Advertisement

Should Income Investors Look At Advanex Inc. (TSE:5998) Before Its Ex-Dividend?

Advanex Inc. (TSE:5998) stock is about to trade ex-dividend in four days. The ex-dividend date is two business days before a company's record date in most cases, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. In other words, investors can purchase Advanex's shares before the 28th of March in order to be eligible for the dividend, which will be paid on the 1st of January.

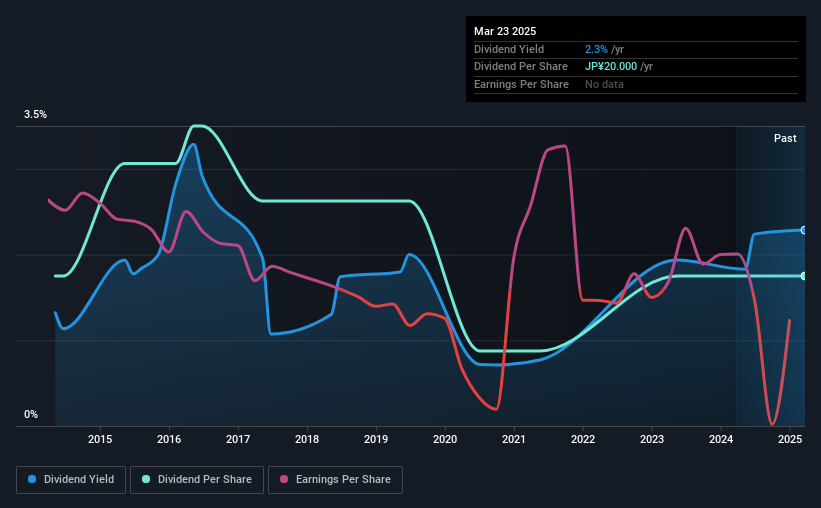

The company's next dividend payment will be JP¥20.00 per share, and in the last 12 months, the company paid a total of JP¥20.00 per share. Based on the last year's worth of payments, Advanex has a trailing yield of 2.3% on the current stock price of JP¥875.00. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. As a result, readers should always check whether Advanex has been able to grow its dividends, or if the dividend might be cut.

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Advanex's dividend is not well covered by earnings, as the company lost money last year. This is not a sustainable state of affairs, so it would be worth investigating if earnings are expected to recover. With the recent loss, it's important to check if the business generated enough cash to pay its dividend. If Advanex didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. Luckily it paid out just 21% of its free cash flow last year.

View our latest analysis for Advanex

Click here to see how much of its profit Advanex paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. Advanex reported a loss last year, but at least the general trend suggests its income has been improving over the past five years. Even so, an unprofitable company whose business does not quickly recover is usually not a good candidate for dividend investors.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Advanex's dividend payments are effectively flat on where they were 10 years ago.

Remember, you can always get a snapshot of Advanex's financial health, by checking our visualisation of its financial health, here.

Final Takeaway

Is Advanex an attractive dividend stock, or better left on the shelf? First, it's not great to see the company paying a dividend despite being loss-making over the last year. On the plus side, the dividend was covered by free cash flow." To summarise, Advanex looks okay on this analysis, although it doesn't appear a stand-out opportunity.

However if you're still interested in Advanex as a potential investment, you should definitely consider some of the risks involved with Advanex. Our analysis shows 4 warning signs for Advanex that we strongly recommend you have a look at before investing in the company.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5998

Advanex

Engages in the manufacture and sale of precision springs in Japan and internationally.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor