Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:5214

Nippon Electric Glass (TSE:5214) Is Increasing Its Dividend To ¥70.00

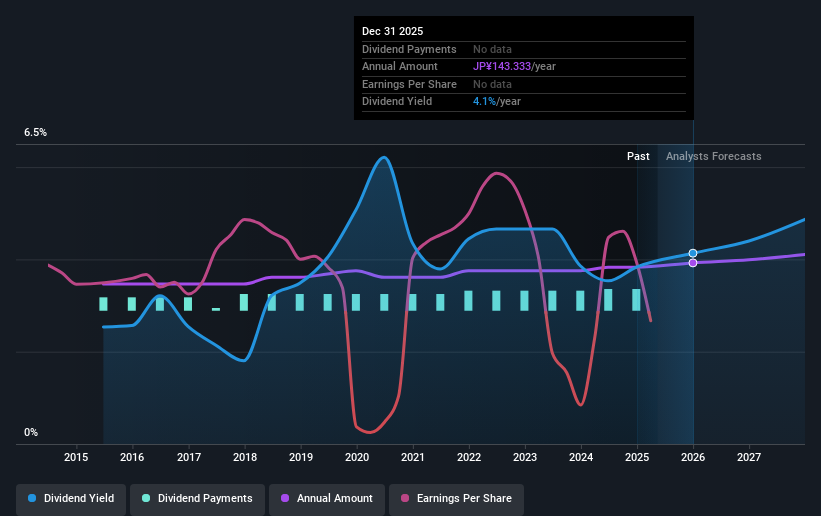

The board of Nippon Electric Glass Co., Ltd. (TSE:5214) has announced that it will be paying its dividend of ¥70.00 on the 1st of September, an increased payment from last year's comparable dividend. This will take the annual payment to 4.2% of the stock price, which is above what most companies in the industry pay.

Our free stock report includes 1 warning sign investors should be aware of before investing in Nippon Electric Glass. Read for free now.Nippon Electric Glass' Distributions May Be Difficult To Sustain

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Nippon Electric Glass is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. This gives us some comfort about the level of the dividend payments.

Over the next year, EPS is forecast to rise by 36.5%. While it is good to see income moving in the right direction, it still looks like the company won't achieve profitability. The positive free cash flows give us some comfort, however, that the dividend could continue to be sustained.

Check out our latest analysis for Nippon Electric Glass

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2015, the annual payment back then was ¥80.00, compared to the most recent full-year payment of ¥145.00. This means that it has been growing its distributions at 6.1% per annum over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

The Dividend Has Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. We are encouraged to see that Nippon Electric Glass has grown earnings per share at 9.2% per year over the past five years. Unprofitable companies aren't normally our pick for a dividend stock, but we like the growth that we have been seeing. All is not lost, but the future of the dividend definitely rests upon the company's ability to become profitable soon.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Nippon Electric Glass' payments are rock solid. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 1 warning sign for Nippon Electric Glass that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Nippon Electric Glass might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5214

Nippon Electric Glass

Manufactures and sells specialty glass products and glass manufacturing machinery in Japan and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor