Stock Analysis

- South Korea

- /

- Machinery

- /

- KOSDAQ:A044490

Exploring Undiscovered Gems In South Korea July 2024

Reviewed by Simply Wall St

The South Korean stock market recently halted its upward momentum, with the KOSPI index experiencing a modest decline amid mixed performances across various sectors. This shift comes amidst broader global market consolidations, particularly impacting technology and semiconductor companies. In this context, identifying stocks that demonstrate strong fundamentals and potential for growth becomes crucial, especially in a market environment characterized by such fluctuations and sector-specific impacts.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CYMECHS | 10.99% | 11.45% | 3.52% | ★★★★★★ |

| Korea Cast Iron Pipe Ind | NA | 2.58% | 14.14% | ★★★★★★ |

| Korea Ratings | NA | 1.74% | 0.87% | ★★★★★★ |

| Korea Airport ServiceLtd | NA | 0.40% | 27.17% | ★★★★★★ |

| ASIA Holdings | 34.13% | 8.28% | 15.67% | ★★★★★★ |

| Oriental Precision & EngineeringLtd | 59.19% | 3.54% | 5.92% | ★★★★★★ |

| Kyungdong Invest | 8.15% | 3.08% | 15.07% | ★★★★★★ |

| Daewon Cable | 24.70% | 8.50% | 62.14% | ★★★★★☆ |

| THINKWARE | 36.41% | 19.78% | 21.78% | ★★★★★☆ |

| Ubiquoss Holdings | 2.69% | 9.93% | 14.22% | ★★★★★☆ |

Let's dive into some prime choices out of from the screener.

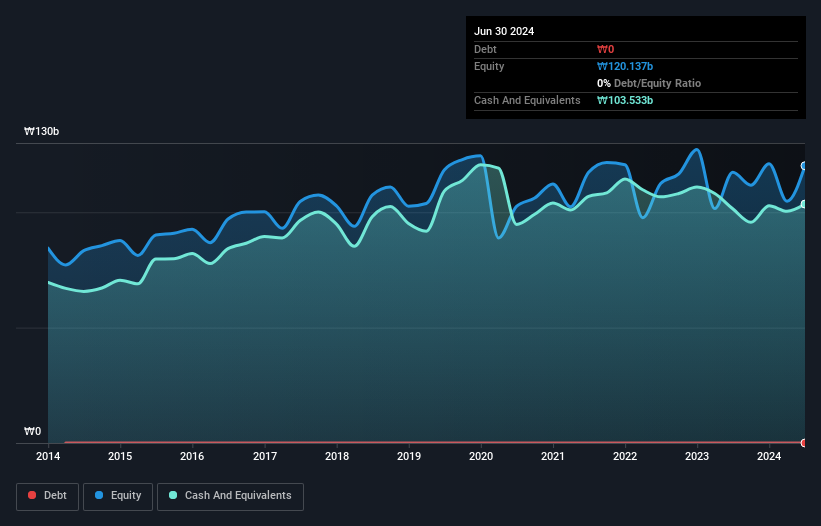

Korea Ratings (KOSDAQ:A034950)

Simply Wall St Value Rating: ★★★★★★

Overview: Korea Ratings Co., Ltd. operates primarily in South Korea, offering credit rating and business valuation services through its subsidiaries, with a market capitalization of approximately ₩384.08 billion.

Operations: The company generates significant revenue from its Korean Corporate Evaluation services, contributing ₩56.21 billion, alongside its Incredible segment which adds another ₩40.99 billion. It maintains a high gross profit margin consistently above 99%, reflecting minimal cost of goods sold relative to revenue.

Korea Ratings, a standout in the South Korean market, has demonstrated robust financial health with no debt and consistent profitability. Recently, its earnings growth of 25.1% significantly outpaced the industry's 0.8%, highlighting its competitive edge. The company's strong cash flow generation and high-quality earnings underscore its operational efficiency. With an upcoming Q1 2024 earnings report on May 24, investors are keenly watching this lesser-known yet promising entity for potential growth opportunities.

- Click here and access our complete health analysis report to understand the dynamics of Korea Ratings.

Explore historical data to track Korea Ratings' performance over time in our Past section.

