- South Korea

- /

- Consumer Durables

- /

- KOSDAQ:A007680

Does Daewon (KOSDAQ:007680) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Daewon Co., Ltd. (KOSDAQ:007680) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Daewon

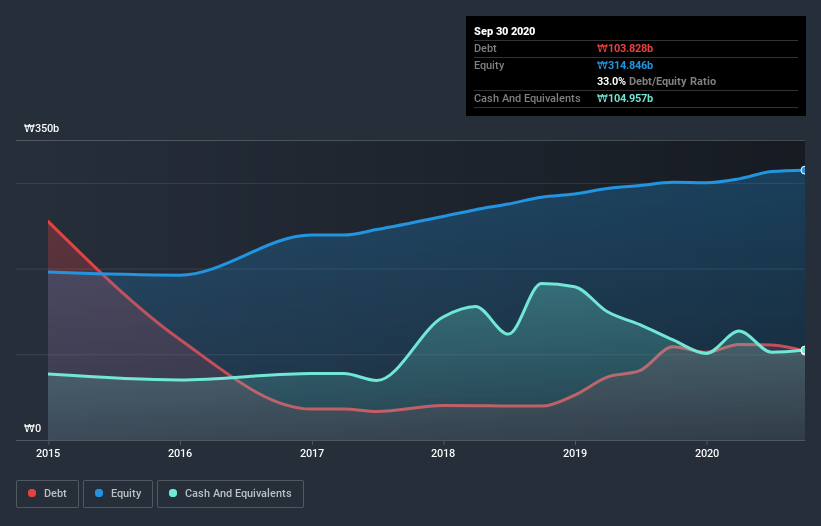

What Is Daewon's Net Debt?

As you can see below, Daewon had ₩103.8b of debt at September 2020, down from ₩108.7b a year prior. But on the other hand it also has ₩105.0b in cash, leading to a ₩1.13b net cash position.

How Healthy Is Daewon's Balance Sheet?

According to the last reported balance sheet, Daewon had liabilities of ₩135.4b due within 12 months, and liabilities of ₩88.8b due beyond 12 months. On the other hand, it had cash of ₩105.0b and ₩45.4b worth of receivables due within a year. So it has liabilities totalling ₩73.9b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of ₩117.9b, so it does suggest shareholders should keep an eye on Daewon's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. While it does have liabilities worth noting, Daewon also has more cash than debt, so we're pretty confident it can manage its debt safely.

In fact Daewon's saving grace is its low debt levels, because its EBIT has tanked 54% in the last twelve months. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Daewon's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Daewon may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Daewon burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing up

While Daewon does have more liabilities than liquid assets, it also has net cash of ₩1.13b. Despite the cash, we do find Daewon's EBIT growth rate concerning, so we're not particularly comfortable with the stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 5 warning signs we've spotted with Daewon .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Daewon, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A007680

Daewon

Engages in the manufactures, produces, and sells ready-mixed concrete and aggregate products in South Korea.

Mediocre balance sheet and slightly overvalued.