- India

- /

- Specialty Stores

- /

- NSEI:TRENT

These 4 Measures Indicate That Trent (NSE:TRENT) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Trent Limited (NSE:TRENT) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Trent

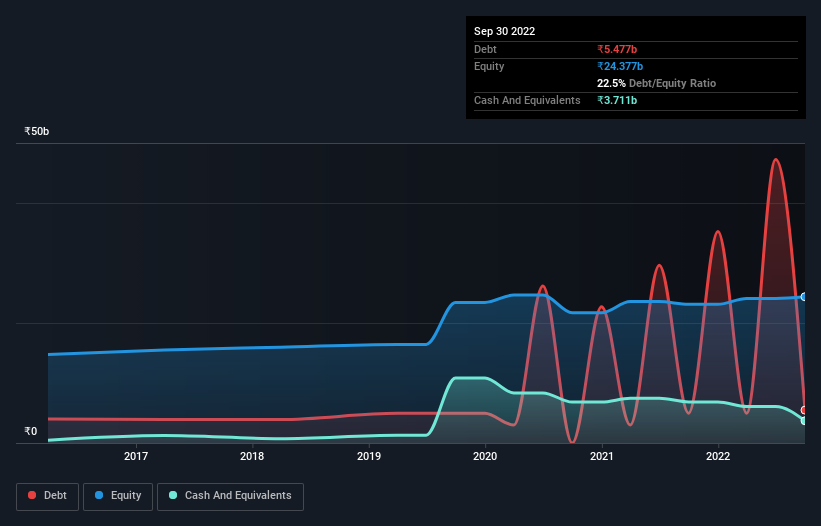

What Is Trent's Debt?

As you can see below, at the end of September 2022, Trent had ₹5.48b of debt, up from ₹4.97b a year ago. Click the image for more detail. However, it also had ₹3.71b in cash, and so its net debt is ₹1.77b.

A Look At Trent's Liabilities

We can see from the most recent balance sheet that Trent had liabilities of ₹9.04b falling due within a year, and liabilities of ₹43.9b due beyond that. Offsetting these obligations, it had cash of ₹3.71b as well as receivables valued at ₹530.5m due within 12 months. So it has liabilities totalling ₹48.7b more than its cash and near-term receivables, combined.

Of course, Trent has a market capitalization of ₹504.3b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. But either way, Trent has virtually no net debt, so it's fair to say it does not have a heavy debt load!

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Trent has a very low debt to EBITDA ratio of 0.24 so it is strange to see weak interest coverage, with last year's EBIT being only 1.8 times the interest expense. So while we're not necessarily alarmed we think that its debt is far from trivial. Notably, Trent's EBIT launched higher than Elon Musk, gaining a whopping 204% on last year. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Trent's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last two years, Trent saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

We weren't impressed with Trent's interest cover, and its conversion of EBIT to free cash flow made us cautious. But like a ballerina ending on a perfect pirouette, it has not trouble growing its EBIT. When we consider all the factors mentioned above, we do feel a bit cautious about Trent's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Trent is showing 1 warning sign in our investment analysis , you should know about...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Trent might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TRENT

Trent

Engages in the retailing and trading of apparels, footwear, accessories, toys, games, and other products in India.

Exceptional growth potential with flawless balance sheet.