Toda (TSE:1860) shares edged up after a quiet session, gaining nearly 2% and extending their steady month-long advance. The modest move reflects ongoing interest in the capital goods sector as investors gauge broader trends in Japanese infrastructure spending.

Toda has quietly built positive momentum, with a 1-month share price return of 8% and year-to-date gains topping 14%. Looking further back, the 1-year total shareholder return stands at a healthy 20%, supported by solid long-term performance as well. Investors appear to be warming up to the growth outlook, even as the pace of infrastructure spending remains a talking point across the sector.

Yet with Toda's shares now above recent analyst targets as the stock hovers near new highs, the big question for investors is whether there is unrealized value left, or if the market has already priced in the company’s future growth.

Advertisement

Price-to-Earnings of 13x: Is it justified?

Toda currently trades at a price-to-earnings (P/E) ratio of 13x, which puts its valuation in focus as shares sit above recent analyst targets. Compared to both its own history and major industry benchmarks, this premium warrants a closer look at what the market may be expecting from future growth and profitability.

The price-to-earnings multiple is a widely used measure that compares a company’s share price to its per-share earnings, helping investors gauge how much they are paying for each unit of earnings. In the capital goods sector, where future growth can be relatively modest and margins are key, this ratio is a direct indicator of prevailing optimism or caution around the company’s prospects.

While Toda’s P/E of 13x is below the Japanese market average of 14.1x, it stands above the construction industry’s average of 12.1x, suggesting a modest premium relative to sector peers. However, it also exceeds the estimated fair P/E ratio of 12.8x, hinting that the market may still be optimistic about Toda’s longer-term outlook even as short-term earnings forecasts remain subdued. If sentiment shifts or profit delivery misses expectations, the P/E could realign towards these sector and fair value benchmarks.

However, slower revenue growth, combined with slightly negative annual net income growth, may challenge Toda’s ability to justify its current valuation going forward.

Another View: What Does the SWS DCF Model Suggest?

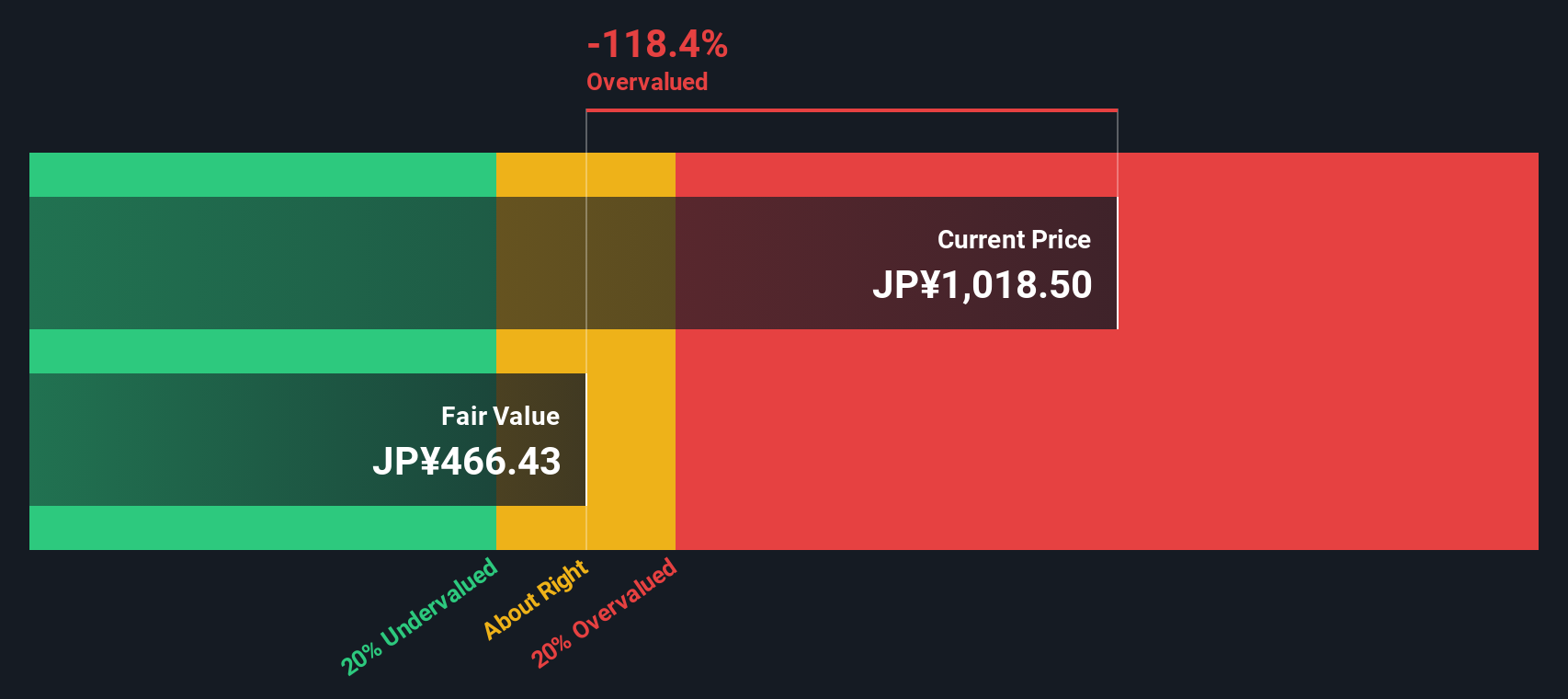

Looking at Toda through the lens of our DCF model provides a more conservative perspective. The SWS DCF model estimates Toda’s fair value at ¥462.23, while shares currently trade significantly above this level. This view indicates the stock may be substantially overvalued if long-term cash flows fall short. Could the market be too optimistic, or are there factors the model is not capturing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Toda for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Toda Narrative

If you see the story differently or want to dig deeper into the numbers, you can quickly put your own perspective together in just a few minutes. Do it your way

Fuel your watchlist with these 25 AI penny stocks, stocks at the forefront of artificial intelligence that are driving innovation and unlocking new business frontiers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toda might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.