Korea Ratings (KOSDAQ:A034950)

Simply Wall St Value Rating: ★★★★★★

Overview: Korea Ratings Co., Ltd. operates primarily in South Korea, offering credit rating and business valuation services through its subsidiaries, with a market capitalization of approximately ₩384.08 billion.

Operations: The company generates significant revenue from its Korean Corporate Evaluation services, contributing ₩56.21 billion, alongside its Incredible segment which adds another ₩40.99 billion. It maintains a high gross profit margin consistently above 99%, reflecting minimal cost of goods sold relative to revenue.

Korea Ratings, a standout in the South Korean market, has demonstrated robust financial health with no debt and consistent profitability. Recently, its earnings growth of 25.1% significantly outpaced the industry's 0.8%, highlighting its competitive edge. The company's strong cash flow generation and high-quality earnings underscore its operational efficiency. With an upcoming Q1 2024 earnings report on May 24, investors are keenly watching this lesser-known yet promising entity for potential growth opportunities.

- Click here and access our complete health analysis report to understand the dynamics of Korea Ratings.

Explore historical data to track Korea Ratings' performance over time in our Past section.

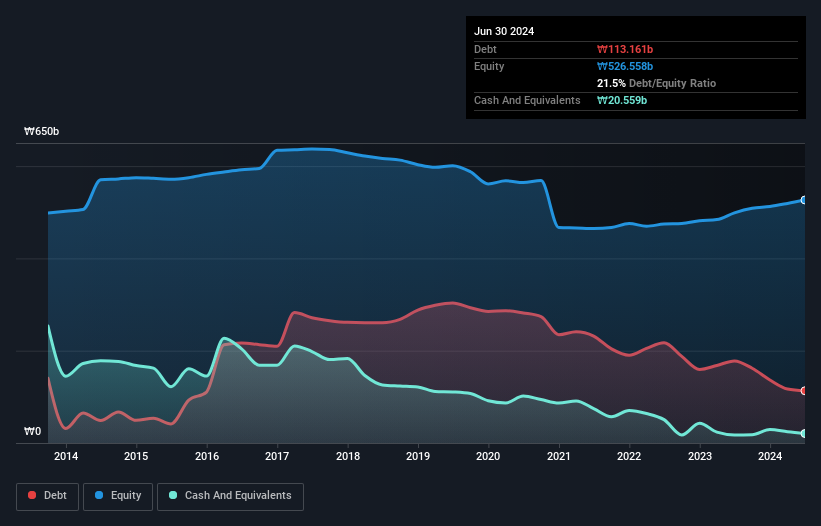

TaewoongLtd (KOSDAQ:A044490)

Simply Wall St Value Rating: ★★★★★★

Overview: Taewoong Co., Ltd is engaged in the manufacturing and international sale of open-die forgings and ring rolled products, with a market capitalization of approximately ₩349.13 billion.

Operations: The company generates its revenue primarily through the sale of goods, which accounted for ₩443.76 billion in the most recent fiscal quarter. It achieved a gross profit margin of 15.30% during this period, reflecting the cost efficiency relative to its sales revenue.

Taewoong Ltd, a lesser-known entity within the machinery sector, has demonstrated remarkable financial performance with earnings growth of 317% last year, surpassing its industry’s decline of 2%. The company's debt to equity ratio improved significantly from 50% to 23% over five years, indicating robust financial health. Trading at a substantial discount—67% below estimated fair value—it presents an intriguing opportunity. Additionally, Taewoong's interest payments are well-covered by EBIT, six times over, ensuring stability in fulfilling debt obligations.

- Navigate through the intricacies of TaewoongLtd with our comprehensive health report here.

Understand TaewoongLtd's track record by examining our Past report.

TaewoongLtd (KOSDAQ:A044490)

Simply Wall St Value Rating: ★★★★★★

Overview: Taewoong Co., Ltd is engaged in the manufacturing and international sale of open-die forgings and ring rolled products, with a market capitalization of approximately ₩349.13 billion.

Operations: The company generates its revenue primarily through the sale of goods, which accounted for ₩443.76 billion in the most recent fiscal quarter. It achieved a gross profit margin of 15.30% during this period, reflecting the cost efficiency relative to its sales revenue.

