Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Encho Co.,Ltd. (TYO:8208) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for EnchoLtd

What Is EnchoLtd's Debt?

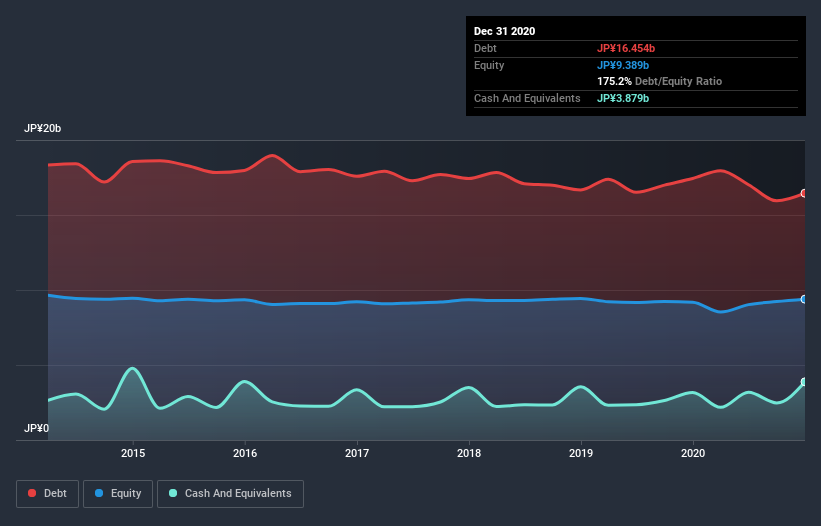

The image below, which you can click on for greater detail, shows that EnchoLtd had debt of JP¥15.9b at the end of December 2020, a reduction from JP¥17.4b over a year. However, it also had JP¥3.88b in cash, and so its net debt is JP¥12.0b.

A Look At EnchoLtd's Liabilities

According to the last reported balance sheet, EnchoLtd had liabilities of JP¥18.3b due within 12 months, and liabilities of JP¥10.2b due beyond 12 months. Offsetting this, it had JP¥3.88b in cash and JP¥1.10b in receivables that were due within 12 months. So it has liabilities totalling JP¥23.5b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the JP¥8.06b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, EnchoLtd would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

As it happens EnchoLtd has a fairly concerning net debt to EBITDA ratio of 7.1 but very strong interest coverage of 11.5. This means that unless the company has access to very cheap debt, that interest expense will likely grow in the future. Notably, EnchoLtd's EBIT launched higher than Elon Musk, gaining a whopping 216% on last year. There's no doubt that we learn most about debt from the balance sheet. But it is EnchoLtd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, EnchoLtd generated free cash flow amounting to a very robust 92% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

We feel some trepidation about EnchoLtd's difficulty level of total liabilities, but we've got positives to focus on, too. To wit both its conversion of EBIT to free cash flow and EBIT growth rate were encouraging signs. We think that EnchoLtd's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Be aware that EnchoLtd is showing 4 warning signs in our investment analysis , and 2 of those are concerning...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade EnchoLtd, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if EnchoLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:8208

EnchoLtd

Operates stores in Japan. The company’s stores offer lumber, construction materials, gardening supplies, paints, glues and adhesives, power tools, carpenter's tools, metal materials for construction, interior materials, electrical equipment, lamps, automobile parts, miscellaneous goods, stationery, bicycles, and leisure goods.

Good value slight.