- Hong Kong

- /

- Metals and Mining

- /

- SEHK:1818

Top 3 SEHK Stocks Estimated To Be Undervalued In September 2024

Reviewed by Simply Wall St

As global markets grapple with economic uncertainties, the Hong Kong market has not been immune to volatility. Despite these challenges, opportunities still exist for discerning investors seeking undervalued stocks in the region. Identifying a good stock often involves looking at companies that are fundamentally strong but currently trading below their intrinsic value due to broader market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Bosideng International Holdings (SEHK:3998) | HK$3.62 | HK$6.74 | 46.3% |

| Shenzhou International Group Holdings (SEHK:2313) | HK$55.85 | HK$95.67 | 41.6% |

| CIMC Enric Holdings (SEHK:3899) | HK$5.80 | HK$10.44 | 44.4% |

| Zhaojin Mining Industry (SEHK:1818) | HK$12.34 | HK$21.44 | 42.4% |

| Hangzhou SF Intra-city Industrial (SEHK:9699) | HK$10.90 | HK$19.87 | 45.1% |

| XD (SEHK:2400) | HK$18.16 | HK$31.08 | 41.6% |

| Vobile Group (SEHK:3738) | HK$1.48 | HK$2.64 | 43.9% |

| Digital China Holdings (SEHK:861) | HK$3.21 | HK$6.10 | 47.4% |

| United Company RUSAL International (SEHK:486) | HK$2.30 | HK$4.25 | 45.9% |

| Innovent Biologics (SEHK:1801) | HK$43.30 | HK$79.60 | 45.6% |

Let's dive into some prime choices out of the screener.

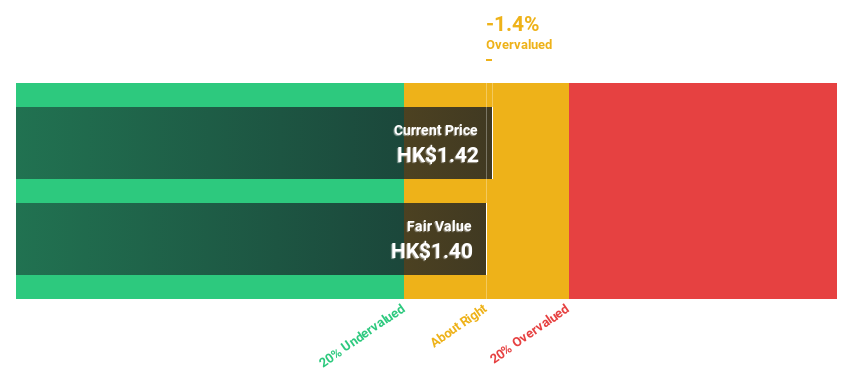

Zhou Hei Ya International Holdings (SEHK:1458)

Overview: Zhou Hei Ya International Holdings Company Limited, with a market cap of HK$3.12 billion, produces, markets, and retails casual braised food in the People’s Republic of China.

Operations: The company generates revenue primarily from the production, marketing, and retailing of casual braised duck-related food, amounting to CN¥2.59 billion.

Estimated Discount To Fair Value: 15.1%

Zhou Hei Ya International Holdings appears undervalued based on cash flows, trading at HK$1.43, below its estimated fair value of HK$1.68. Despite a recent decline in revenue to CNY 1.26 billion and net income to CNY 32.91 million for the first half of 2024, analysts forecast significant earnings growth of over 55% annually for the next three years, outpacing the Hong Kong market's average growth rate.

- Upon reviewing our latest growth report, Zhou Hei Ya International Holdings' projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Zhou Hei Ya International Holdings.

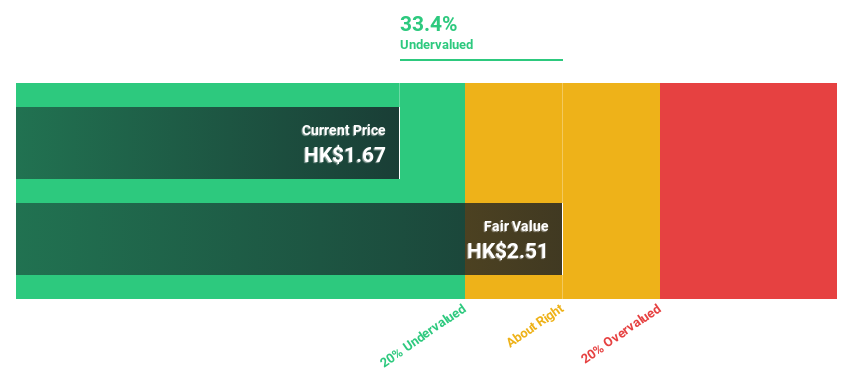

K. Wah International Holdings (SEHK:173)

Overview: K. Wah International Holdings Limited is an investment holding company involved in property development and investment in Hong Kong and Mainland China, with a market cap of HK$5.20 billion.

Operations: The company's revenue segments include Property Investment (HK$634.10 million), Property Development in Hong Kong (HK$669.98 million), and Property Development in Mainland China (HK$2.81 billion).

