As Japan's stock markets recently experienced volatility due to political shifts and a slightly hawkish tone from new leadership, investors are keenly observing the broader economic landscape and its impact on small-cap stocks. Despite these fluctuations, opportunities remain for discerning investors who can identify companies with strong fundamentals and potential for growth within this dynamic environment. In this context, Kotobuki Spirits stands out as one of three promising yet under-the-radar stocks in Japan that could capture investor interest.

Top 10 Undiscovered Gems With Strong Fundamentals In Japan

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Togami Electric Mfg | 1.39% | 3.97% | 10.23% | ★★★★★★ |

| Central Forest Group | NA | 7.05% | 14.29% | ★★★★★★ |

| AOKI Holdings | 28.27% | 0.91% | 37.15% | ★★★★★★ |

| Nitto Fuji Flour MillingLtd | 0.80% | 6.26% | 4.41% | ★★★★★★ |

| Otec | 9.81% | 2.32% | -1.39% | ★★★★★★ |

| Techno Smart | NA | 6.07% | -0.57% | ★★★★★★ |

| Soliton Systems K.K | 0.58% | 5.04% | 16.76% | ★★★★★★ |

| Yashima Denki | 2.93% | -2.38% | 13.99% | ★★★★★★ |

| HeadwatersLtd | NA | 19.26% | 23.89% | ★★★★★★ |

| Yukiguni Maitake | 170.63% | -6.51% | -39.66% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

