Timken India Limited (NSE:TIMKEN) Delivered A Weaker ROE Than Its Industry

Many investors are still learning about the various metrics that can be useful when analysing a stock. This article is for those who would like to learn about Return On Equity (ROE). We'll use ROE to examine Timken India Limited (NSE:TIMKEN), by way of a worked example.

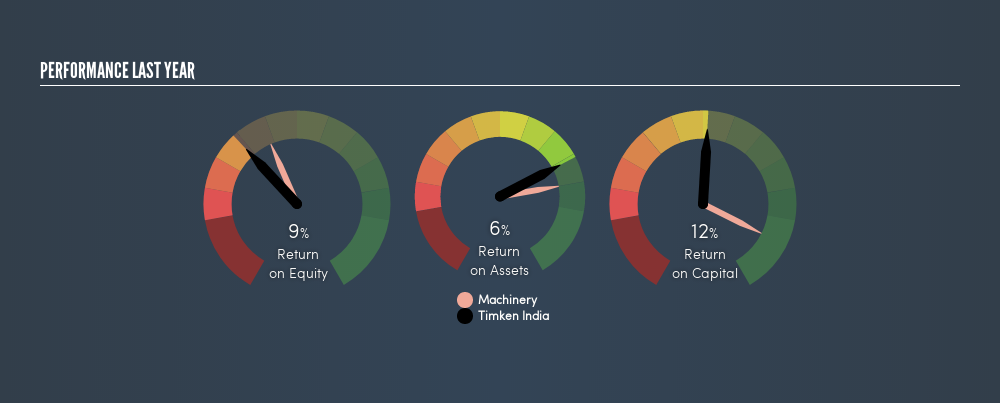

Our data shows Timken India has a return on equity of 9.2% for the last year. One way to conceptualize this, is that for each ₹1 of shareholders' equity it has, the company made ₹0.092 in profit.

Check out our latest analysis for Timken India

How Do I Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit ÷ Shareholders' Equity

Or for Timken India:

9.2% = ₹1.2b ÷ ₹13b (Based on the trailing twelve months to December 2018.)

Most readers would understand what net profit is, but it’s worth explaining the concept of shareholders’ equity. It is the capital paid in by shareholders, plus any retained earnings. Shareholders' equity can be calculated by subtracting the total liabilities of the company from the total assets of the company.

What Does Return On Equity Signify?

ROE looks at the amount a company earns relative to the money it has kept within the business. The 'return' is the yearly profit. That means that the higher the ROE, the more profitable the company is. So, all else equal, investors should like a high ROE. That means it can be interesting to compare the ROE of different companies.

Does Timken India Have A Good ROE?

One simple way to determine if a company has a good return on equity is to compare it to the average for its industry. Importantly, this is far from a perfect measure, because companies differ significantly within the same industry classification. If you look at the image below, you can see Timken India has a lower ROE than the average (12%) in the Machinery industry classification.

That certainly isn't ideal. We'd prefer see an ROE above the industry average, but it might not matter if the company is undervalued. Nonetheless, it could be useful to double-check if insiders have sold shares recently.

Why You Should Consider Debt When Looking At ROE

Virtually all companies need money to invest in the business, to grow profits. That cash can come from issuing shares, retained earnings, or debt. In the first and second cases, the ROE will reflect this use of cash for investment in the business. In the latter case, the debt required for growth will boost returns, but will not impact the shareholders' equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

Combining Timken India's Debt And Its 9.2% Return On Equity

Timken India has a debt to equity ratio of just 0.014, which is very low. Its ROE is certainly on the low side, and since it already uses debt, we're not too excited about the company. Conservative use of debt to boost returns is usually a good move for shareholders, though it does leave the company more exposed to interest rate rises.

The Bottom Line On ROE

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. In my book the highest quality companies have high return on equity, despite low debt. If two companies have around the same level of debt to equity, and one has a higher ROE, I'd generally prefer the one with higher ROE.

But ROE is just one piece of a bigger puzzle, since high quality businesses often trade on high multiples of earnings. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So you might want to take a peek at this data-rich interactive graph of forecasts for the company.

Of course Timken India may not be the best stock to buy. So you may wish to see this free collection of other companies that have high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:TIMKEN

Timken India

Manufactures and distributes tapered roller bearings, other roller bearings, components, and accessories for the automotive sector and railway industry in India, the United States, and internationally.

Flawless balance sheet with reasonable growth potential.