Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Brainhole Technology Limited (HKG:2203) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Brainhole Technology

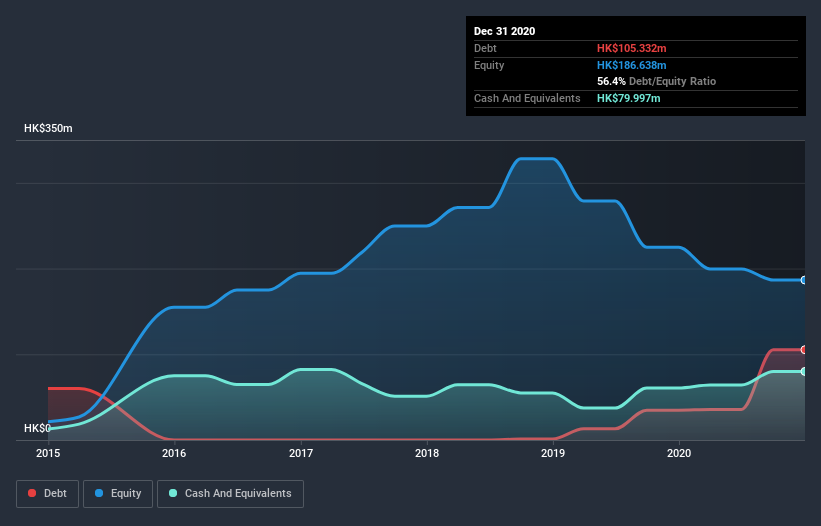

What Is Brainhole Technology's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Brainhole Technology had HK$105.3m of debt, an increase on HK$34.8m, over one year. However, it also had HK$80.0m in cash, and so its net debt is HK$25.3m.

How Healthy Is Brainhole Technology's Balance Sheet?

The latest balance sheet data shows that Brainhole Technology had liabilities of HK$105.8m due within a year, and liabilities of HK$78.0m falling due after that. Offsetting these obligations, it had cash of HK$80.0m as well as receivables valued at HK$99.9m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$3.79m.

Having regard to Brainhole Technology's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the HK$196.0m company is struggling for cash, we still think it's worth monitoring its balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Brainhole Technology will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Brainhole Technology made a loss at the EBIT level, and saw its revenue drop to HK$262m, which is a fall of 24%. That makes us nervous, to say the least.

Caveat Emptor

While Brainhole Technology's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping HK$35m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. For example, we would not want to see a repeat of last year's loss of HK$59m. So we do think this stock is quite risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with Brainhole Technology (at least 1 which is concerning) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Brainhole Technology, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Brainhole Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:2203

Brainhole Technology

An investment holding company, engages in the assembly, packaging, and sale of discrete semiconductors primarily for smart consumer electronic devices in the People’s Republic of China, Hong Kong, Korea, rest of Asia, Europe, and internationally.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor