Advertisement

- Japan

- /

- Construction

- /

- TSE:1893

Penta-Ocean Construction (TSE:1893): Evaluating Valuation After Share Buyback Authorization

Simply Wall St

Reviewed by Simply Wall St

Penta-Ocean Construction (TSE:1893) just announced a new share buyback program after its board approved the repurchase of up to 4,500,000 shares. This move is intended to strengthen its management base and improve capital efficiency.

See our latest analysis for Penta-Ocean Construction.

Penta-Ocean Construction’s latest buyback announcement comes as momentum in the share price has really accelerated, with a year-to-date share price return of 128.3% and a one-year total shareholder return of 150.77%. While the company’s focus has recently been on capital management moves like the approved repurchase, strong price gains in recent months suggest renewed investor confidence and growing optimism around its ability to drive value over the long term.

If you want to spot other companies where management confidence and rapid gains are on display, this is a great moment to discover fast growing stocks with high insider ownership

With shares having already soared this year and trading above analyst targets, the big question now is whether Penta-Ocean Construction is offering investors a real bargain or if markets have already priced in forthcoming growth potential.

Price-to-Earnings of 21x: Is it justified?

Penta-Ocean Construction’s shares are trading at a price-to-earnings ratio of 21x, which puts them at a significant premium compared to peers and industry averages. With the last close price at ¥1,501.5, investors pay a higher price for each ¥1 of earnings generated by the company.

The price-to-earnings (P/E) ratio measures how much investors are willing to pay for every unit of current earnings. For construction companies, this metric is commonly used to compare valuations across similar businesses, as earnings are a primary driver of shareholder returns.

Currently, Penta-Ocean Construction’s P/E multiple significantly exceeds key benchmarks. The company is valued higher than the peer average of 16x and well above the Japanese construction industry average of 12.1x. Even when measured against the SWS Fair Price-to-Earnings Ratio of 19x, the stock still looks expensive. This reflects market optimism about future profit growth, but places a high bar for continued performance.

Explore the SWS fair ratio for Penta-Ocean Construction

Result: Price-to-Earnings of 21x (OVERVALUED)

However, slower revenue growth and shares trading above analyst price targets could prompt investors to reassess growth expectations in the coming months.

Find out about the key risks to this Penta-Ocean Construction narrative.

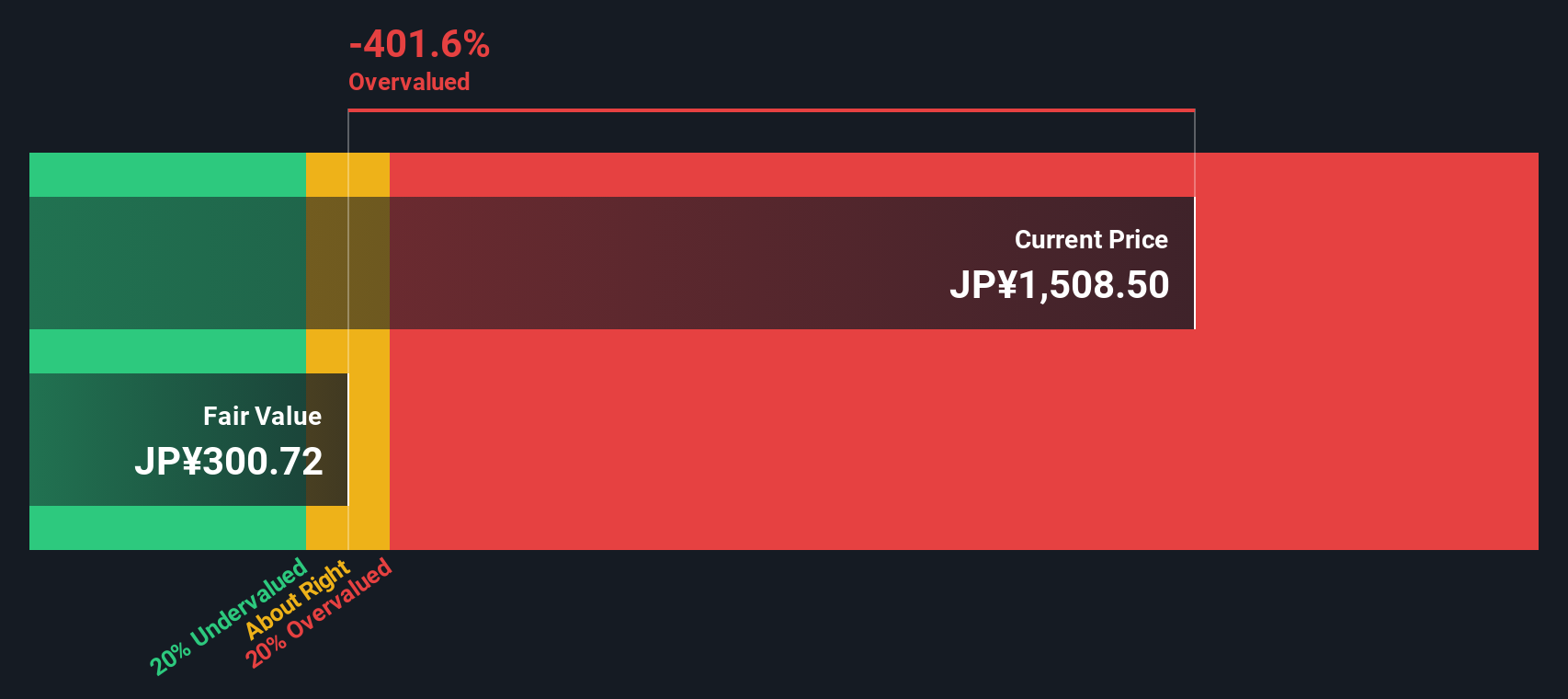

Another View: SWS DCF Model Paints a Much Cheaper Picture

While Penta-Ocean Construction’s shares look expensive based on earnings multiples, the SWS DCF model suggests a sharply different story. According to the model, the fair value is much lower than the current share price, indicating the stock is overvalued by a wide margin. This stark contrast raises the question: which valuation should investors trust when momentum is running high?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Penta-Ocean Construction for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 869 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Penta-Ocean Construction Narrative

If you have a different take or want to dive deeper into the numbers yourself, you can put together your own view in less than three minutes with Do it your way.

A great starting point for your Penta-Ocean Construction research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Sharpen your investment edge and move ahead of the pack by targeting stocks with qualities that match your goals. Don’t let unique opportunities slip by. These carefully chosen screens can help you spot tomorrow’s winners today.

- Boost your passive income potential and check out high-yield picks in these 16 dividend stocks with yields > 3% delivering yields above 3%.

- Ride the momentum in artificial intelligence by targeting innovation leaders found in these 25 AI penny stocks who are reshaping the future of tech.

- Secure your spot among savvy investors seeking value by investigating these 869 undervalued stocks based on cash flows that are poised for a rebound based on strong cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1893

Penta-Ocean Construction

Engages in the civil engineering and building construction activities in Japan, Southeast Asia, and internationally.

Average dividend payer with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor