Advertisement

Keiyo Bank (TSE:8544): Valuation in Focus After Upgraded Earnings Outlook on Stronger Net Interest and Lower Credit Costs

Simply Wall St

Reviewed by Simply Wall St

Keiyo Bank (TSE:8544) has just revised its earnings forecast upward for the six months ending September 2025, citing improved operating performance. This updated guidance comes as net interest income and securities gains outpace earlier projections. Lower credit costs have also contributed.

See our latest analysis for Keiyo Bank.

Keiyo Bank’s new guidance has been met with strong momentum in the shares, with a 2.92% gain just today and a remarkable 70.57% share price return so far this year. Over the past 12 months, investors have seen a standout 88.20% total shareholder return, which reflects rising confidence as the bank’s growth narrative strengthens.

If impressive gains like these have you scanning the market for your next opportunity, broaden your search and discover fast growing stocks with high insider ownership.

Yet with Keiyo Bank’s shares up nearly 71% year-to-date and strong results now public, investors may be wondering if there is still value left for new investors or if the market is already factoring in all the future growth.

Price-to-Earnings of 14.2x: Is it justified?

Keiyo Bank's shares currently trade at a price-to-earnings (P/E) ratio of 14.2 times earnings, noticeably above both the Japanese Banks industry average and its direct peers. This elevated multiple has significant implications for investors weighing whether the strong performance is fully reflected in the stock price.

The price-to-earnings ratio compares the company’s current share price to its earnings per share, effectively measuring what investors are willing to pay for each unit of earnings. For banks, the P/E is commonly used as a key benchmark for valuation because of the generally stable earnings in the sector.

The market is clearly assigning a premium to Keiyo Bank, with the P/E ratio far exceeding the peer average of 12.1x and the broader industry average of 11.4x. This suggests investors are expecting continued growth or higher-quality earnings. However, such optimism may already be reflected in the price at these levels.

Without a fair ratio calculation to provide an objective benchmark, it is challenging to justify the premium on quantitative grounds alone. Comparatively, this makes Keiyo Bank seem expensive even among high-performing local banks.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 14.2x (OVERVALUED)

However, slower economic growth or unexpected shifts in interest rates could quickly challenge the recent optimism around Keiyo Bank's elevated valuation.

Find out about the key risks to this Keiyo Bank narrative.

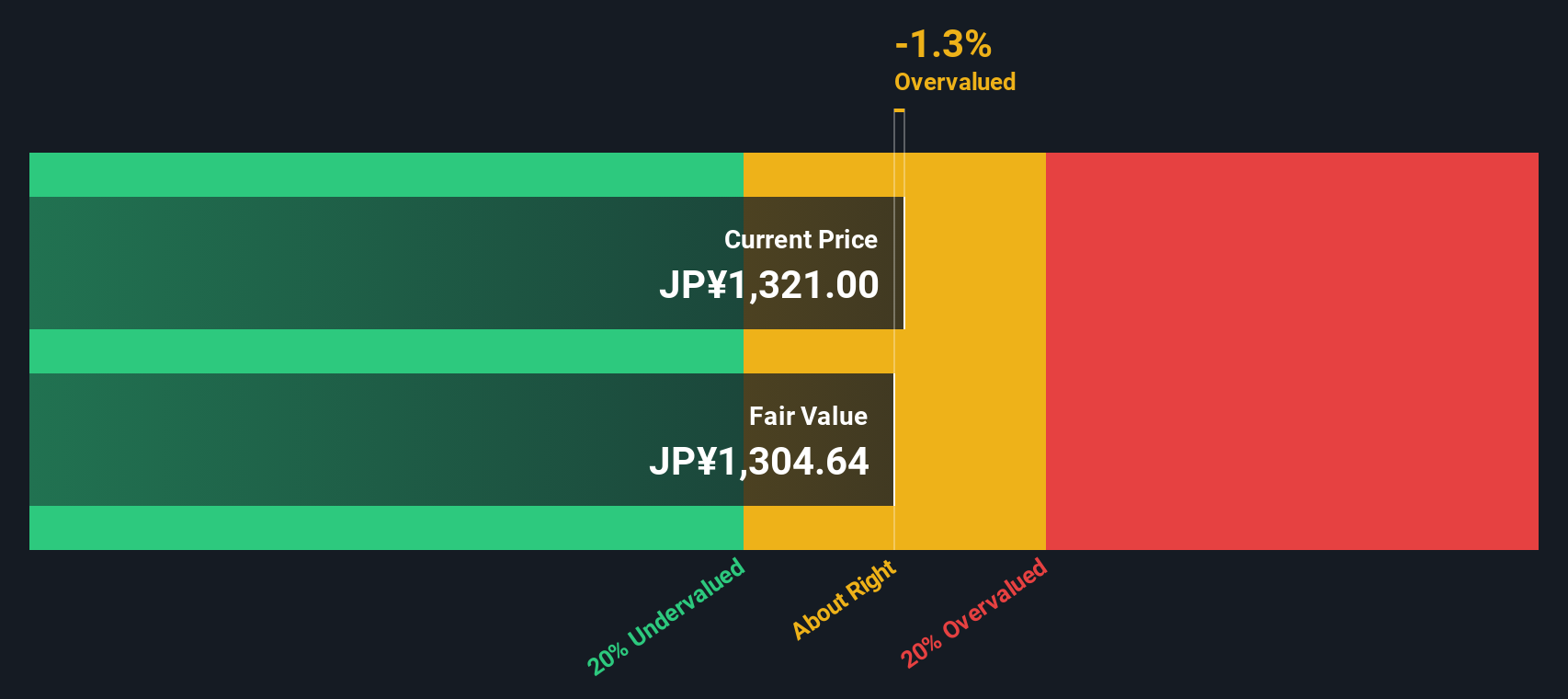

Another View: What Does the SWS DCF Model Indicate?

Looking from a different angle, our SWS DCF model estimates Keiyo Bank’s fair value at ¥1,305.49, slightly below the current share price of ¥1,339. This suggests shares are trading around 2.6% above fair value. In practical terms, this model signals investors may be paying a slight premium for future growth. Might the market be anticipating even better results ahead?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Keiyo Bank for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 848 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Keiyo Bank Narrative

If you see the numbers differently or want to dive deeper into your own research, you can craft your own take in just a few minutes. Do it your way.

A great starting point for your Keiyo Bank research is our analysis highlighting 2 important warning signs that could impact your investment decision.

Looking for More Winning Investment Ideas?

Smart investors never stop at just one opportunity. Expand your horizons and confidently uncover new stocks primed for growth, income, or innovation before the crowd catches on.

- Capture passive income potential with above-average yields featured in these 17 dividend stocks with yields > 3% to strengthen your portfolio for the long haul.

- Capitalize on the AI revolution by targeting companies leading cutting-edge advancements in automation and machine learning through these 25 AI penny stocks.

- Spot hidden bargains that may be trading well below their intrinsic value with real cash flow strength, thanks to these 848 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Keiyo Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8544

Keiyo Bank

Offers various banking products and services to individual, corporate, and business customers in Japan.

Adequate balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor