Bank of Baroda's (NSE:BANKBARODA) Shareholders Will Receive A Bigger Dividend Than Last Year

The board of Bank of Baroda Limited (NSE:BANKBARODA) has announced that it will be paying its dividend of ₹5.50 on the 6th of August, an increased payment from last year's comparable dividend. This makes the dividend yield 3.0%, which is above the industry average.

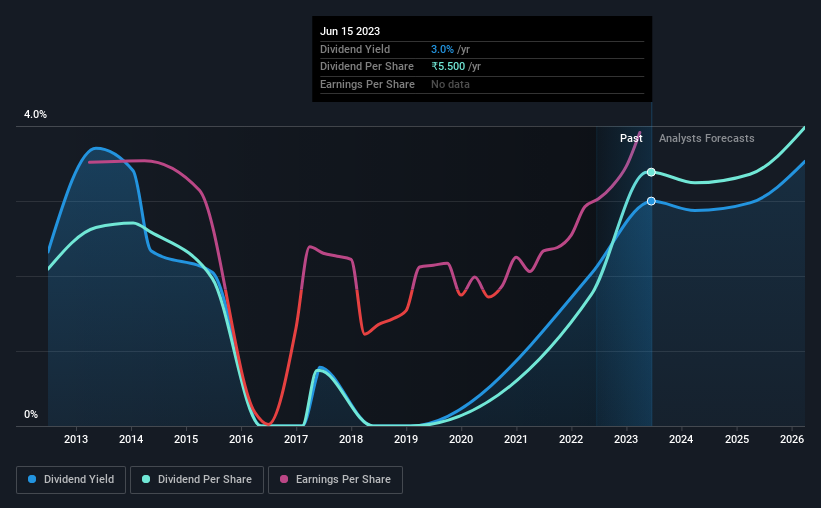

View our latest analysis for Bank of Baroda

Bank of Baroda's Payment Expected To Have Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much.

Having distributed dividends for at least 10 years, Bank of Baroda has a long history of paying out a part of its earnings to shareholders. While past records don't necessarily translate into future results, the company's payout ratio of 19% also shows that Bank of Baroda is able to comfortably pay dividends.

Looking forward, EPS is forecast to rise by 25.1% over the next 3 years. Analysts forecast the future payout ratio could be 18% over the same time horizon, which is a number we think the company can maintain.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The annual payment during the last 10 years was ₹3.40 in 2013, and the most recent fiscal year payment was ₹5.50. This means that it has been growing its distributions at 4.9% per annum over that time. Modest growth in the dividend is good to see, but we think this is offset by historical cuts to the payments. It is hard to live on a dividend income if the company's earnings are not consistent.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. It's encouraging to see that Bank of Baroda has been growing its earnings per share at 68% a year over the past five years. Earnings per share is growing at a solid clip, and the payout ratio is low which we think is an ideal combination in a dividend stock as the company can quite easily raise the dividend in the future.

We Really Like Bank of Baroda's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, Bank of Baroda has 2 warning signs (and 1 which can't be ignored) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Bank of Baroda might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BANKBARODA

Bank of Baroda

Provides various banking products and services to individuals, government departments, and corporate customers in India and internationally.

Established dividend payer and good value.