Estimated Discount To Fair Value: 34%

K. Wah International Holdings is trading at HK$1.65, significantly below its estimated fair value of HK$2.50, suggesting it is undervalued based on cash flows. Despite a recent drop in sales to HK$1.21 billion and net income to HK$153.79 million for the first half of 2024, earnings are forecasted to grow 43% annually over the next three years, outpacing the Hong Kong market's growth rate of 11%.

- Our expertly prepared growth report on K. Wah International Holdings implies its future financial outlook may be stronger than recent results.

- Navigate through the intricacies of K. Wah International Holdings with our comprehensive financial health report here.

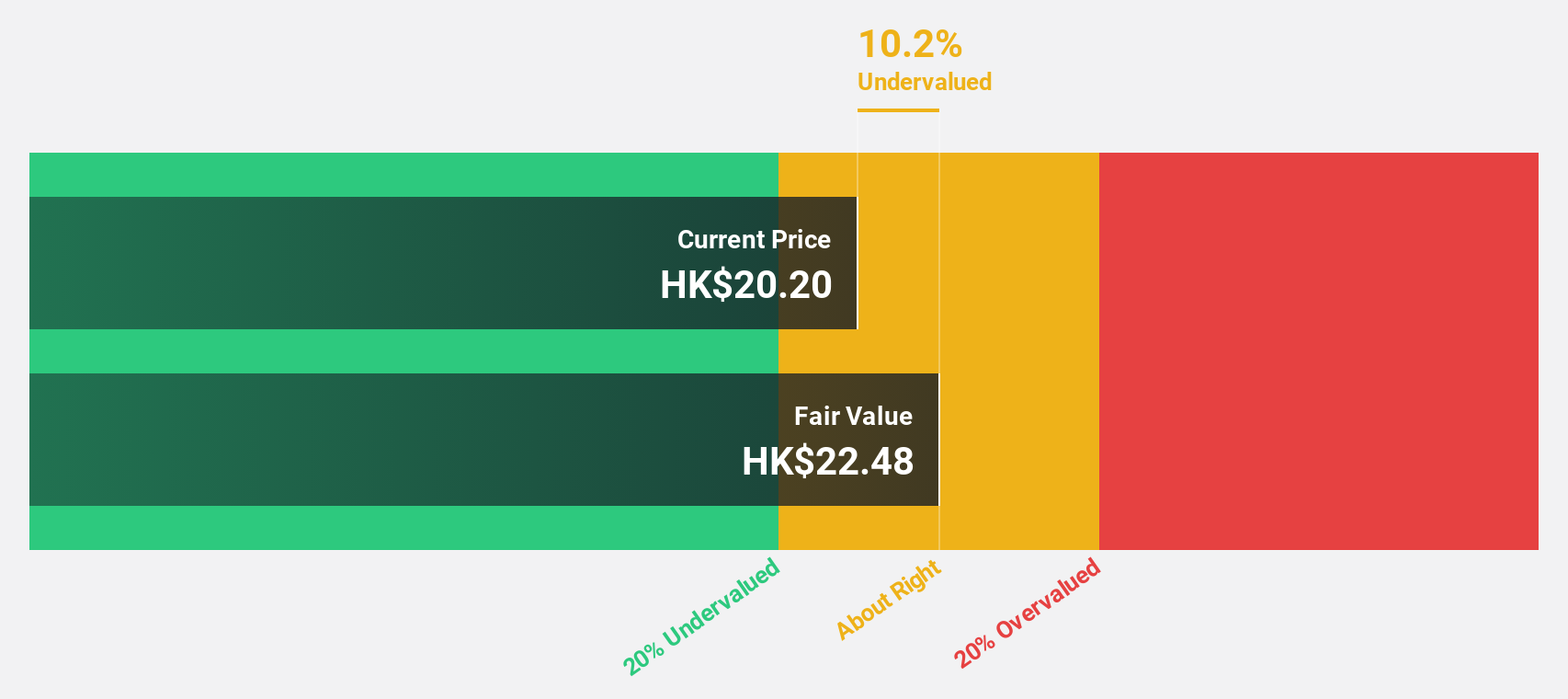

Zhaojin Mining Industry (SEHK:1818)

Overview: Zhaojin Mining Industry Company Limited, with a market cap of HK$40.08 billion, engages in the exploration, mining, processing, smelting, and sale of gold and silver products in the People’s Republic of China.

Operations: The company generates revenue through the exploration, mining, processing, smelting, and sale of gold and silver products in the People’s Republic of China.

Estimated Discount To Fair Value: 42.4%

Zhaojin Mining Industry is trading at HK$12.34, significantly below its estimated fair value of HK$21.44, indicating it is undervalued based on cash flows. The company reported substantial growth in earnings for the first half of 2024, with net income rising to CNY 552.79 million from CNY 252.86 million a year ago and basic earnings per share increasing to CNY 0.12 from CNY 0.04, despite recent shareholder dilution and significant insider selling over the past three months.

- Our earnings growth report unveils the potential for significant increases in Zhaojin Mining Industry's future results.

- Take a closer look at Zhaojin Mining Industry's balance sheet health here in our report.

Next Steps

- Unlock our comprehensive list of 25 Undervalued SEHK Stocks Based On Cash Flows by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zhaojin Mining Industry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1818

Zhaojin Mining Industry

An investment holding company, engages in exploration, mining, processing, smelting, and sale of gold and silver products in the People’s Republic of China.

High growth potential with excellent balance sheet.