- Hong Kong

- /

- Real Estate

- /

- SEHK:1918

Sunac China Holdings (SEHK:1918) Reports Improved Net Losses Following Recent Earnings Release

Reviewed by Simply Wall St

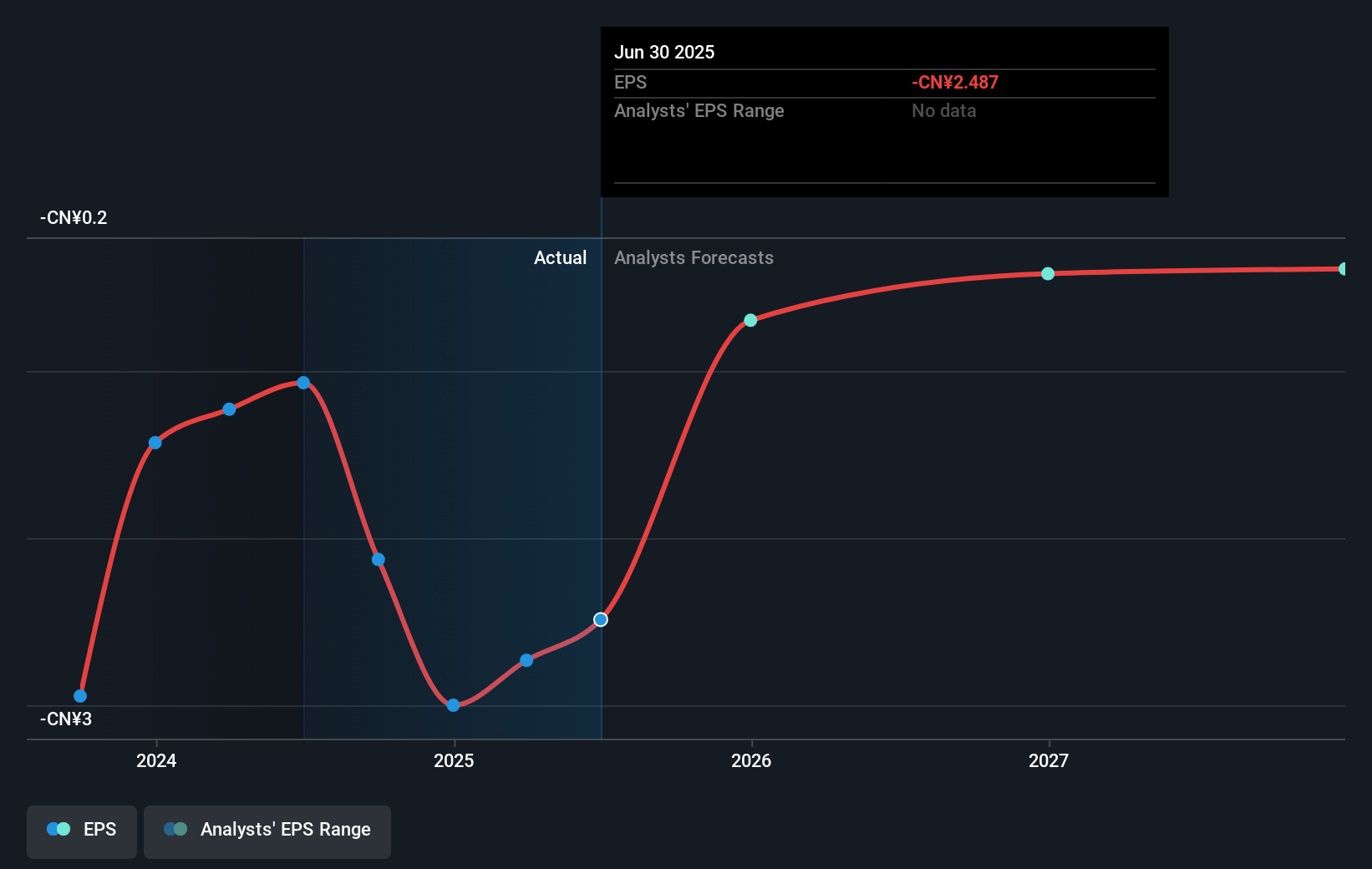

Sunac China Holdings (SEHK:1918) recently reported a 22% price increase over the last quarter. Key events during this period included an earnings release showing improved net losses, which provided some optimism despite a decline in sales. The upcoming Special/Extraordinary Shareholders Meeting may harbor shareholder interest. With broader market indices like the Dow Jones hitting record highs and hopes of interest rate cuts, Sunac's stock movement aligns with broader market trends, reflecting investor sentiment rather than individual company performance shifts. These events likely added weight to general market optimism rather than countering it.

Over the last year, Sunac China Holdings (SEHK:1918) achieved a total shareholder return of 84.95%, reflecting a robust period of growth. While the Hong Kong Real Estate industry and market itself experienced returns of 39% and 54.4% respectively over the same period, Sunac surpassed both benchmarks, indicating strong investor interest. This recent performance may, however, be tempered by the company's ongoing financial challenges including declining sales and unprofitability over the past few years.

The recent 22% quarterly price increase does not wholly align with analysts' price targets, which are estimated at HK$1.22, below the current market price of HK$1.72. This discrepancy suggests investor optimism driven by broader market conditions, such as hopes for interest rate cuts, rather than company-specific fundamentals. Moving forward, continuing losses, reduced sales, and strategic decisions made at upcoming shareholder meetings could impact future revenue and earnings forecasts, making cautious assessment crucial for stakeholders as the company navigates its financial trajectory.

Dive into the specifics of Sunac China Holdings here with our thorough balance sheet health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1918

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives