Weimob And 2 More SEHK Stocks Estimated To Be Trading Below Fair Value

Reviewed by Simply Wall St

The Hong Kong market has shown resilience despite global economic uncertainties, with the Hang Seng Index gaining 2.14% recently. As investors seek value amid fluctuating indices and mixed corporate earnings, identifying undervalued stocks becomes crucial for capitalizing on potential growth opportunities. In this article, we will explore three SEHK stocks estimated to be trading below their fair value, starting with Weimob.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Bosideng International Holdings (SEHK:3998) | HK$3.75 | HK$6.78 | 44.7% |

| Zhaojin Mining Industry (SEHK:1818) | HK$11.94 | HK$21.43 | 44.3% |

| WuXi XDC Cayman (SEHK:2268) | HK$19.74 | HK$39.28 | 49.7% |

| Pacific Textiles Holdings (SEHK:1382) | HK$1.48 | HK$2.85 | 48% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$28.25 | HK$56.25 | 49.8% |

| Hangzhou SF Intra-city Industrial (SEHK:9699) | HK$11.04 | HK$19.87 | 44.4% |

| Innovent Biologics (SEHK:1801) | HK$43.15 | HK$80.36 | 46.3% |

| United Company RUSAL International (SEHK:486) | HK$2.35 | HK$4.25 | 44.7% |

| DPC Dash (SEHK:1405) | HK$69.95 | HK$135.33 | 48.3% |

| Weimob (SEHK:2013) | HK$1.28 | HK$2.56 | 49.9% |

Underneath we present a selection of stocks filtered out by our screen.

