Advertisement

- Japan

- /

- Construction

- /

- TSE:1946

A Look at Toenec (TSE:1946) Valuation After Upgraded Guidance and Enhanced Dividend Policy

Simply Wall St

Reviewed by Simply Wall St

Toenec (TSE:1946) just raised its full-year earnings guidance and unveiled a more generous dividend policy, signaling confidence in its business momentum. This double announcement is likely to catch the eye of shareholders and market watchers alike.

See our latest analysis for Toenec.

Toenec’s latest upgrades have clearly sparked renewed optimism, with the share price surging 26.9% over the last month and up an impressive 83.8% year-to-date. While the company’s near-term momentum is striking, long-term holders have truly been rewarded, achieving a 95.5% total shareholder return over the past year and nearly tripling their investment over three years. The strong rally suggests investors are confident that the upgraded earnings outlook and more generous dividend approach will support further growth.

If this kind of turnaround momentum interests you, now is a great moment to explore other breakout opportunities and discover fast growing stocks with high insider ownership

With shares soaring and fresh guidance on the table, the real question becomes whether Toenec’s stock is still undervalued or if the impressive run means the market is already anticipating all of the future gains.

Price-to-Earnings of 11x: Is it justified?

Toenec’s stock currently trades at a price-to-earnings (P/E) ratio of 11x, putting it well below both industry peers and the broader construction sector in Japan. With shares closing at ¥1785, investors are getting exposure to earnings at a notable discount versus the sector.

The price-to-earnings multiple shows what the market is willing to pay today for a company’s earnings power. This is a key benchmark for the construction industry, as investors often gauge value by comparing ongoing profits.

A P/E of 11x not only signals a bargain against the JP Construction industry, which averages 12.4x, but also stands out compared to a peer average of 19.3x. The implication is clear: the market appears to be underestimating Toenec’s earnings growth and quality, especially considering its recent profit acceleration and sector-beating performance. If the stock moves toward the sector average, there may be additional upside potential.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 11x (UNDERVALUED)

However, shifts in construction demand or unexpected margin pressures could quickly change investor sentiment and challenge the optimistic outlook that is currently priced into Toenec’s stock.

Find out about the key risks to this Toenec narrative.

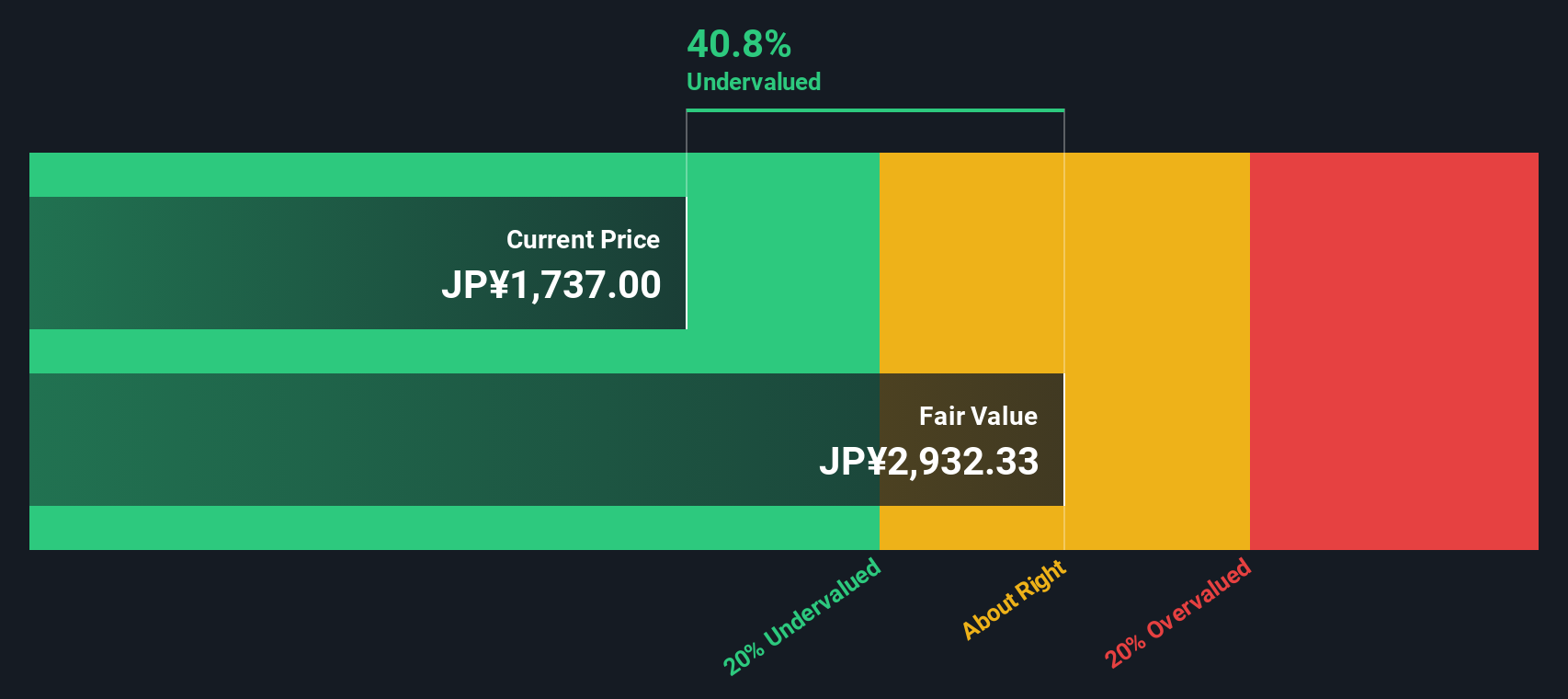

Another View: What Does the SWS DCF Model Suggest?

Looking beyond earnings multiples, the SWS DCF model estimates Toenec's fair value at ¥2941.44, which is 39.3% above the current share price. This indicates the market may be overlooking long-term cash flow potential. Could this gap mean more room for growth, or is there a reason for skepticism?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Toenec for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 849 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Toenec Narrative

If you think the analysis here misses something or would rather dive into the details yourself, you can create your own perspective in just a few minutes. Do it your way.

A great starting point for your Toenec research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors seize timely opportunities before the crowd. Use Simply Wall Street’s powerful Screener to spot hidden gems and make your next move with confidence.

- Spot high yields and steady income streams by checking out these 17 dividend stocks with yields > 3% with consistent payouts above 3%.

- Tap into the future of medicine and technology by reviewing these 32 healthcare AI stocks, which is leading advances in healthcare through artificial intelligence.

- Uncover tomorrow’s breakthroughs by tracking these 28 quantum computing stocks, which is at the forefront of quantum computing innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toenec might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1946

Toenec

Engages in the construction and improvement of social infrastructure in the energy, environment, and information technology fields in Japan.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor