundai G.F. Holdings (KOSE:A005440)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hyundai G.F. Holdings Co., Ltd. engages in rental and investment businesses with a market cap of ₩787.32 billion.

Operations: Hyundai G.F. Holdings generates revenue primarily from rental and investment activities. The company has a market cap of ₩787.32 billion.

Hyundai G.F. Holdings, a promising player in South Korea, has shown remarkable earnings growth of 242291% over the past year, far outpacing the Trade Distributors industry average of 21.7%. The company is trading at 42.8% below its estimated fair value and has more cash than total debt, indicating strong financial health. Additionally, Hyundai G.F.'s revenue is forecast to grow by 20.82% annually, underscoring its potential for future expansion and profitability.

- Click here to discover the nuances of Hyundai G.F. Holdings with our detailed analytical health report.

Assess Hyundai G.F. Holdings' past performance with our detailed historical performance reports.

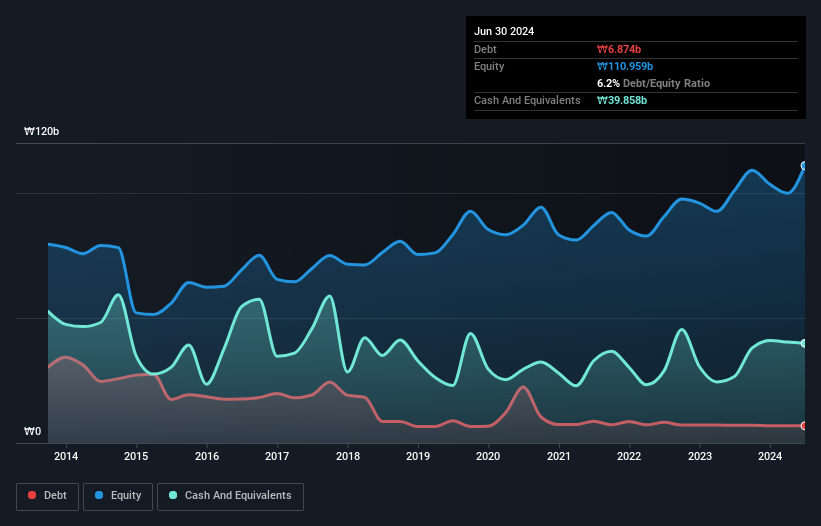

Korea Electric Power Industrial Development (KOSE:A130660)

Simply Wall St Value Rating: ★★★★★★

Overview: Korea Electric Power Industrial Development Co., Ltd. (KOSE:A130660) specializes in providing electric power generation services and has a market cap of ₩463.25 billion.

Operations: Korea Electric Power Industrial Development generates revenue primarily from its electric power generation services, amounting to ₩373.29 billion.

Korea Electric Power Industrial Development has demonstrated solid financial performance, with earnings growth of 26.8% over the past year, surpassing the Electric Utilities industry average of 4.6%. The company’s debt to equity ratio improved from 10.7% to 6.2% in five years, indicating better financial health. Recent reports show net income for Q2 at KRW 10.89 million, up from KRW 8.35 million a year ago, despite sales dropping to KRW 6.94 million from KRW 7.83 million last year.

Cuckoo Holdings (KOSE:A192400)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cuckoo Holdings Co., Ltd., along with its subsidiaries, manufactures and sells electric heaters and daily necessities in South Korea and internationally, with a market cap of ₩775.41 billion.

Operations: Cuckoo Holdings generates revenue primarily from its electric heating appliances segment, amounting to ₩797.73 billion.

Cuckoo Holdings, a small-cap player in South Korea, has shown consistent earnings growth of 8.8% annually over the past five years. The company repurchased shares in 2024, reflecting confidence in its valuation. Despite its debt to equity ratio increasing slightly from 0% to 0.04%, Cuckoo remains financially sound with more cash than total debt. However, recent earnings growth of 6.5% lagged behind the Consumer Durables industry’s robust performance at 26.5%.

- Dive into the specifics of Cuckoo Holdings here with our thorough health report.

Examine Cuckoo Holdings' past performance report to understand how it has performed in the past.

Seize The Opportunity

- Dive into all 188 of the KRX Undiscovered Gems With Strong Fundamentals we have identified here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hyundai G.F. Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A005440

Solid track record with excellent balance sheet and pays a dividend.