Advertisement

- South Korea

- /

- Consumer Durables

- /

- KOSDAQ:A025440

DHAUTOWARE Co., LTD's (KOSDAQ:025440) 27% Jump Shows Its Popularity With Investors

DHAUTOWARE Co., LTD (KOSDAQ:025440) shareholders are no doubt pleased to see that the share price has bounced 27% in the last month, although it is still struggling to make up recently lost ground. But the last month did very little to improve the 58% share price decline over the last year.

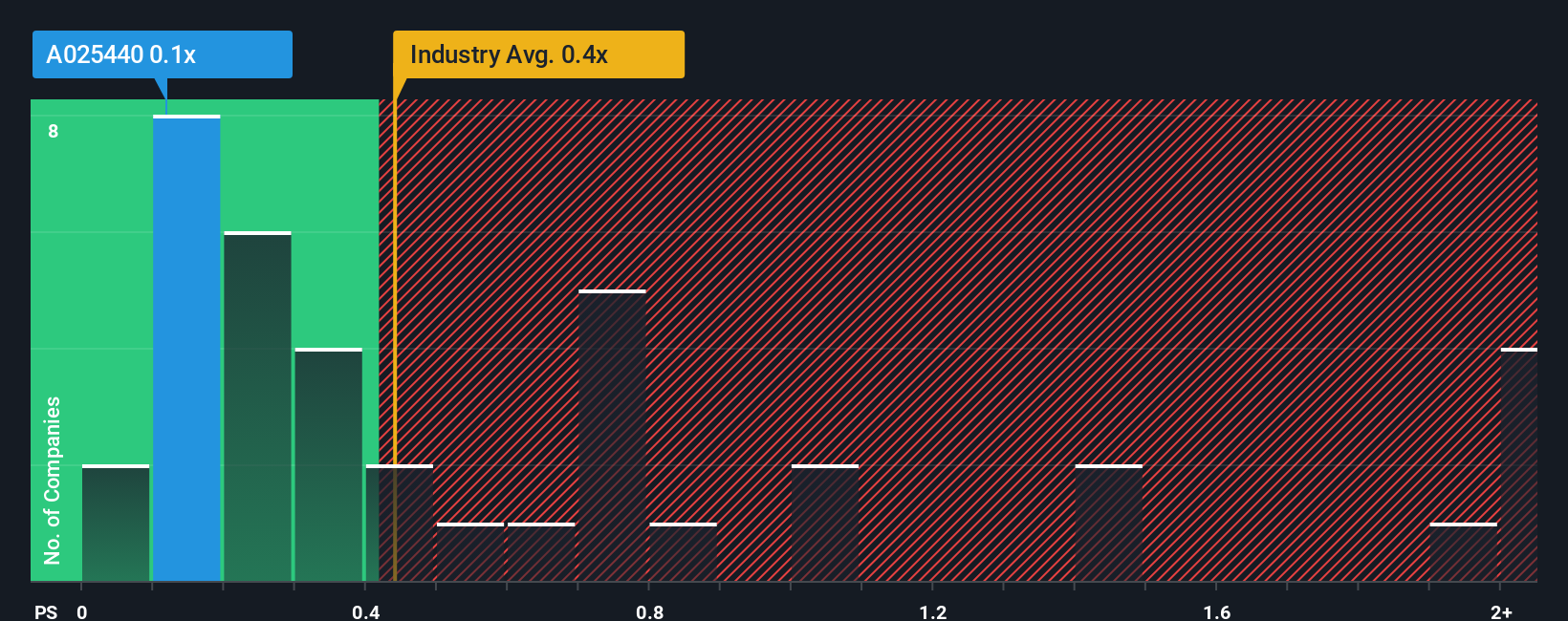

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about DHAUTOWARE's P/S ratio of 0.1x, since the median price-to-sales (or "P/S") ratio for the Consumer Durables industry in Korea is also close to 0.4x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for DHAUTOWARE

What Does DHAUTOWARE's Recent Performance Look Like?

As an illustration, revenue has deteriorated at DHAUTOWARE over the last year, which is not ideal at all. Perhaps investors believe the recent revenue performance is enough to keep in line with the industry, which is keeping the P/S from dropping off. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on DHAUTOWARE will help you shine a light on its historical performance.Do Revenue Forecasts Match The P/S Ratio?

The only time you'd be comfortable seeing a P/S like DHAUTOWARE's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a frustrating 5.4% decrease to the company's top line. Regardless, revenue has managed to lift by a handy 12% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

It's interesting to note that the rest of the industry is similarly expected to grow by 4.9% over the next year, which is fairly even with the company's recent medium-term annualised growth rates.

With this information, we can see why DHAUTOWARE is trading at a fairly similar P/S to the industry. It seems most investors are expecting to see average growth rates continue into the future and are only willing to pay a moderate amount for the stock.

What Does DHAUTOWARE's P/S Mean For Investors?

Its shares have lifted substantially and now DHAUTOWARE's P/S is back within range of the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we've seen, DHAUTOWARE's three-year revenue trends seem to be contributing to its P/S, given they look similar to current industry expectations. With previous revenue trends that keep up with the current industry outlook, it's hard to justify the company's P/S ratio deviating much from it's current point. Unless the recent medium-term conditions change, they will continue to support the share price at these levels.

It is also worth noting that we have found 3 warning signs for DHAUTOWARE (1 makes us a bit uncomfortable!) that you need to take into consideration.

If these risks are making you reconsider your opinion on DHAUTOWARE, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A025440

DHAUTOWARE

Develops and supplies in-vehicle infotainment products to motor companies worldwide.

Low risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor