Advertisement

- India

- /

- Electrical

- /

- NSEI:DELTAMAGNT

Shareholders Will Probably Hold Off On Increasing Delta Manufacturing Limited's (NSE:DELTAMAGNT) CEO Compensation For The Time Being

Under the guidance of CEO Ram Shroff, Delta Manufacturing Limited (NSE:DELTAMAGNT) has performed reasonably well recently. As shareholders go into the upcoming AGM on 29 September 2022, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still want to keep CEO compensation within reason.

View our latest analysis for Delta Manufacturing

How Does Total Compensation For Ram Shroff Compare With Other Companies In The Industry?

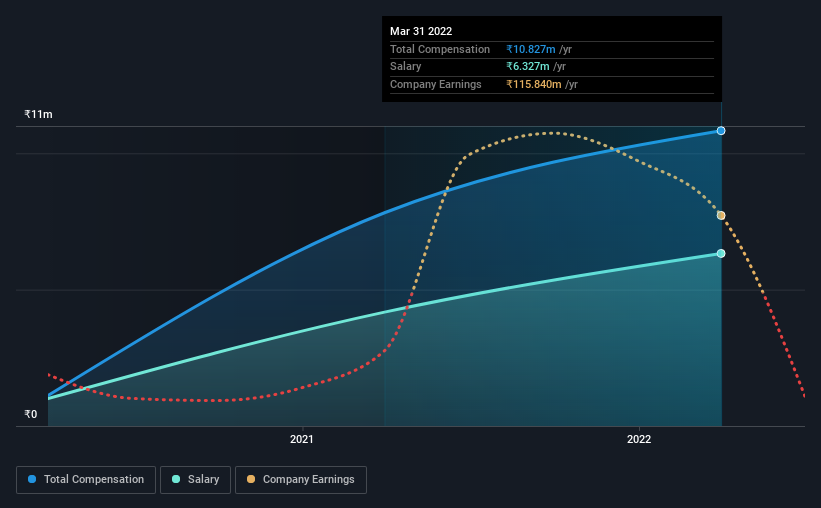

According to our data, Delta Manufacturing Limited has a market capitalization of ₹855m, and paid its CEO total annual compensation worth ₹11m over the year to March 2022. Notably, that's an increase of 38% over the year before. In particular, the salary of ₹6.33m, makes up a fairly large portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under ₹16b, the reported median total CEO compensation was ₹5.0m. Accordingly, our analysis reveals that Delta Manufacturing Limited pays Ram Shroff north of the industry median. What's more, Ram Shroff holds ₹4.7m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | ₹6.3m | ₹4.2m | 58% |

| Other | ₹4.5m | ₹3.6m | 42% |

| Total Compensation | ₹11m | ₹7.8m | 100% |

On an industry level, around 71% of total compensation represents salary and 29% is other remuneration. Delta Manufacturing pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Delta Manufacturing Limited's Growth

Delta Manufacturing Limited's earnings per share (EPS) grew 64% per year over the last three years. Its revenue is down 25% over the previous year.

Shareholders would be glad to know that the company has improved itself over the last few years. While it would be good to see revenue growth, profits matter more in the end. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Delta Manufacturing Limited Been A Good Investment?

We think that the total shareholder return of 91%, over three years, would leave most Delta Manufacturing Limited shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 1 warning sign for Delta Manufacturing that investors should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:DELTAMAGNT

Delta Manufacturing

Manufactures and sells hard ferrites, soft ferrites, textile woven labels, heat transfer labels, fabric printed labels, and elastic/woven tape in India and internationally.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor