Exploring TOCALOLtd And 2 Other Hidden Gems With Promising Potential

Reviewed by Simply Wall St

In the wake of a significant rally in U.S. stocks driven by election outcomes and economic policy expectations, small-cap indices like the Russell 2000 have shown notable gains, reflecting investor optimism about potential growth opportunities. Amidst this dynamic market environment, identifying promising small-cap stocks requires a keen focus on companies with strong fundamentals and innovative strategies that can capitalize on evolving economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Parker Drilling | 46.25% | -0.33% | 53.04% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Industrias del Cobre Sociedad Anónima | NA | 19.63% | 22.92% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| National General Insurance (P.J.S.C.) | NA | 9.68% | 28.34% | ★★★★★☆ |

| Arab Banking Corporation (B.S.C.) | 190.18% | 16.52% | 21.58% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

TOCALOLtd (TSE:3433)

Simply Wall St Value Rating: ★★★★★★

Overview: TOCALO Co., Ltd. specializes in developing surface modifying technologies and operates both in Japan and internationally, with a market cap of ¥114.66 billion.

Operations: The primary revenue stream for TOCALO Ltd. comes from its Thermal Spraying segment, generating ¥37.34 billion, followed by contributions from its Foreign Subsidiary at ¥7.79 billion and Domestic Subsidiary at ¥2.96 billion.

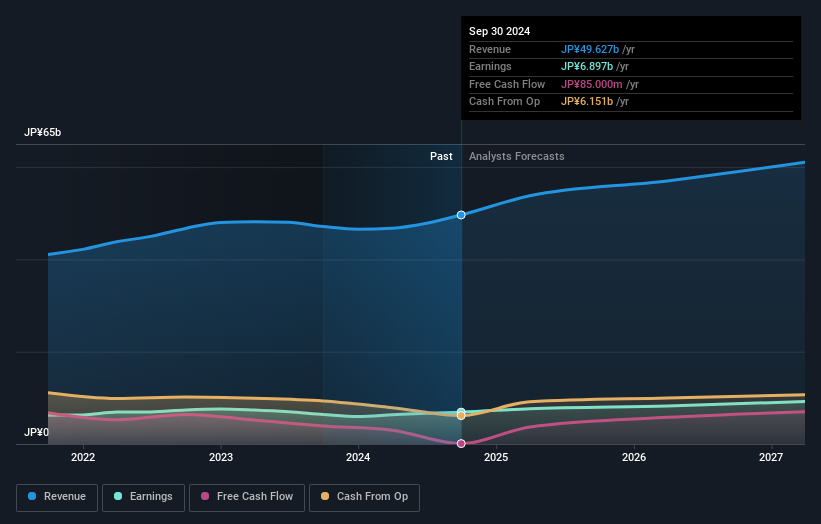

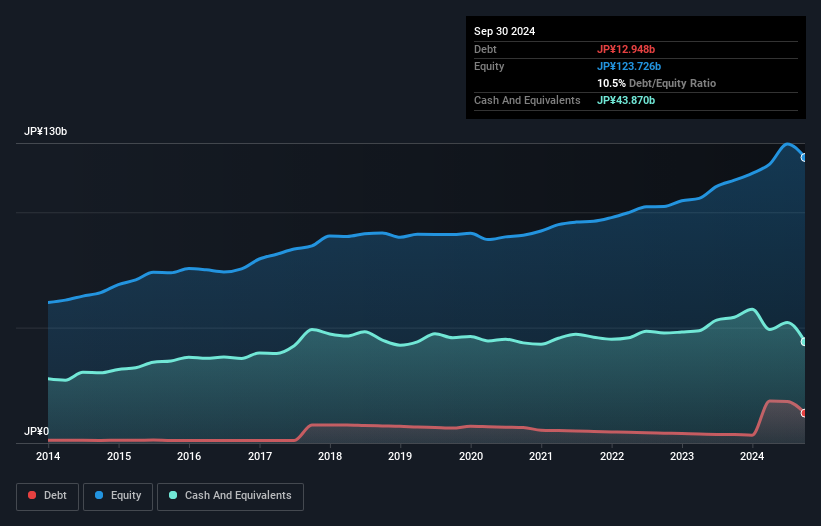

TOCALO Ltd., a smaller player in its industry, is trading at 57% below its estimated fair value, suggesting potential upside. The company boasts high-quality earnings and has reduced its debt-to-equity ratio from 14.4% to 7.3% over the past five years, indicating a stronger financial position. Recently, TOCALO raised its full-year guidance with expected net sales of ¥53 billion and operating profit of ¥11.5 billion, reflecting an optimistic outlook. Additionally, the dividend per share for the fiscal year ending March 2025 is projected at ¥63, up from previous forecasts, signaling confidence in future earnings growth.