Taewoong Ltd, a lesser-known entity within the machinery sector, has demonstrated remarkable financial performance with earnings growth of 317% last year, surpassing its industry’s decline of 2%. The company's debt to equity ratio improved significantly from 50% to 23% over five years, indicating robust financial health. Trading at a substantial discount—67% below estimated fair value—it presents an intriguing opportunity. Additionally, Taewoong's interest payments are well-covered by EBIT, six times over, ensuring stability in fulfilling debt obligations.

- Navigate through the intricacies of TaewoongLtd with our comprehensive health report here.

Understand TaewoongLtd's track record by examining our Past report.

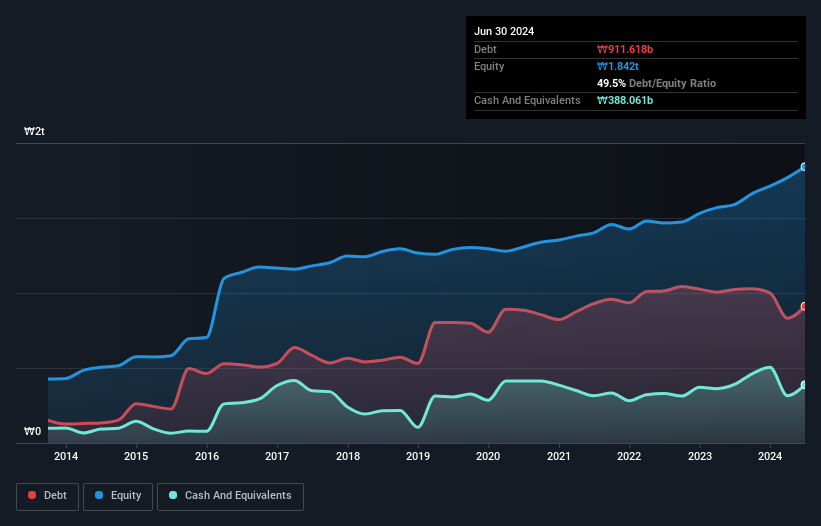

Samyang (KOSE:A145990)

Simply Wall St Value Rating: ★★★★★★

Overview: Samyang Corporation operates in the chemicals and food sectors across Korea, China, Japan, other parts of Asia, Europe, and internationally with a market capitalization of approximately ₩494.51 billion.

Operations: The company operates primarily in the food and chemicals sectors, generating significant revenue streams from these segments. It recorded a gross profit margin of 18.10% in the latest quarter, reflecting its ability to manage production costs effectively relative to sales.

Samyang, a lesser-known yet promising player in South Korea's market, showcases a P/E ratio significantly below the national average at 4.4 compared to 12.6. With a substantial earnings growth of 77.4% over the past year—outpacing its industry's 47.4%—the company demonstrates robust financial health and potential for value discovery. Additionally, its debt-to-equity ratio improved impressively from 63.8% to 47%, reflecting prudent financial management and enhancing its investment appeal in the competitive food sector.

- Unlock comprehensive insights into our analysis of Samyang stock in this health report.

Evaluate Samyang's historical performance by accessing our past performance report.

Samyang (KOSE:A145990)

Simply Wall St Value Rating: ★★★★★★

Overview: Samyang Corporation operates in the chemicals and food sectors across Korea, China, Japan, other parts of Asia, Europe, and internationally with a market capitalization of approximately ₩494.51 billion.

Operations: The company operates primarily in the food and chemicals sectors, generating significant revenue streams from these segments. It recorded a gross profit margin of 18.10% in the latest quarter, reflecting its ability to manage production costs effectively relative to sales.

Samyang, a lesser-known yet promising player in South Korea's market, showcases a P/E ratio significantly below the national average at 4.4 compared to 12.6. With a substantial earnings growth of 77.4% over the past year—outpacing its industry's 47.4%—the company demonstrates robust financial health and potential for value discovery. Additionally, its debt-to-equity ratio improved impressively from 63.8% to 47%, reflecting prudent financial management and enhancing its investment appeal in the competitive food sector.

- Unlock comprehensive insights into our analysis of Samyang stock in this health report.

Evaluate Samyang's historical performance by accessing our past performance report.

Seize The Opportunity

- Investigate our full lineup of 212 KRX Undiscovered Gems With Strong Fundamentals right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether TaewoongLtd is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A044490

TaewoongLtd

Manufactures and sells open-die forgings and ring rolled products in South Korea and internationally.

Flawless balance sheet and undervalued.