Stock Analysis

- Hong Kong

- /

- Real Estate

- /

- SEHK:16

We Wouldn't Be Too Quick To Buy Sun Hung Kai Properties Limited (HKG:16) Before It Goes Ex-Dividend

Sun Hung Kai Properties Limited (HKG:16) is about to trade ex-dividend in the next 4 days. Typically, the ex-dividend date is one business day before the record date which is the date on which a company determines the shareholders eligible to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Accordingly, Sun Hung Kai Properties investors that purchase the stock on or after the 12th of March will not receive the dividend, which will be paid on the 20th of March.

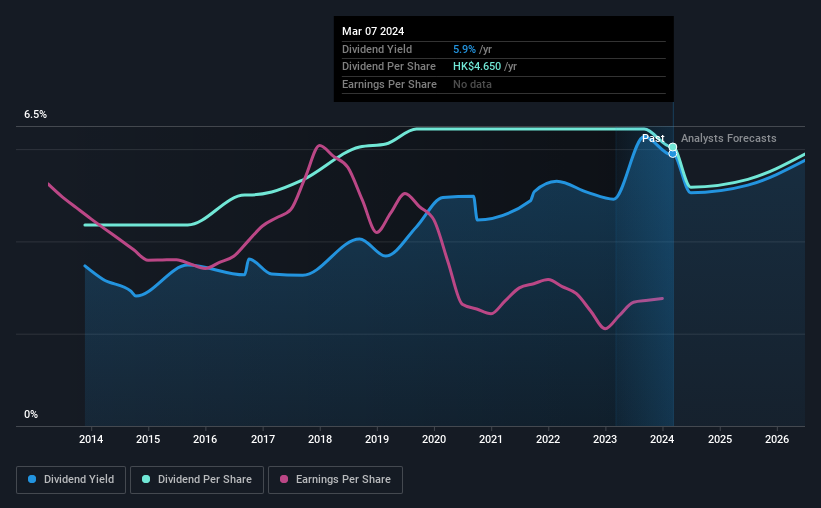

The company's upcoming dividend is HK$0.95 a share, following on from the last 12 months, when the company distributed a total of HK$4.65 per share to shareholders. Based on the last year's worth of payments, Sun Hung Kai Properties stock has a trailing yield of around 5.9% on the current share price of HK$78.75. If you buy this business for its dividend, you should have an idea of whether Sun Hung Kai Properties's dividend is reliable and sustainable. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

View our latest analysis for Sun Hung Kai Properties

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Sun Hung Kai Properties is paying out an acceptable 55% of its profit, a common payout level among most companies. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Over the last year it paid out 66% of its free cash flow as dividends, within the usual range for most companies.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Readers will understand then, why we're concerned to see Sun Hung Kai Properties's earnings per share have dropped 13% a year over the past five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Since the start of our data, 10 years ago, Sun Hung Kai Properties has lifted its dividend by approximately 3.3% a year on average. That's interesting, but the combination of a growing dividend despite declining earnings can typically only be achieved by paying out more of the company's profits. This can be valuable for shareholders, but it can't go on forever.

To Sum It Up

Is Sun Hung Kai Properties an attractive dividend stock, or better left on the shelf? It's never good to see earnings per share shrinking, but at least the dividend payout ratios appear reasonable. We're aware though that if earnings continue to decline, the dividend could be at risk. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Sun Hung Kai Properties.

Ever wonder what the future holds for Sun Hung Kai Properties? See what the 14 analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Valuation is complex, but we're helping make it simple.

Find out whether Sun Hung Kai Properties is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:16

Sun Hung Kai Properties

Sun Hung Kai Properties Limited develops and invests in properties for sale and rent in Hong Kong, Mainland China, and internationally.

Undervalued with proven track record and pays a dividend.