- Navigate through the intricacies of TOCALOLtd with our comprehensive health report here.

Assess TOCALOLtd's past performance with our detailed historical performance reports.

KITZ (TSE:6498)

Simply Wall St Value Rating: ★★★★★★

Overview: KITZ Corporation specializes in the manufacturing and sale of valves and flow control devices both domestically and internationally, with a market cap of ¥99.84 billion.

Operations: KITZ Corporation generates revenue primarily from the manufacturing and sale of valves and flow control devices. The company's financial performance includes a notable net profit margin, reflecting its efficiency in managing costs relative to its revenue.

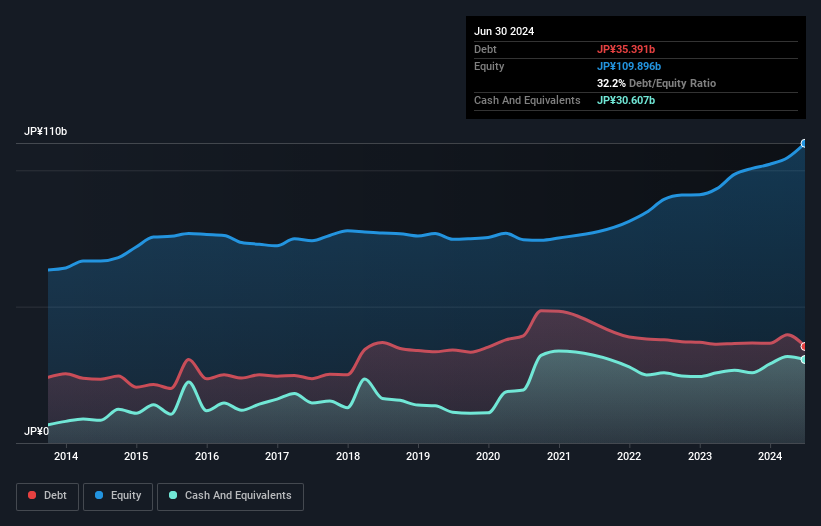

KITZ, a smaller player in the machinery sector, has shown promising financial health with a debt to equity ratio dropping from 44.4% to 35% over five years. The company boasts high-quality earnings and trades at 51% below its estimated fair value, suggesting potential undervaluation. Over the past year, KITZ's earnings growth of 4.6% outpaced the industry's 1.5%, highlighting its competitive edge. Recently, it repurchased nearly one million shares for ¥1 billion to enhance capital efficiency and address market dynamics. Earnings are forecasted to grow annually by about 5.52%, indicating steady future prospects in a dynamic environment.

Mitsubishi Pencil (TSE:7976)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mitsubishi Pencil Co., Ltd. is a Japanese company that manufactures and supplies writing instruments, with a market capitalization of ¥148.32 billion.

Operations: The company generates revenue primarily from the sale of writing instruments. It has a market capitalization of ¥148.32 billion.

Mitsubishi Pencil, a notable player in writing instruments, has seen earnings grow by 44% over the past year, outpacing the industry average of 5%. Trading at 61% below estimated fair value suggests potential for investors. The company recently revised its dividend to ¥22 per share and announced a special dividend of ¥1. However, operating profit guidance was lowered to ¥11.5 billion due to costs from acquiring Lamy as a subsidiary. A joint venture with Linc Limited aims to leverage Mitsubishi's technology for high-quality products in India, enhancing market reach and corporate value moving forward.

- Click here and access our complete health analysis report to understand the dynamics of Mitsubishi Pencil.

Gain insights into Mitsubishi Pencil's past trends and performance with our Past report.

Summing It All Up

- Delve into our full catalog of 4664 Undiscovered Gems With Strong Fundamentals here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TOCALOLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3433

TOCALOLtd

Develops surface modifying technologies in Japan and internationally.

Flawless balance sheet with proven track record and pays a dividend.