Advertisement

Returns On Capital Are A Standout For Ko Yo Chemical (Group) (HKG:827)

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. And in light of that, the trends we're seeing at Ko Yo Chemical (Group)'s (HKG:827) look very promising so lets take a look.

Return On Capital Employed (ROCE): What is it?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Ko Yo Chemical (Group) is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.30 = CN¥503m ÷ (CN¥4.0b - CN¥2.4b) (Based on the trailing twelve months to December 2021).

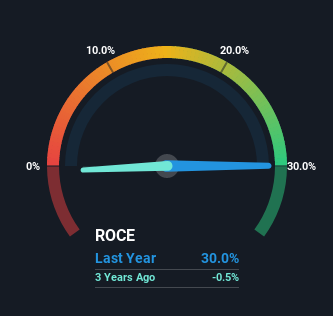

Therefore, Ko Yo Chemical (Group) has an ROCE of 30%. That's a fantastic return and not only that, it outpaces the average of 12% earned by companies in a similar industry.

Check out our latest analysis for Ko Yo Chemical (Group)

Historical performance is a great place to start when researching a stock so above you can see the gauge for Ko Yo Chemical (Group)'s ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Ko Yo Chemical (Group), check out these free graphs here.

What Does the ROCE Trend For Ko Yo Chemical (Group) Tell Us?

We're delighted to see that Ko Yo Chemical (Group) is reaping rewards from its investments and has now broken into profitability. While the business is profitable now, it used to be incurring losses on invested capital five years ago. In regards to capital employed, Ko Yo Chemical (Group) is using 22% less capital than it was five years ago, which on the surface, can indicate that the business has become more efficient at generating these returns. The reduction could indicate that the company is selling some assets, and considering returns are up, they appear to be selling the right ones.

On a separate but related note, it's important to know that Ko Yo Chemical (Group) has a current liabilities to total assets ratio of 58%, which we'd consider pretty high. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line On Ko Yo Chemical (Group)'s ROCE

In the end, Ko Yo Chemical (Group) has proven it's capital allocation skills are good with those higher returns from less amount of capital. Since the stock has returned a solid 97% to shareholders over the last five years, it's fair to say investors are beginning to recognize these changes. Therefore, we think it would be worth your time to check if these trends are going to continue.

One final note, you should learn about the 3 warning signs we've spotted with Ko Yo Chemical (Group) (including 2 which shouldn't be ignored) .

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Ko Yo Chemical (Group) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:827

Ko Yo Chemical (Group)

An investment holding company, engages in the research and development, manufacture, marketing, and distribution of chemical products and chemical fertilizers in the People’s Republic of China.

Slight risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$26.69|18.6% undervalued

BE

Community Contributor