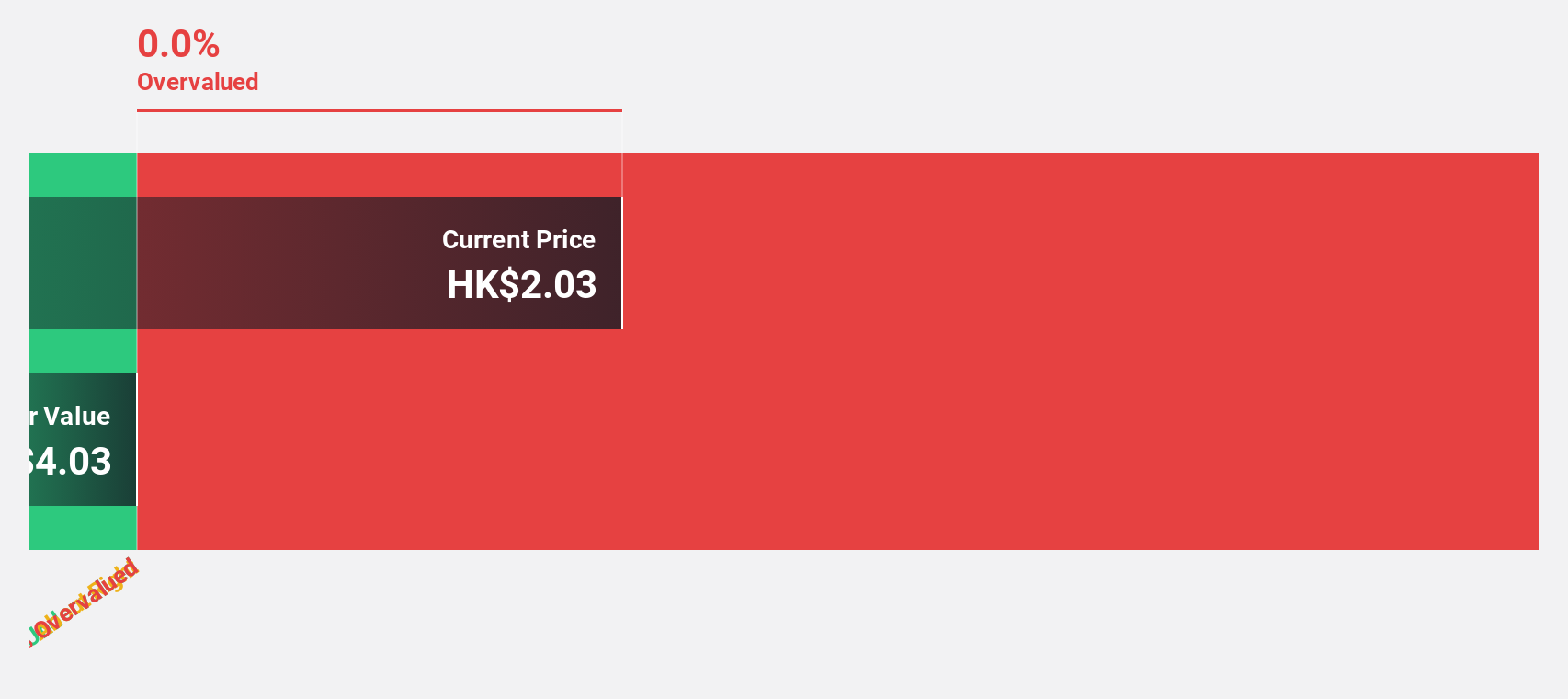

Weimob (SEHK:2013)

Overview: Weimob Inc., an investment holding company with a market cap of HK$3.94 billion, provides digital commerce and media services in the People’s Republic of China.

Operations: The company generates revenue from two main segments: Merchant Solutions (CN¥754.71 million) and Subscription Solutions (CN¥1.13 billion).

Estimated Discount To Fair Value: 49.9%

Weimob Inc. is trading at 49.9% below its estimated fair value of HK$2.56 per share, making it highly undervalued based on discounted cash flow analysis. Despite recent shareholder dilution and a low forecasted return on equity, the company’s revenue is expected to grow faster than the Hong Kong market at 16.5% annually, with earnings projected to increase significantly by 113.49% per year, becoming profitable within three years. Recent private placements raised $90 million in gross proceeds further bolstering its financial position.

- According our earnings growth report, there's an indication that Weimob might be ready to expand.

- Dive into the specifics of Weimob here with our thorough financial health report.

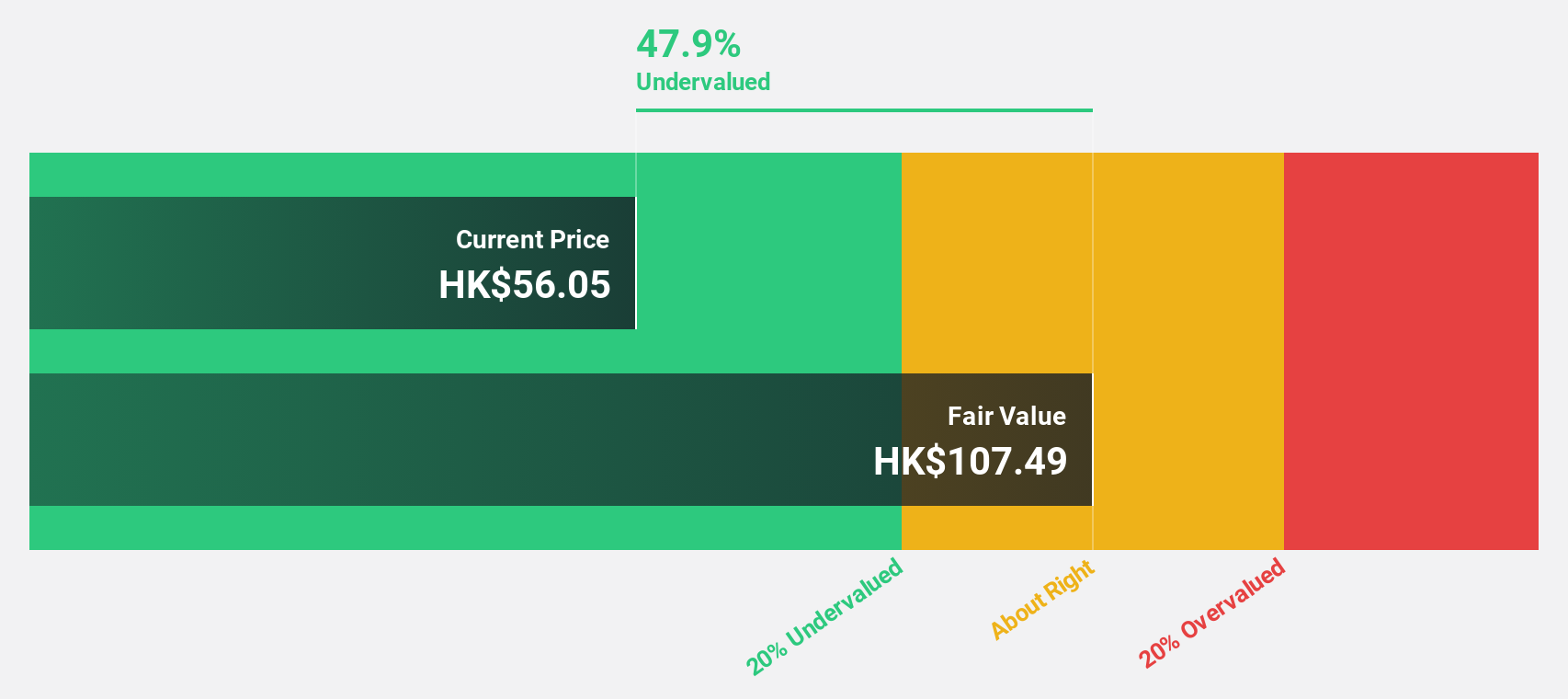

Shenzhou International Group Holdings (SEHK:2313)

Overview: Shenzhou International Group Holdings Limited is an investment holding company that manufactures, prints, and sells knitwear products in Mainland China, the European Union, the United States, Japan, and other international markets with a market cap of HK$94.03 billion.

Operations: The company's revenue from the manufacture and sale of knitwear products amounts to CN¥26.38 billion.

Estimated Discount To Fair Value: 35.2%

Shenzhou International Group Holdings is trading 35.2% below its estimated fair value of HK$96.28 per share, indicating significant undervaluation based on discounted cash flow analysis. The company reported robust earnings growth of 24% over the past year and a forecasted annual profit growth rate of 12.9%, outpacing the Hong Kong market’s average. Recent earnings showed a net income increase to CNY 2.93 billion, reinforcing its strong cash flow position despite an unstable dividend track record.

- The analysis detailed in our Shenzhou International Group Holdings growth report hints at robust future financial performance.

- Navigate through the intricacies of Shenzhou International Group Holdings with our comprehensive financial health report here.

Yunkang Group (SEHK:2325)

Overview: Yunkang Group Limited operates as a medical operation service provider in the People's Republic of China with a market cap of HK$4.93 billion.

Operations: The company generates revenue primarily from its Diagnostic Services segment, which amounts to CN¥794.58 million.

Estimated Discount To Fair Value: 38.9%

Yunkang Group's recent earnings report for the first half of 2024 showed a significant decline, with sales dropping to CNY 379.94 million and a net loss of CNY 126.13 million. Despite this, the stock is trading at HK$8.2, well below its estimated fair value of HK$13.41 based on discounted cash flow analysis, suggesting it may be undervalued. Revenue is forecast to grow at 10% per year, outpacing the Hong Kong market's average growth rate of 7.6%.

- The growth report we've compiled suggests that Yunkang Group's future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in Yunkang Group's balance sheet health report.

Next Steps

- Click here to access our complete index of 34 Undervalued SEHK Stocks Based On Cash Flows.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2313

Shenzhou International Group Holdings

An investment holding company, engages in the manufacture, printing, and sale of knitwear products in Mainland China, European Union, the United States, Japan, and internationally.

Excellent balance sheet, good value and pays a dividend.