Key Insights

- A2A's Annual General Meeting to take place on 29th of November

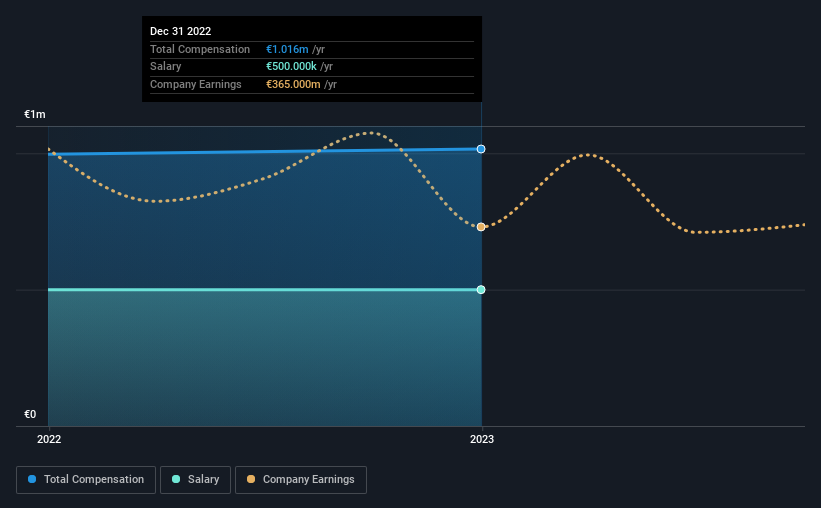

- CEO Renato Mazzoncini's total compensation includes salary of €500.0k

- The total compensation is 55% less than the average for the industry

- A2A's EPS declined by 9.6% over the past three years while total shareholder return over the past three years was 79%

The performance at A2A S.p.A. (BIT:A2A) has been rather lacklustre of late and shareholders may be wondering what CEO Renato Mazzoncini is planning to do about this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 29th of November. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. In our opinion, CEO compensation does not look excessive and we discuss why.

View our latest analysis for A2A

How Does Total Compensation For Renato Mazzoncini Compare With Other Companies In The Industry?

At the time of writing, our data shows that A2A S.p.A. has a market capitalization of €6.0b, and reported total annual CEO compensation of €1.0m for the year to December 2022. That is, the compensation was roughly the same as last year. While we always look at total compensation first, our analysis shows that the salary component is less, at €500k.

In comparison with other companies in the Italy Integrated Utilities industry with market capitalizations ranging from €3.7b to €11b, the reported median CEO total compensation was €2.3m. Accordingly, A2A pays its CEO under the industry median. Moreover, Renato Mazzoncini also holds €289k worth of A2A stock directly under their own name.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | €500k | €500k | 49% |

| Other | €516k | €496k | 51% |

| Total Compensation | €1.0m | €996k | 100% |

On an industry level, roughly 41% of total compensation represents salary and 59% is other remuneration. A2A is paying a higher share of its remuneration through a salary in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at A2A S.p.A.'s Growth Numbers

A2A S.p.A. has reduced its earnings per share by 9.6% a year over the last three years. Its revenue is down 21% over the previous year.

Overall this is not a very positive result for shareholders. This is compounded by the fact revenue is actually down on last year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has A2A S.p.A. Been A Good Investment?

We think that the total shareholder return of 79%, over three years, would leave most A2A S.p.A. shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Although shareholders would be quite happy with the returns they have earned on their initial investment, earnings have failed to grow and this could mean these strong returns may not continue. Shareholders might want to question the board about these concerns, and revisit their investment thesis for the company.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 1 warning sign for A2A that investors should look into moving forward.

Switching gears from A2A, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:A2A

A2A

Engages in the production, sale, and distribution of gas and electricity, and district heating in Italy and internationally.

Undervalued with solid track record and pays a dividend.