Advertisement

- Japan

- /

- Industrials

- /

- TSE:9045

Keihan Holdings (TSE:9045): Assessing Valuation After Upbeat Results, Upgraded Forecasts, and a Higher Dividend

Simply Wall St

Reviewed by Simply Wall St

Keihan Holdings (TSE:9045) announced interim results that surpassed expectations, thanks in part to brisk real estate sales and Expo 2025 demand. Alongside the earnings, management raised annual forecasts and upgraded the dividend outlook.

See our latest analysis for Keihan Holdings.

Keihan Holdings’ upbeat earnings and new dividend outlook have helped revive momentum, even after a muted few months. The stock's share price is still down year-to-date, but patient shareholders have enjoyed an 8.6% total return over the past year. This signals that underlying prospects and sentiment are stabilizing after a turbulent stretch.

If you’re curious about where else optimism might be building, now’s a great opportunity to broaden your search and discover fast growing stocks with high insider ownership

With forecasts and dividends on the rise, investors are now asking whether Keihan Holdings is actually undervalued, or if the company’s future growth is already fully reflected in its current share price.

Price-to-Earnings of 11.2x: Is it justified?

Keihan Holdings is trading on a price-to-earnings ratio of 11.2x, which signals better value compared to both peers and the broader industrials sector. At a last close of ¥3,170, this multiple indicates the company may be attractively priced for investors looking at earnings relative to share price.

The price-to-earnings ratio reflects how much investors are willing to pay for each ¥1 of earnings. It is a widely used benchmark for comparing valuations, especially within mature sectors such as transportation and industrials, where earnings quality and growth prospects are scrutinized closely.

At 11.2x, Keihan Holdings’ multiple is not only below the Japanese market average of 14.3x, but also well under the Asian Industrials industry average of 12.9x and the peer group average of 15.2x. Regression analysis points to a fair price-to-earnings ratio of 13.1x for the company, which suggests there could be room for market sentiment to turn more positive and for the share price to move higher over time.

Explore the SWS fair ratio for Keihan Holdings

Result: Price-to-Earnings of 11.2x (UNDERVALUED)

However, muted revenue and profit growth, along with lingering share price weakness, could present challenges for Keihan Holdings’ valuation story in the months ahead.

Find out about the key risks to this Keihan Holdings narrative.

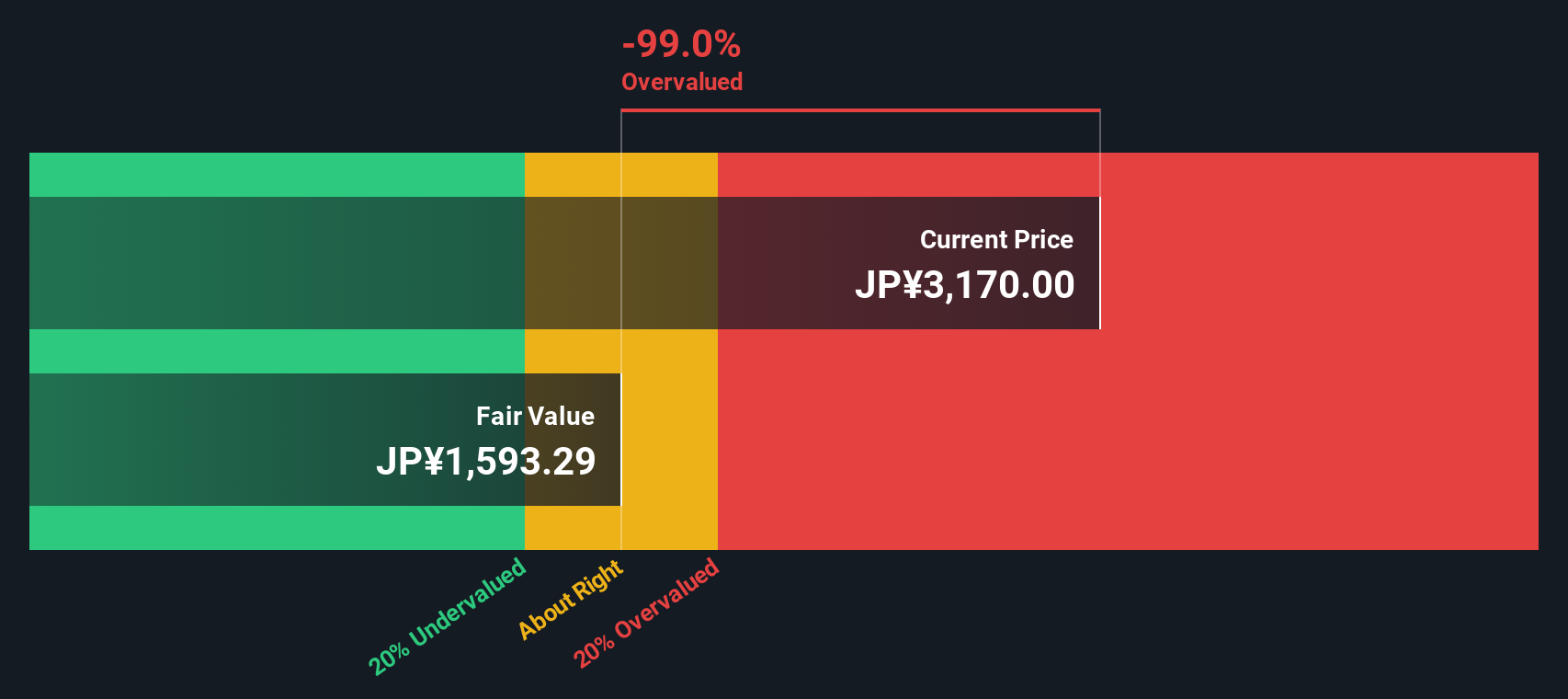

Another View: DCF Model Shows a Different Picture

While the price-to-earnings approach suggests Keihan Holdings is attractively valued, our SWS DCF model offers a challenge. It estimates fair value at ¥1,593, which is well below the current share price of ¥3,170. This indicates investors may be paying a premium today and raises doubts about upside potential.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Keihan Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Keihan Holdings Narrative

If you see things differently or would rather dive into the data firsthand, you can craft your own narrative in just a few minutes. Do it your way

A great starting point for your Keihan Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investing means staying ahead. Give yourself an edge and check the market for game-changing opportunities that might otherwise slip by.

- Unlock high-growth potential by scanning the market for these 3589 penny stocks with strong financials with strong financials and surprising momentum.

- Capture steady income by hunting for these 16 dividend stocks with yields > 3% that consistently deliver yields above 3 percent.

- Seize tomorrow’s breakthroughs with a curated list of these 32 healthcare AI stocks that are leading the charge in medical technology innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Keihan Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9045

Keihan Holdings

Engages in the transportation and various other businesses in Japan.

Proven track record and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor