Glory (TSE:6457) shares have edged up slightly in the past day, continuing a year marked by steady gains. Investors watching the capital goods sector may find Glory’s trajectory worth a closer look, especially considering its recent momentum.

This year’s strong run, with a 43.4% year-to-date share price return and a one-year total shareholder return of 48.7%, shows that momentum for Glory is still building. Short-term movements may ebb and flow, but that long-term performance places the stock among the sector’s stronger stories.

But the real question remains: is Glory’s robust performance an early signal of further upside, or has the market already factored in all of its future growth potential, leaving little room for a bargain?

Advertisement

Price-to-Earnings of 19.3x: Is it justified?

Glory is currently trading at a price-to-earnings (P/E) ratio of 19.3x, noticeably above both its industry peers and the level suggested by regression analysis. With the last close at ¥3,674, the stock appears expensive when measured against these benchmarks.

The P/E ratio measures how much investors are willing to pay today for a dollar of future earnings. In capital goods, a higher multiple often signals expectations of strong profit growth or superior business quality relative to competitors.

In Glory’s case, the 19.3x P/E is significantly higher than the JP Machinery industry average of 13.4x, and also exceeds the estimated fair P/E ratio of 18.2x. This suggests the market is pricing in premium expectations for Glory’s future earnings compared to its broader sector. Whether the company can deliver the growth implied by this premium is an open question, and the market could shift toward the fair ratio if expectations are not met.

Another View: Discounted Cash Flow Signals Undervaluation

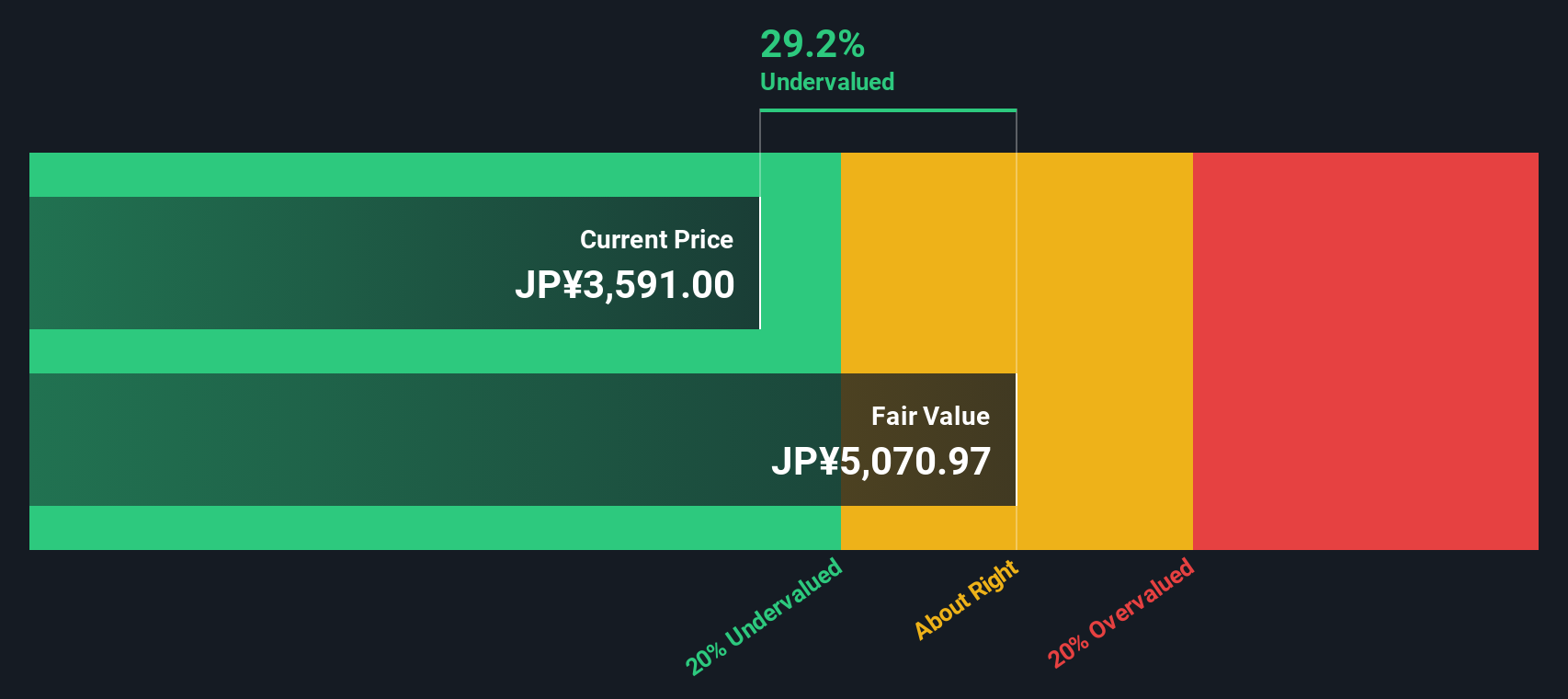

While the market seems to have priced Glory as expensive based on its current price-to-earnings ratio, our DCF model presents a different perspective. According to SWS's DCF analysis, the share price is actually trading about 26.7% below its estimated fair value. Could the market have overlooked something, or is caution still warranted?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Glory for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Glory Narrative

If you’d rather dig into the numbers personally and share a perspective beyond what we’ve covered, you can craft your own take on Glory in under three minutes with Do it your way.

Smart investors go where the opportunities are emerging, and Simply Wall Street’s screeners can help you spot tomorrow’s winners before the crowd catches up.

Uncover future market leaders by scanning these 24 AI penny stocks, which leverage artificial intelligence for game-changing growth and innovation across multiple industries.

Boost your search for high yield by checking these 16 dividend stocks with yields > 3%, offering robust dividends and the potential for steady passive income, regardless of market swings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks