The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Ambuja Cements Limited (NSE:AMBUJACEM) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Ambuja Cements

How Much Debt Does Ambuja Cements Carry?

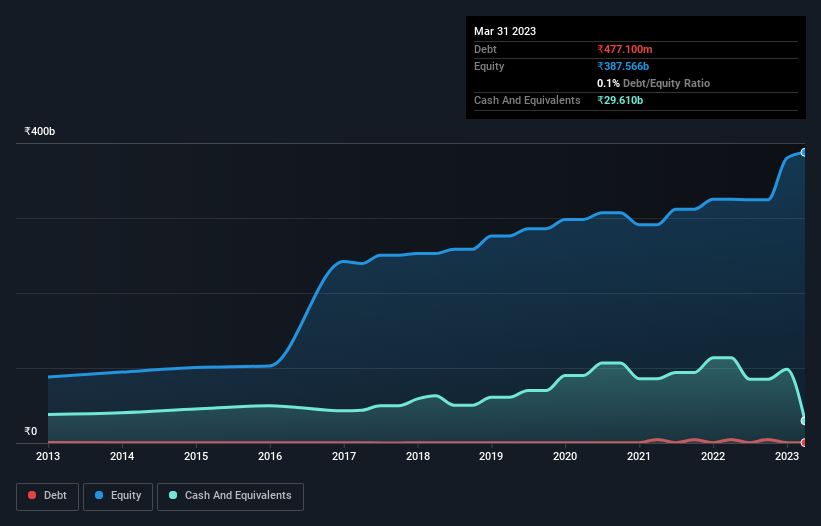

As you can see below, Ambuja Cements had ₹477.1m of debt at March 2023, down from ₹4.77b a year prior. However, its balance sheet shows it holds ₹29.6b in cash, so it actually has ₹29.1b net cash.

How Healthy Is Ambuja Cements' Balance Sheet?

According to the last reported balance sheet, Ambuja Cements had liabilities of ₹115.1b due within 12 months, and liabilities of ₹14.5b due beyond 12 months. Offsetting this, it had ₹29.6b in cash and ₹11.6b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹88.4b.

Since publicly traded Ambuja Cements shares are worth a very impressive total of ₹915.4b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Ambuja Cements also has more cash than debt, so we're pretty confident it can manage its debt safely.

The modesty of its debt load may become crucial for Ambuja Cements if management cannot prevent a repeat of the 49% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Ambuja Cements's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Ambuja Cements may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Ambuja Cements created free cash flow amounting to 17% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing Up

We could understand if investors are concerned about Ambuja Cements's liabilities, but we can be reassured by the fact it has has net cash of ₹29.1b. So we don't have any problem with Ambuja Cements's use of debt. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 1 warning sign with Ambuja Cements , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:AMBUJACEM

Ambuja Cements

Manufactures and markets cement and cement related products to individual homebuilders, masons and contractors, and architects and engineers in India.

Flawless balance sheet with reasonable growth potential.