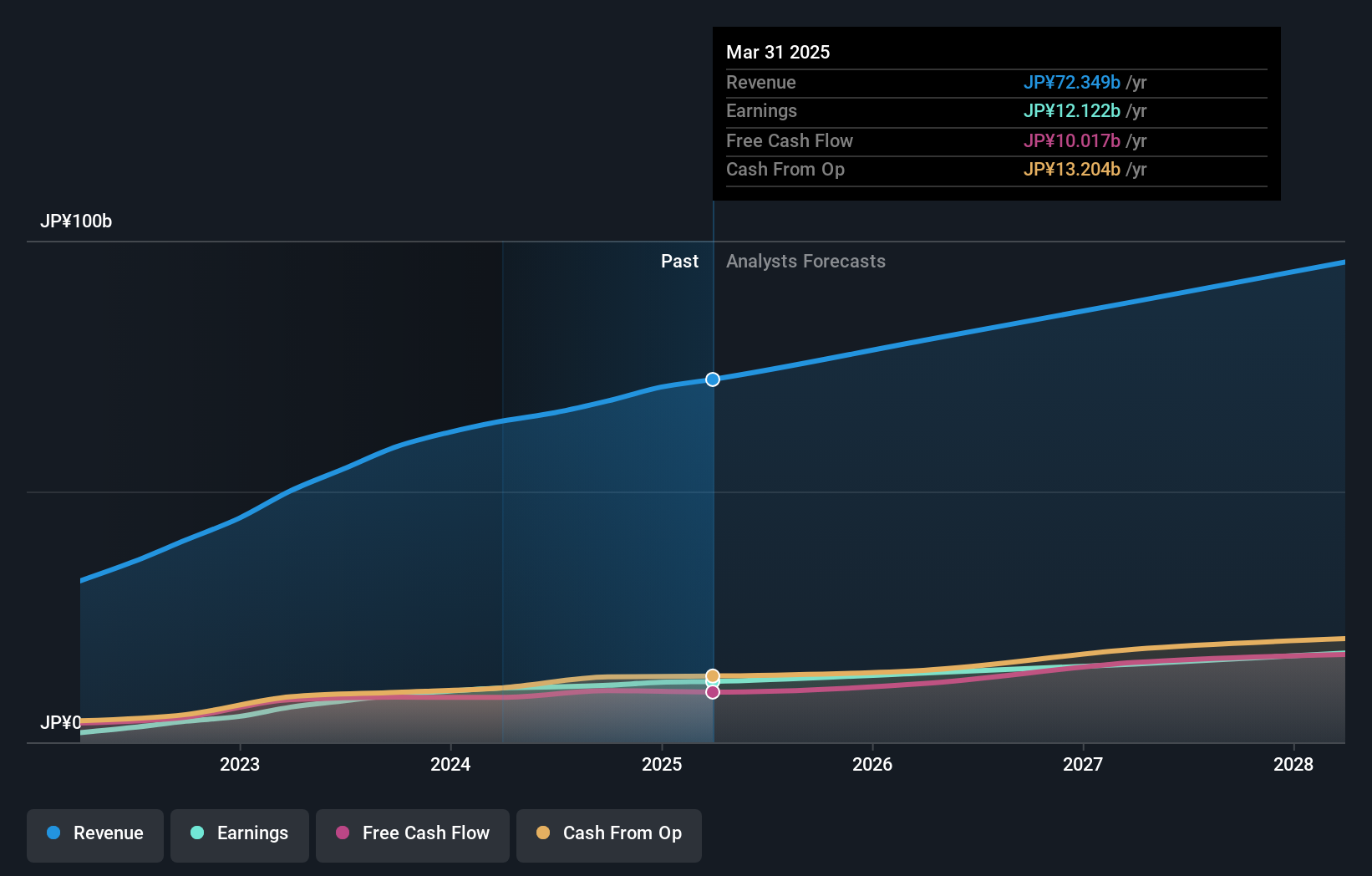

Kotobuki Spirits (TSE:2222)

Simply Wall St Value Rating: ★★★★★★

Overview: Kotobuki Spirits Co., Ltd. is a Japanese company that specializes in the production and sale of sweets, with a market capitalization of ¥285.61 billion.

Operations: Kotobuki Spirits generates revenue primarily from its segments Shukrei and Casey Shii, contributing ¥27.03 billion and ¥18.88 billion, respectively. The net profit margin shows a notable trend at 8.5%, highlighting the company's efficiency in converting sales into actual profit after expenses.

Kotobuki Spirits, a niche player in Japan's confectionery market, has shown impressive growth with earnings surging 33.7% over the past year, outpacing the food industry’s 27.5%. Trading at 46.6% below estimated fair value suggests potential undervaluation. The company's debt-to-equity ratio improved from 2.1 to 0.9 over five years, indicating better financial health and more cash than total debt supports stability in operations and future expansions within its sector.

- Click here to discover the nuances of Kotobuki Spirits with our detailed analytical health report.

Gain insights into Kotobuki Spirits' past trends and performance with our Past report.

SAN-ALTD (TSE:2659)

Simply Wall St Value Rating: ★★★★★★

Overview: SAN-A CO., LTD. operates a chain of supermarkets in Okinawa with a market cap of ¥179.10 billion.

Operations: The company generates revenue primarily through its supermarket operations in Okinawa. It has a market capitalization of ¥179.10 billion, reflecting its significant presence in the region's retail sector.

SAN-ALTD, a promising player in Japan's market, is trading at 41% below its fair value estimate. Over the past five years, earnings have grown at an annual rate of 8.7%, showcasing high-quality past earnings. Despite not outpacing the Consumer Retailing industry last year with a 17.6% growth rate compared to the industry's 22.2%, it remains debt-free and exhibits positive free cash flow. With no debt concerns and a profitable stance, SAN-ALTD seems positioned for steady growth ahead.

- Navigate through the intricacies of SAN-ALTD with our comprehensive health report here.

Examine SAN-ALTD's past performance report to understand how it has performed in the past.

PAL GROUP Holdings (TSE:2726)

Simply Wall St Value Rating: ★★★★★★

Overview: PAL GROUP Holdings CO., LTD. operates in Japan, focusing on the planning, manufacturing, wholesale, and retail of men's and women's clothing and accessories, with a market cap of ¥221.83 billion.

Operations: PAL GROUP Holdings generates revenue primarily from its clothing business, which contributed ¥121.28 billion, and its miscellaneous goods/accessories segment, adding ¥75.51 billion.

PAL GROUP Holdings is showing promising signs with its earnings growth of 18.8% in the past year, outpacing the Specialty Retail industry average of 5.3%. The company seems to be trading at a favorable valuation, approximately 43.5% below estimated fair value, which could suggest potential upside. With an impressive debt-to-equity ratio reduction from 41.2% to 18.9% over five years and interest coverage by EBIT at a robust 215 times, financial stability appears strong for this small-cap player in Japan's retail sector.

- Take a closer look at PAL GROUP Holdings' potential here in our health report.

Understand PAL GROUP Holdings' track record by examining our Past report.

Key Takeaways

- Click through to start exploring the rest of the 727 Japanese Undiscovered Gems With Strong Fundamentals now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kotobuki Spirits might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2222

Flawless balance sheet with solid track record.