Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:6871

Micronics Japan (TSE:6871): Assessing Valuation Following New 2025 Earnings Guidance

Simply Wall St

Reviewed by Simply Wall St

Micronics Japan (TSE:6871) announced fresh earnings guidance for the year ending December 2025, forecasting JPY 68,900 million in net sales and JPY 13,800 million in operating profit. This update often shapes investor expectations regarding upcoming performance.

See our latest analysis for Micronics Japan.

Micronics Japan’s updated earnings outlook comes after a big run in its share price, with a 1-month share price return of 21.4% and an impressive 113.1% year-to-date. Over the past year, total shareholder return topped 116%, which suggests rising momentum as investors respond to both recent results and forward-looking guidance.

If you’re watching for what’s next in the market, now’s an ideal time to broaden your radar and discover fast growing stocks with high insider ownership

But with shares currently trading well above analyst price targets and recent surges already factored in, the lingering question for investors is whether Micronics Japan still offers upside or if markets have already priced in future gains.

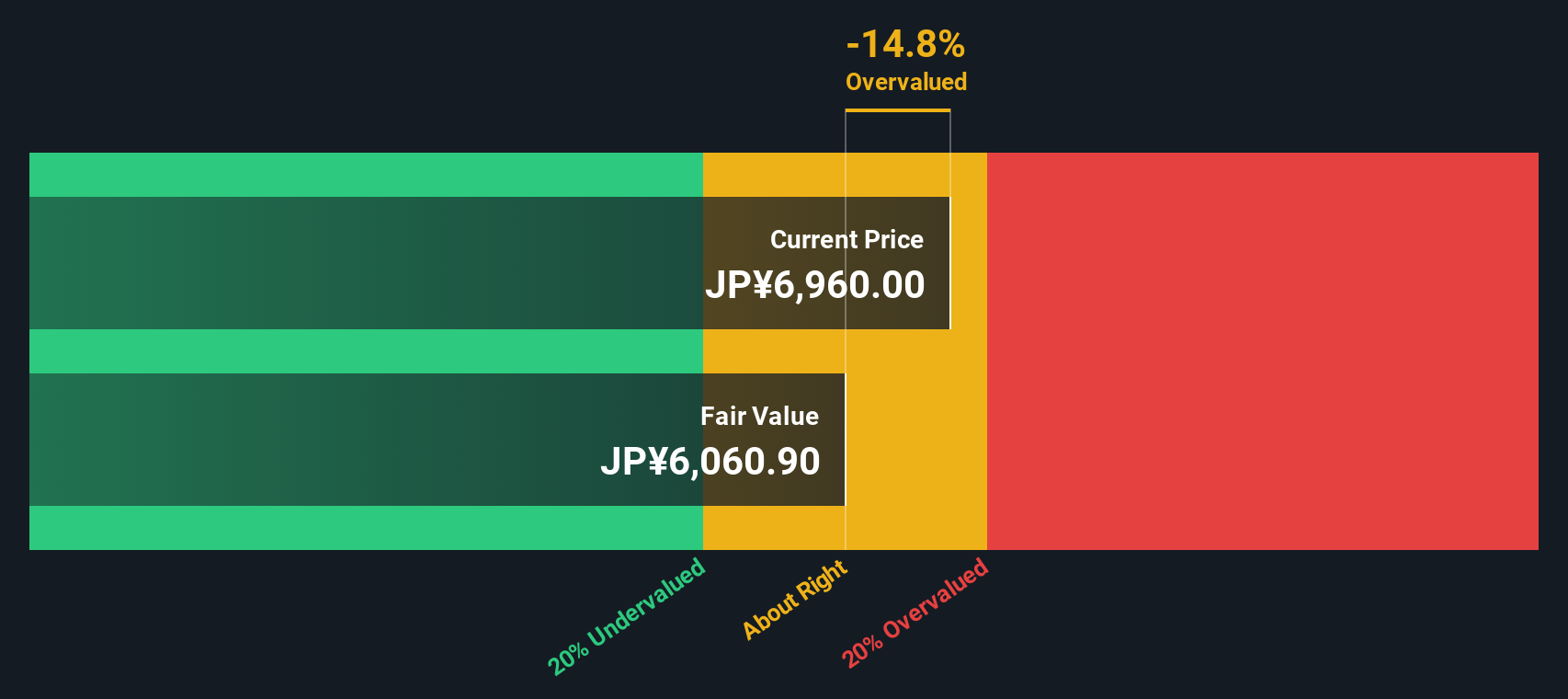

Price-to-Earnings of 32.5x: Is it justified?

Micronics Japan trades at a price-to-earnings (P/E) ratio of 32.5x, putting its valuation well above both peers and sector averages based on its last close price.

The price-to-earnings ratio reflects how much investors are willing to pay today for a company’s current and projected future earnings. For semiconductor companies, a high P/E may indicate optimism around growth prospects, but it can also raise the bar for performance.

With Micronics Japan’s 32.5x P/E, the stock is valued substantially higher than the Japanese semiconductor industry average of 20.2x and the peer average of 22.7x. This signals that investors are paying a premium, likely in anticipation of continued strong profit gains. However, this premium may be difficult to justify if the company’s growth pace moderates. The market currently prices Micronics Japan not only above the present industry but also beyond what regression analysis suggests is a "fair" earnings multiple (30.1x), which highlights how stretched expectations have become.

Explore the SWS fair ratio for Micronics Japan

Result: Price-to-Earnings of 32.5x (OVERVALUED)

However, slowing revenue growth at 13% annually and the stock trading 23% above analyst price targets could quickly challenge the current bullish outlook.

Find out about the key risks to this Micronics Japan narrative.

Another View: Discounted Cash Flow Says Overvalued Too

Taking a different angle, the SWS DCF model estimates Micronics Japan's fair value at ¥6,053, which is noticeably below its recent price of ¥8,290. This approach suggests the shares could be 37% above fair value. Can longer-term profit growth bridge that valuation gap, or is risk beginning to outweigh reward?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Micronics Japan for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 863 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Micronics Japan Narrative

If you have a different perspective or want to dig deeper into the numbers, it's easy to build your own take on Micronics Japan in just a few minutes, so why not Do it your way

A great starting point for your Micronics Japan research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never stop at just one opportunity. Widen your search and uncover compelling stocks in high-potential sectors with these handpicked tools from Simply Wall Street:

- Target fresh growth by examining these 863 undervalued stocks based on cash flows, where you’ll spot companies trading below their true worth based on solid financials.

- Unlock passive income streams as you check out these 16 dividend stocks with yields > 3% to find stocks with yields above 3% and robust track records.

- Ride the innovation wave by seizing early opportunities in digital disruption. Browse these 82 cryptocurrency and blockchain stocks at the frontier of blockchain and cryptocurrency trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6871

Micronics Japan

Develops, manufactures, and sells body measuring equipment, semiconductor, and liquid crystal display inspection equipment worldwide.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor