- India

- /

- Basic Materials

- /

- NSEI:GRASIM

Grasim Industries' (NSE:GRASIM) Sluggish Earnings Might Be Just The Beginning Of Its Problems

A lackluster earnings announcement from Grasim Industries Limited (NSE:GRASIM) last week didn't sink the stock price. Our analysis suggests that along with soft profit numbers, investors should be aware of some other underlying weaknesses in the numbers.

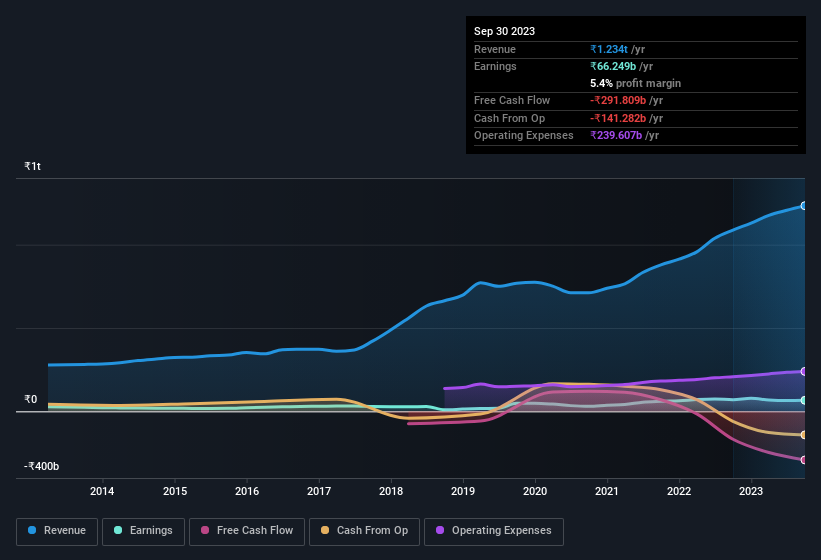

Check out our latest analysis for Grasim Industries

The Impact Of Unusual Items On Profit

For anyone who wants to understand Grasim Industries' profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit gained from ₹30b worth of unusual items. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. If Grasim Industries doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Grasim Industries' Profit Performance

Arguably, Grasim Industries' statutory earnings have been distorted by unusual items boosting profit. Because of this, we think that it may be that Grasim Industries' statutory profits are better than its underlying earnings power. But the good news is that its EPS growth over the last three years has been very impressive. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you'd like to know more about Grasim Industries as a business, it's important to be aware of any risks it's facing. For instance, we've identified 4 warning signs for Grasim Industries (2 don't sit too well with us) you should be familiar with.

Today we've zoomed in on a single data point to better understand the nature of Grasim Industries' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:GRASIM

Grasim Industries

Primarily operates in fibre, yarn, pulp, chemicals, textile, fertilizers, and insulators businesses in India and internationally.

Moderate second-rate dividend payer.